If you’re earning six or even seven figures, you might assume you’re set for retirement.

But after working with high earners for over 20 years, helping them transition into financial independence, I’ve learned this isn’t always the case.

In fact, no matter how much someone earns, I often hear the same questions:

- “Will I have enough?”

- “Can I retire now?”

- “What should I be doing right now to prepare?”

In this post, I’ll walk you through:

- How to calculate how much you need to retire

- How to assess your current financial position

- A proven strategy we use with our clients to retire more securely - and sometimes even earlier

What does "enough" really mean?

Whether you’re early in your career or closing in on retirement, financial life management at its core is about one simple equation:

Save more than you spend.

In retirement, you’re no longer drawing a salary or running your business. So the question becomes: what income sources will replace that pay cheque?

Common income sources in retirement

- State pensions, if you’ve kept up with contributions

- Final salary (defined benefit) pensions, often available from public sector jobs or longstanding corporations

- Rental income from investment properties

- Part-time or passion-based work, sometimes even consulting

But will those income streams cover the lifestyle you want?

Example cash flow

If not, you’ll need to fill the gap using your savings and investments.

By the way, I also published a YouTube video on this very topic, which you can watch here if you prefer:

Building the bridge: savings and investments

That’s where assets come in — pensions, ISAs, general investment accounts, savings - these are your tools to generate income when your working days are over.

So when do you have enough?

It’s when the value of your assets is large enough to sustainably support your desired lifestyle for the rest of your life - without the fear of running out of money.

Think of it like owning a well on your property.

If it’s deep enough and fed by a reliable water source, you can keep drawing from it year after year.

If not, it runs dry — and fast.

The big unknowns (and why they matter)

Of course, it's not that simple.

Planning for retirement is filled with unknowns:

- How long will you live?

- What will inflation do to the value of your money?

- How will your investments perform?

- What will future tax rates look like?

Especially if you’re living or planning to retire abroad (like many of our clients in the Middle East), those unknowns are magnified.

We call this “educated guesswork.”

But smart guesswork needs to be based on real data.

The 4% Rule: a good starting point

Let’s say you want to know if you’ve hit your retirement number.

That’s where the 4% Rule comes in.

It’s a rough rule of thumb that says you can withdraw 4% of your retirement savings each year (adjusted for inflation), and your money should last at least 30 years.

So if you want to spend $100,000 per year, you’ll need a portfolio of $2.5 million ($100,000 x 25).

Example: meet John

John is a partner at a global law firm. He’s 52 and wants to retire at 55.

He calls his plan “ICE” — Independent, Continue Earning.

He’s done well:

- Small pension from his early UK work

- End of service benefit due

- Rental property in the UK

- Fully owns his home in Dubai

- Annual spending goal: $240,000 (or $20,000/month)

With $6 million in investments and assets, John already meets the 4% Rule threshold.

Even if markets fluctuate, and even with tax and location uncertainties, his situation looks strong - as long as the money is invested wisely.

Two things you need to remember

1. Inflation is the silent killer

We all think in today’s dollars (or pounds or dirhams).

But costs will go up - often by more than we expect.

That’s why your investments need to grow faster than inflation.

Planning based on today’s prices without accounting for inflation is like packing for summer and arriving in a snowstorm.

2. Taxes matter - a lot

Where you retire affects how much of your investment income you keep.

Structuring your portfolio for tax efficiency is vital - especially when your retirement location is still undecided.

The big surprise: John had already hit his number

When we ran the numbers for John, the result surprised even him.

He didn’t need to keep grinding until 55 - he'd already reached financial independence two years earlier.

Most people aren’t so lucky, but the process is the same:

- Calculate your ideal retirement income

- Assess your assets

- Identify the shortfall (if any)

- Create a pathway to reach your number

But in John’s case, we skipped ahead… to something even more powerful.

