“Time is the greatest money-making asset any individual can possess.”

Ed Slott

For senior international professionals

As a senior executive and part of a globally-minded family, you want a happy, healthy and prosperous life not just for yourself, but your loved ones too. You understand this will take hard work, dedication, commitment and perseverance.

Think about your goals as the destination. That’s only one part of your financial journey.

Next you need to know how to create a financial plan - a roadmap for your money that helps you achieve your goals. It keeps you and your family on track when life takes unexpected turns or when the markets test your resilience.

A financial plan is a comprehensive picture of your current finances, your financial goals and any strategies you've set to achieve those goals. Good financial planning should include details about your cash flow, savings, debt, investments, insurance and any other elements of your financial life.

So where do you begin? Here are four of the most commonly asked questions to get you started. They’ve helped others like you on their financial planning journey.

Financial planning for individuals is essential to achieving long-term financial security, whether you’re building wealth or preserving it. A well-structured plan helps you manage income, investments, and future expenses while ensuring tax efficiency.

For those with significant assets, financial planning for high-net-worth individuals requires a tailored approach, incorporating advanced investment strategies, estate planning, and wealth preservation techniques. With wise counsel and sage guidance, you can optimise your financial position, protect your assets, and secure the future of your and your family.

A personalised financial plan provides clarity, control, and confidence in your financial future, helping you make informed decisions every step of the way.

It’s also hugely important to get it right.

The 10 principles inside will help you take advantage of opportunities provided by efficient capital markets, and provide a systematic, time-proven way to reach your financial goals.

.webp?height=900&name=Pursuing%20a%20better%20investment%20experience%20downloadable%20asset%20(3).webp)

Long-term financial planning is what we advocate for. The key ingredients are time, patience, and discipline - all the time allowing the great companies of the world, through the stock market, to work their magic.

By systematically investing and staying the course, you benefit from compound growth, turning small, regular contributions into significant wealth over time. Avoiding emotional decisions and focusing on a well-diversified portfolio also helps weather market fluctuations. There's vast evidence to support this approach to financial planning.

With a clear plan, realistic goals, and a commitment to decades-long investing, you can build financial independence and enjoy the rewards that come with it.

For wealthy professionals living and working internationally, starting financial planning is about taking structured steps to secure long-term wealth. Here’s how:

1. Define your goals – consider short-term needs and long-term aspirations, such as retirement, property investment, or legacy planning for your loved ones.

2. Assess your current situation – understand your income, assets, liabilities, and tax obligations across different jurisdictions.

3. Create a wealth strategy – work with a financial life manager to optimise investments, pensions, and tax efficiency, using tools like cash flow modelling to forecast future financial needs.

4. Invest wisely – focus on diversified, low-cost investments for long-term growth.

5. Review regularly – adjust your plan to align with changing goals, market conditions, and tax laws.

Read more:

How to choose a regulated financial adviser in Dubai and the UAE

Senior international professionals are generally highly intelligent, well educated and handle complex operations themselves. So we often get the question - do I really need a financial planner?

Strictly speaking, maybe not.

Let's start off with two things.

Now, choosing a financial planner is a choice, because much like many professional services, it’s entirely possible to do it yourself.

The rules of building wealth and how to invest successfully are remarkably simple.

But it's extremely rare for us to review and not find a costly error which is why, having a sage financial planner, at the right time, may add immense value and convenience while paving the way for you to achieve your future financial goals faster and preparing for a financially secure retirement.

Financial planners can help prioritise the things that are most important to you and sift through the endless ambiguity on investing and insurance in order to find solutions that align to your unique goals. This is why financial planning is important.

It’s also about guiding you onto the right path and pulling you back when you veer off track, all while being an unbiased soundboard for any doubts or fears and reminding you to stay the course to achieve your long-term financial goals.

Good financial planners remove the drudgery so you have more time to do the things you enjoy.

Read more:

'Time is money' for most high-earning international executives.

Having a good financial planning expert on your side not only helps you spend your time doing the things you enjoy with your family, but more importantly helps you make the right decisions and stay on the right track to achieving your life's financial goals.

