“The individual investor should act consistently as an investor and not as a speculator.”

Benjamin Graham, the economist, investor and teacher of Warren Buffet

Before you start out on your investment journey, it's important for you to think about how to set investment goals. Identifying your investment goals and articulating them will give you clarity around what investment success means to you.

There are three key factors to consider when investing: your age, income, and lifestyle. Identifying where you want to be at each stage in life will define your appetite for risk and the amount you invest. You cannot invest what you don’t have, which makes your income an important factor that influences your investable assets.

The return from your investments could mean different things - it could be the money you use to pay for your children's education or your retirement. Understanding how to identify financial investment opportunities that align with your financial needs is crucial. Knowing what to know before investing - such as risk levels, market conditions, and wealth management strategies - ensures you make informed decisions that support your ideal future.

Once you work out what you aim to achieve by investing, you can move on to your next big decision: Do you need a professional financial adviser in Dubai to help you with investing, or do you have the time and technical expertise to test DIY (do-it-yourself) investing?

It’s also hugely important to get it right.

The 10 principles inside will help you take advantage of opportunities provided by efficient capital markets, and provide a systematic, time-proven way to reach your financial goals.

.webp?height=900&name=Pursuing%20a%20better%20investment%20experience%20downloadable%20asset%20(3).webp)

When considering overseas investments, what kind of guidance do you think investors need most?

From our experience, it's rarely about complex financial products or advanced trading strategies. Instead, investors primarily need guidance on how to avoid common pitfalls that could impact their investment performance. Unfortunately, the financial industry internationally has been designed to sell complexity, keeping you stuck and distracted from what truly matters. This leads to uncertainty, missed opportunities, poor decisions, anxiety and the dream crushing weight of ‘financial life drift’. But you don’t have to learn the hard way.

You can either struggle up the mountain alone, or take a trusted guide who’s already mapped and trodden the best path innumerable times. No fads, no hype. Just time-tested, evidence-based wisdom to help you seize the opportunities of wealth while avoiding its pitfalls.

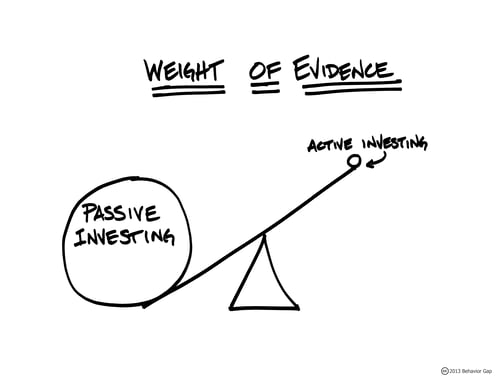

The opposite of active, is passive. Passive investment strategies have many names, like tracking or indexing, but our favourite name for it is evidence-based investing, because that's exactly what it is.

It’s investing based on evidence – not guesswork or speculation or baseless predictions.

Passive investing is a style of investing associated with exchange-traded funds (ETFs), trackers and index funds, where a fund's portfolio mirrors a market index, like the FTSE 100 or S&P 500, for example.

Passive investors:

1. Hold a basket of securities representing an index

2. Track and attempt to match an index

3. Remove the risk of trying to pick stocks, guess the market and outperform it

4. Spread risk, diversify, cut costs and improve returns

With passive investment strategies, there's a firm belief in the power of the markets (the great companies of the world) and one of the benefits of passive investing is a time-tested, evidence-based approach that allows investors to benefit from human ingenuity and innovation.

In financial economics there is a theory called the Efficient Market Hypothesis (EMH). It maintains that market prices reflect all available information and expectations. So a stock’s current price is the best approximation of a company’s intrinsic value.

Any attempts to identify and exploit stocks that are mispriced will most likely fail, because stock price movements are random, and largely driven by unforeseen and unforeseeable events.

Of course mispricing can occur, but there’s no predictable pattern for this.

So this hypothesis suggests that no active fund manager will ever be able to consistently beat the market over long periods of time – unless by complete chance, of course.

Therefore, stock picking, market timing and active investing cannot ever be reliably depended upon to add enough value to outperform a passive investment strategy. That’s the science behind what is actually, just common sense.