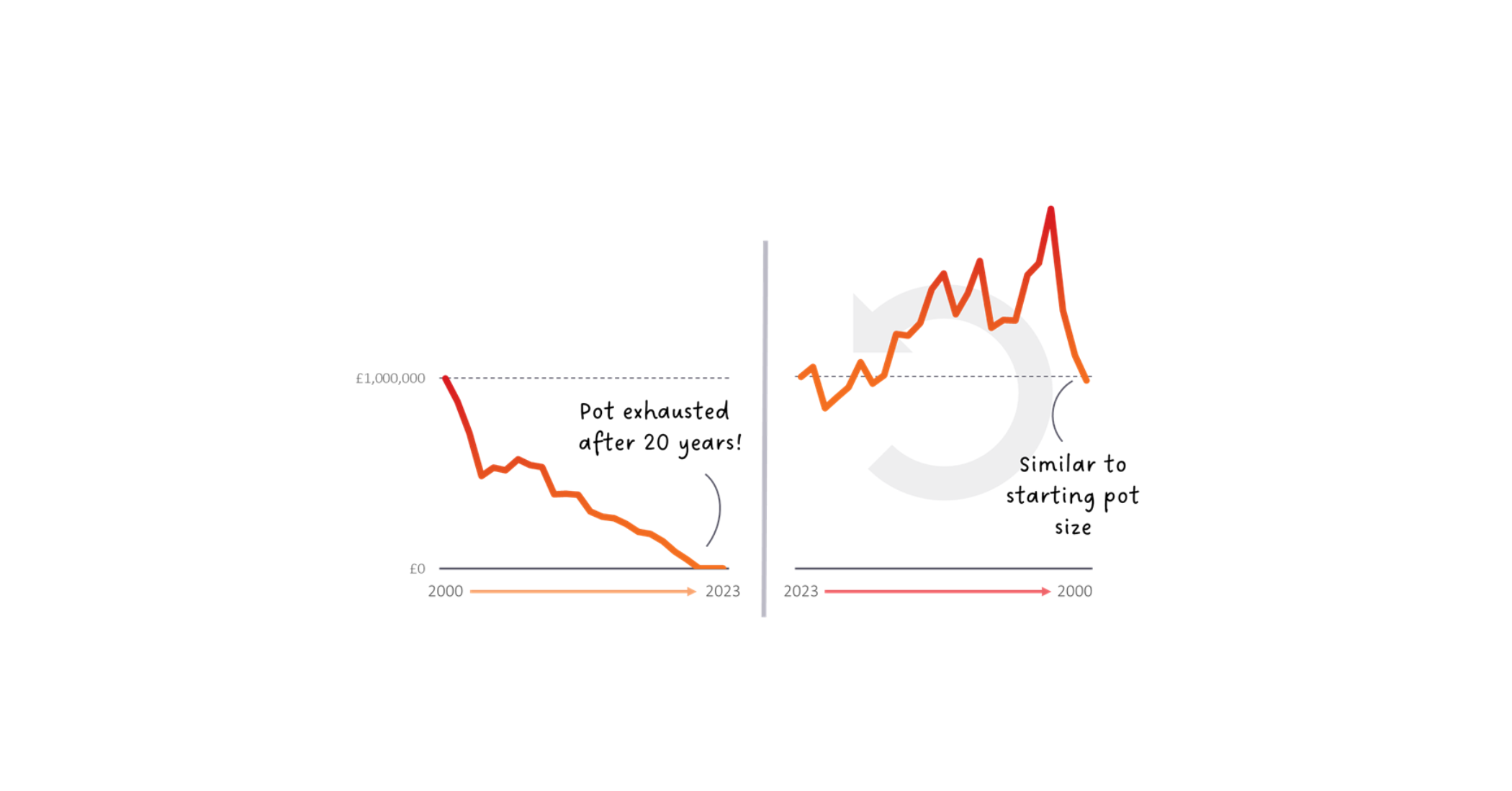

Smarter withdrawals: the “guardrails” strategy

The 4% Rule is helpful, but rigid. It doesn’t adjust for market conditions.

Whether your portfolio is up 20% or down 20%, you’re withdrawing the same amount.

That’s where guardrails come in.

Guardrails allow you to take more when markets are strong, and cut back slightly when they’re weak - all within a safe range.

This flexibility means your money can go further, with less risk of running out.

According to Morningstar’s “State of Retirement Income” report:

- A 60% equity portfolio using a fixed 4% withdrawal rate is relatively safe.

- But with guardrails, you could safely withdraw 5.4% instead of 3.8%.

That’s a huge increase in income, just by being a little flexible.

The bottom line: plan, adjust, and review

Here’s the moral of the story: A good plan gives you options.

Even if your numbers show a shortfall right now, that’s okay.

Many people are also supporting children, helping aging parents, or dealing with life’s curveballs.

Start by:

- Setting a goal, even if it’s rough

- Saving a manageable but slightly uncomfortable amount each month

- Investing wisely and reviewing annually

Over time, you’ll build momentum.

You may even discover, like John, you’re closer to retirement than you thought.

Final thought: don’t hope - plan

Yes, retirement numbers can be scary.

But guess what? Having no plan is even scarier.

Start with a target.

Reassess each year.

Let time and discipline do the heavy lifting.

And perhaps most importantly, once your financial plan is in place, you can finally start thinking about how you want to live in retirement — not just whether you can afford to.