Canadian neuropsychologist and executive coach, Dr. Moira Somers, wrote a book called Advice that Sticks: How to Give Financial Advice that People Will Follow.

She gives several reasons why people need advice and the importance of successful financial planning:

1. Reduce complexity

There is a lot of complicated information out there. Experts help simplify this by understanding what is relevant to you and your individual needs.

2. Take action

Sometimes when faced with too many choices, people suffer from ‘decisional paralysis’. Having a financial expert will encourage you to make a decision.

3. Save time

Delegating a few of your financial responsibilities will free up more of your time and energy.

4. Offload unpleasantness

Getting someone to do the tasks that feel more like chores will relieve you.

5. Make someone else happy

Seeking advice can indirectly benefit other people – especially for major life events like marriage and education.

6. Increase confidence

During doubtful and challenging times, a financial expert will reassure you of your goals and plans.

7. Help make better trade-offs

A financial planner can help find the balance between what you want and what you can afford.

8. Receive encouragement

Changing your financial habits can be difficult. A financial expert can keep you motivated along the way.

9. Have someone to blame

Research suggests some people delegate primarily to waive responsibility and blame rather than to purely obtain good advice.

10. Feel safer

Studies show our brains process difficult financial decisions better when we receive advice from an expert.

So, to answer the question above, a financial planner can definitely help you reach your financial goals and live the lifestyle you always dreamed of having for you and your family.

Here's how this applies to high-earning executives in particular...

We found an insightful report titled: The Value of Financial Advice. It’s produced by the International Longevity Centre of the UK and supported by Royal London.

It examines the impact of financial advice on the ‘affluent’ and ‘just getting by’.

Here are the key findings:

Overall, creating a holistic financial plan that lays out a detailed course of action while factoring in all possibilities is easier said than done – but a good financial planner can help.

They’ll offer you support and guidance to save you from bad decisions.

Planning your financial future may seem simple after all. But it’s certainly not plain sailing when done alone.

Good, long-term financial planning requires long-term commitment in order to see results.

Jason Butler, author and former adviser, discusses why a 2-month spell with a personal trainer (or financial planner) won’t get you the financial results you desire.

And why not?

Because like physical fitness, achieving financial fitness is about adopting new and evolving financial planning habits. It’s about proper decision making and accountability but most importantly, it’s about being disciplined.

There are plenty of things a financial planner has to do on a daily basis.

It's about evolving new and regular habits, accountability and discipline to check with your financial decisions and keep you on track.

The most important recurring task for your financial planner is to re-balance your portfolio once or twice a year. It’s something you need to do but investors who manage on their own often fail to do so.

What re-balancing your portfolio means is selling something that has gone up in value, (which is counter intuitive) and buying more of what has fallen in order to keep the risk-return-ratio profile of the portfolio in check. This requires regular monitoring, planning and changes.

So to answer the question, financial planning is a lifelong process and not a one-time thing.

There is a great deal of work but the outset is amazing because it helps you achieve your future financial goals by devising a strategy that delivers results.

We're always excited about this question because the answer has a profound effect on you and your financial plan. Investing helps you live the life you want.

This might mean:

Bottom line, there are only two ways to make money: by working and/or by having your assets work for you.

Senior executives are usually high earners and part of successful families with a good amount of savings, so we often get asked this question since they believe they can reach their financial goals eventually without investing.

Let’s put it this way, if you don’t invest and you keep your money in cash you will never have more money than what you save i.e., your money isn't working for you. In fact, inflation actually erodes it.

By investing your money wisely, you are getting your money to generate more money - by buying and selling assets that increase in value.

Whether you invest in stocks, bonds, property, or any combination, the objective is the same: to make your money work hard for you and to protect your future purchasing power. For this reason alone, it's critical you get financial and investment planning right.

And the simple truth is that many people don’t.

Investing done well implies:

Whether your financial goal is to send your kids to college or to retire on a yacht in the Mediterranean, investing well is one of the only vehicles that will get you and your family there. This is why you should invest and make it the most important part of your financial planning.

Let's talk now about financial planning for life and the first part of your financial planning process - getting a clear idea of what actually helps you reach your financial goals.