Passive investing means:

The approach you choose has to be right for you.

Passive investing isn’t perfect for everyone.

But the general consensus of professional opinion is that passive investing is the best approach for long-term investing.

The legendary active investor Warren Buffet also advises his wife and ordinary investors to put their money into passive investments.

The reason is that passive investing will provide average returns in an efficient way, at a low cost, whereas active funds in the longer term will, in all probability, provide the same average returns but at a higher cost.

The effect of compounding costs and charges on investment returns is substantial. Over a 10 year investment period, charges paid to an active fund manager are far greater than the costs of running a passive investment that just tracks the market.

Read more:

Science has changed every aspect of our lives including how we communicate, travel, shop and even invest. And the technology keeps improving. In the financial world, planners who don't keep up, often fall behind and sell their clients short. Before computers, there was no way people could possibly understand what drives the markets.

New technology allowed researchers to dive deep into the data to analyse the behaviour of security prices.

One such researcher was Eugene Fama. He developed a new framework to study financial markets, along with Kenneth French, and has been honoured with a Nobel prize in Economic Sciences for his work.

Their research underlies all of Dimensional Fund Advisor's thinking and helped develop the firm's process. Widely regarded as the "father of modern finance," Fama has brought an empirical and scientific rigor to the field of investing.

Transforming the way finance is viewed and conducted, which you may know as evidence-based investing.

Dimensional Fund Advisors is currently the eighth-largest fund company.

It manages assets exclusively for institutional investors and the clients of a select group of fee-based advisers.

Those assets were worth $794 billion as of September 2024.

So why haven’t you heard of them? The firm does no advertising and is primarily owned by employees and directors. This helps keep fund expense ratios very low.

DFA’s board members, directors, and consultants represent a “who’s who” in the world of financial economics, including Eugene Fama and other Nobel Prize-winning laureates, Robert Merton and Myron Scholes.

DFA does not develop or recommend investor portfolios. Instead, this work is left up to the planner chosen by the client. Development of highly efficient portfolio models requires a thorough understanding of Modern Portfolio Theory (MPT).

The principal goal of MPT is to achieve the greatest return for the amount of risk taken (or, conversely, to minimise the risk in a portfolio targeted to achieve a specific return). Doing so requires combining asset classes in the investment portfolio to achieve effective diversification.

The only free lunch in investing.

This is accomplished by measuring the correlation between specific asset classes that demonstrate a historically high rate of return and combining the asset classes in such a way that portfolio volatility is minimised.

Global diversification of the investment portfolio protects investors from a downturn in any single asset class. Domestic or foreign. DFA-based portfolios typically contain more than 9,000 securities in 44 countries.

Dimensional adds value over benchmarks and peers through a dynamic and robust investment process that carefully structures and implements portfolios to target higher expected returns. By evolving with advances in financial science, the firm has delivered impressive long-term results for clients. Which is why so many institutional clients and big companies use it. And why it’s a well-kept secret.

The driving factor behind Dimensional's outperformance comes from their ability to have an exposure that is more sensitive to the market, size, and relative price premiums. Of course, past performance is no guarantee of future success. But looking at the evidence helps put things in perspective—just take a look at any Dimensional funds review, and you’ll see why their systematic approach has been so effective.

A systematic investment approach is the way forward.

It keeps investors disciplined and patient even through the most challenging times, because they believe in the enduring power of the markets. They believe in their strategies and that their portfolio is working for them no matter what.

It's why during the volatile period of 2008-2012, US mutual funds saw outflows of $535.7 billion and Dimensional saw inflows of $34.4 billion. Having a strategy you trust is vital when you are investing.

It will give you the clarity and confidence needed to control your financial future.

You’re not alone if you’ve never considered investing anywhere other than your home country before. Many people are unaware of the offshore investment opportunities that exist.

What’s more, for some people, it’s a case of ‘better the devil you know’ when it comes to managing money and investing.

Because, as investment management companies say all the time, the value of any investment can go down as well as up, and so sticking to what you know reduces risk – at least in the minds of some investors.

However, often the reverse is true. Sticking to what you know could actually be limiting not only your choice but also the potential returns of any investment you make.