There are seven key financial planning tips that can positively influence your wealth in any given year.

We often talk about things like low-cost, systematic investing and asset allocation, but there are other big financial ideas that should guide your investment decisions too. It's all about financial planning for the future.

Let's dig deeper into seven of them:

Compounding can help you reach your financial goals sooner and it highlights that time can be as valuable as money (possibly more so). Even young adults can turn a modest $50 or $100 into significant wealth with time on their side.

Of course, compounding works best when high investment costs are avoided or large losses caused by a lack of diversification. It’s also why a globally diversified portfolio using low-cost investment funds can really help. Inversely, compounding can also work against us and deter our financial plan. If we have large debts that we’re paying off over many years.

Whenever we focus our money on a single thing, we’re giving up something else. We don’t pause long enough during impulse shopping moments to consider the trade-off that’s involved and the opportunities we’re missing out on.

We’re often drawn to news of latest releases, like the recently launched iPhone with its impressive array of features.

But what if we thought about the price of that iPhone a little differently. Could that $1000 be better spent on a memorable trip or experience?

Or invested to reap a possible $4000 return in the long run?

Our lives are a constant tug of war between the demands of now and those of tomorrow. And, if we’re perfectly honest with ourselves, in this game, our current wants and needs usually prevail.

This is why we often fall short of our financial goals and move away from our financial plan.

We land up settling for a retirement we didn’t dream of or a college for our children that was only fifth on our list.

Luckily, there are ways to make investing a habit. Like choosing an automatic investment plan as part of your larger financial plan that deducts money from your account or salary before you’re tempted to spend it.

A financial planner also helps keep you in check to and to make sure you don’t stray from your long-term financial goals.

Our entire financial planning is centred around our income-earning ability. For at least four decades, our regular pay cheques allow us to:

We need to spend each pay cheque wisely.

Allocate appropriate amounts to our needs, wants and savings. It’s a great way to gage how much you spend on important things and where you can cut down on unnecessary costs.

There are some financial risks we simply should avoid. Like the lack of financial planning in the event of our premature death. Without one in place your family could be left in a very difficult situation.

The smartest way to avoid this is to buy enough insurance that covers your family.

But there’s another type of ‘insurance’ we need to consider and that’s for the possibility of living longer than expected and outlasting our assets.

Purchasing income annuities that pay a lifetime income will help us make ends meet if we do.

Today’s world makes it easy to not own anything since we have the option to rent everything. In some instances, this makes perfect sense, especially for expats who do not plan on living in one country for very long.

However, renting means lining the pockets of someone else instead of your own. If you see yourself living in the same city for at least five years, then buying a house is a good idea.

And if ever you decide to move you can sell and possibly earn a handsome profit.

We are all creating financial plans and investing for that ultimate goal – retirement and we can’t afford to fail. So why do so many of us fall short?

The simple answer: not knowing how much is enough. If our goal is to accumulate as much as possible, we may take reckless risks in order to grow the biggest financial pile.

It’s why it’s so important to diversify and balance your risk. If the markets crash today, tomorrow or next year at least you’ll have a cushion to soften the blow.

One of the most important parts in financial planning is putting in motion an investment strategy. But the question we are asked time and again is, when is a good time to start investing and can you time the market to find the best window of opportunity?

Let’s answer this question using evidence and facts so the results can speak for themselves.

Imagine this scenario…

Two brothers, let’s call them John and James both receive a £100,000 inheritance from their grandfather in 1986 and invest it into the FTSE All-Share Index. Over the course of 33 years, both he and his brother keep their investments, albeit with different investment strategies.

John invests the money and leaves it alone, choosing a long-term approach and ignoring whatever happens in the markets. James, on the other hand, enjoys the thrill of a more active approach – selling when the market is low and buying when it’s high.

Who lands up with the larger investment?

Because of his constant buying and selling, James misses out on 10 ‘best days’. His investment value is worth only half of John’s.

Like Aesop’s famous fable ‘The tortoise and the hare’ a slow and steady approach ultimately wins the race.

The real cost of timing the market

One of the biggest risks of trying to time the market is being out of it when an unexpected rise takes place. Often this happens immediately after a correction, meaning that by staying invested, you have the best opportunity to capture growth over the long-term.

Your view should be time in the market, rather than timing the market. Even missing out on 10 ‘best days’, could chop your investment in half. Market timing is a pure gamble, summed up beautifully by Matt Hall in his book, Odds On…

“Most investors try to pick the right investments and time the market’s moves, but their chances of winning are as slim as their chance of beating the house when they walk into a casino. The deck is stacked against them.”

Every year, global events shape our countries and our economies. A lot of people wait to start investing and try to time the market. Here are 30 examples of 'why not to invest'.

But happily ignoring these events (in terms of our investments, at least), Is the best course of action.

No one knows what the markets will do, which means market timing doesn’t work. It also means you miss out on the power of compounding which needs time to work its magic and to get you closer to achieving your financial goal.

Remember, Warren Buffett made 99% of his fortune at 52. Maximising growth comes down to patience, time and compounding. Too often, investors are fed a bunch of comforting lies, conflicting or biased information that work against them. That’s not what we do. We prefer to be radically transparent and honest while creating a financial plan for you.

But if you haven’t started an investment portfolio, there’s no better time than now. You’ll never be younger than you are right now.

The best time to invest is as soon as you have the money.

One of our clients was recently about to make a significant investment.

Considering market twitches and fear ahead of the US election result, he asked him to pull the plug on his investment.

Of course, our team said we can do that - but also offered some wise, evidence-based counsel and gave him a chance to change his mind.

After discussing the deeper concerns at play, he went ahead and invested, and is doing incredibly well as a result.

We're not suggesting we can guess the market. No one can.

We're trying to show you that all but the most experienced investors should be supported and advised by a proficient investment fiduciary…

Otherwise their emotions will negatively impact their investment performance.

Ed Slott

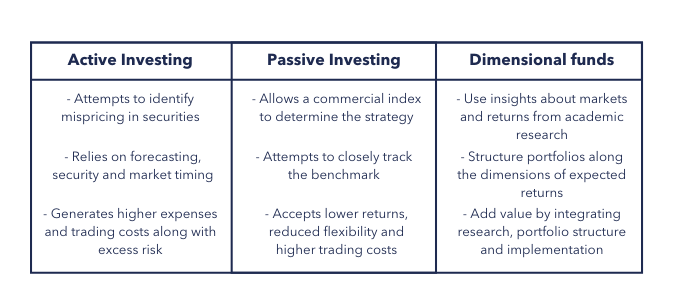

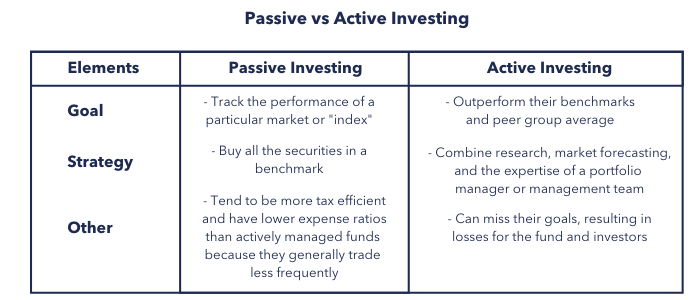

When it comes to crafting an effective investment strategy, there are generally three approaches for investors. For each, you should question whether your strategy is really working for you, and helping you with your financial plan.

Here’s a quick look at these different investment approaches in the image below.

Active investing is a guessing game where money managers pick the ‘winners’ for you. However, finding the winning investment manager is a challenge and it is difficult to distinguish between those who are skilled and others who are lucky.

If you look at the stats over the years you’ll see the dismal number of active managers able to beat the market. It’s this very revelation that led to the introduction of passive investing.

Contrary to active investing, it doesn’t try to beat the market and has no ‘expert’ managing your money, instead, it tries to capture the market return.

Despite being an easy and successful way to invest, Dimensional Fund Advisors (DFA) offers an alternative. The next step in the evolution of investing with the potential to get better results.