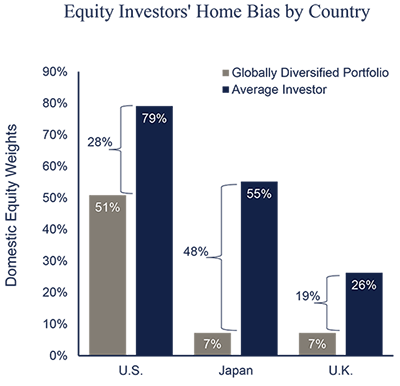

What’s more, limiting yourself to one market, especially if you’re living abroad, makes little sense. It’s called having a home-country bias. Understanding the benefits of international diversification is key to making the most of global markets and securing long-term growth. As the future of global investing continues to evolve, forward-thinking investors are recognising why investing internationally can be a game-changer for their financial success.

Let's take an example of a British man who has emigrated and lived long-term in Australia…

He can no longer take advantage of any of the tax-free offerings in the UK such as ISAs or pensions, he is living in a different time zone, he is earning and using a different currency day-to-day, and he is surrounded by a whole world of new financial opportunities.

Why would this man limit his investment choices to those available in a country he’s left behind?

And, having an awareness of the workings of two first world economies – Britain's and Australia’s – he is equally as unlikely to want to commit all his money to investing in Australia alone.

So, it makes no sense for him to have an old or a new home-country bias: he needs to explore the offshore investment opportunities open to him and get some advice from an investment management professional.

Therefore, for anyone living abroad, it makes sense to consider investing internationally.

The term 'offshore investment' is synonymous in many people's minds with illegally 'stashing cash' out of reach of the taxman. This is just a myth perpetuated by the media, and understanding offshore investment risks is crucial to making informed decisions.

Offshore investing and international investing are one and the same: the terms are used interchangeably, though some debate exists around offshore vs international investment differences in terms of regulatory frameworks. Offshore simply means a jurisdiction or country other than the one in which you're living. When evaluating offshore investment advantages, consider that these arrangements often provide access to a broader range of investment opportunities and potential tax efficiencies.

When we talk about investing abroad we aren't suggesting putting your money in a poorly regulated, semi-legal island state where there are no rules, and where you have no protection. It's essential to be vigilant about hidden fees in offshore investments, just as you would with any domestic investment vehicle. Offshore centres and international jurisdictions utilised by most senior international professionals and global families are those offering high levels of statutory consumer protection. These jurisdictions maintain strict regulatory oversight to protect investors' interests.

Investments made are completely geographically portable. And the investment management can be done easily, no matter where you're from, where you move to, or even where you want to retire or if you want to repatriate. Ultimately, by going offshore the jurisdictions available and solutions on offer, deliver senior professionals and their families the widest possible choice.

For investors seeking the best financial opportunities, a home-country bias can restrict returns significantly. Yet it’s still the case that most investors commit the majority of their funds to their own home market, mainly because of a fear of the unknown.

But, anyone who’s got an iPhone, a BMW, Gucci sunglasses or even an IKEA sofa trades globally, supports economies around the world, and diversifies their spending base.

So why not think the same way about investing?

Fidelity Investment looked into home-country bias in the US and discovered that American investors keep about 72% of their investments in-country, and about a third of all investors have absolutely no exposure to international stocks at all.

It’s impossible to quantify the restriction such an approach causes to an individual’s portfolio. However, the clever people at Fidelity produced a useful example of what such a restriction could look like in general terms:

Since 1950, a sample and theoretical portfolio of 70% U.S. stocks and 30% international stocks could have returned 11.4% a year. That’s 2% more than a straight S&P 500 portfolio, with 10% less risk.

If that illustration isn’t incentive enough to consider investing offshore, consider the fact that:

For non-professional investors, knowing where to look and invest, and precisely when to commit was all but impossible before the proliferation of exchange-traded funds and index trackers.

Nowadays it's incredibly easy for anyone to develop an international investment portfolio, and a comprehensive offshore investment guide or sage financial life manager can help you get started.

Read more:

Rental property vs. stock market investing

We'll call, learn about you and help you decide if we're a good fit. It's that easy.