Unlike passive investing, DFA does not rely on a commercial index, it relies, instead, on the Nobel Prize-winning work of Eugene Fama and Kenneth French. DFA focuses on capturing the key ‘dimensions’ that exist in the marketplace.

It’s this evidence-based approach that makes their funds so successful and the international executives who use them, very happy.

Unlike passive investing, DFA requires investors to work with a select group of financial planners which it approves of, trains and has direct access to the funds to help them stick to their financial plan.

They believe that investors will have a better investment experience this way. So that’s it. There are basically 3 ways to invest and hopefully this sheds some light on their differences and which is right for you and should be a part of your financial plan.

The financial planning world can be surprisingly complex and full of people who have their own interest in mind and not yours, making it very important for you to choose your professional financial planner carefully and to be aware of the many different practices prevalent amongst different types of ‘adviser.’

For example, a commission-based, life insurance-based salesperson is the anthesis of a regulated financial planner or fiduciary.

There are 6 principles which any kind of influence is based on. These were discovered by Professor Robert Cialdini, author of the book: Influence: The Psychology of Persuasion. These influences affect many different sectors and industries.

But we mainly want to discuss how you can avoid falling for such trickery while choosing your financial planner.

We’ve all heard the line: ‘Trust me, I’m an expert’.

Authority bias is powerful because it can drive people to behave in ways that are often at odds with reason. It can get you to invest in something your gut instinct is warning you against.

We all know the story of Bernard Madoff who ran the largest Ponzi scheme in the world. He is behind the biggest financial fraud in U.S. history – estimated to be worth $64.8 billion.

New York Times reporter Diana B. Henriques, said about the scandal:

“If you ignore the simple checks, legitimacy can be hidden under layers upon layers of untruths and obfuscation.”

Don’t take things on face value. Expertise is not a bad thing – but do your research, ask to see qualifications, certifications and records and check client testimonials are real by contacting the people before signing on the dotted line.

Do you want to be rich, live in your dream house and make it all happen?

“What if I told you I have the financial product to make all this a reality…Want to know more?”

See what I did there?

It’s what I call the ‘yes’ train and it’s one of the more notable tactics used in tele-sales ads back in the day (You know, the ones selling magic stain removers).

It’s a bit of mind trickery. A salesperson will start you off on a series of questions that you’ll answer ‘yes’ to, inevitably painting a picture where all your dreams can be realised, making you think this person truly understands you and your financial needs.

By the time they switch to selling you the product you’re so used to saying ‘yes’ that you find it hard to say ‘no’. The commitment and consistency bias makes it difficult to change your position. Remember this as you make financial decisions in the future.

‘Crypto: everyone else is doing it and making loads of money’.

Sound familiar? While following the crowd can have its benefits, there are a few dangers to look out for.

Social proof in investing contributes to volatile asset prices. These trigger market booms and busts, just a quick look back at Bitcoin and you’ll see what we mean.

When it comes to investing, it’s best not to follow trends. Instead, opt for long-term diversified portfolios that will minimise risk and safeguard your finances during ups and downs in the market.

When someone does you a favour, do you feel the need to repay them?

This is reciprocity bias. Financial tricksters can use this bias to get you to buy their products without any concern for your financial planning or future goals. A game of golf at a prestigious club, a free gift when you provide referrals, all of these may encourage a need to return the favour.

It’s important to not be misled by supposed acts of kindness since these won't make up for a bad financial decision.

Friendship is a common deception to ordinary investors. After all – it’s easy to trust people we like.

Friendship can make you let your guard down but that can adversely affect your finances. Regardless of how charismatic, trustworthy and friendly you believe someone to be - do your due diligence before signing on the dotted line. Compare the data, products, performance and fee structures and read unbiased expert reviews to give you a better perspective.

This supermarket tactic is also used by financial salespeople.

‘Special offer for a limited time’ or ‘Free bonus units’. These are done in an attempt to force you to make a decision under pressure, which means, you’re far more likely to rely on the emotional part of your brain than the rational one.

If you feel you may be persuaded into purchasing a product you’re unsure of, getting a second or even a third opinion never hurts. It may even save you money down the line.

You can give us a call and we’ll happily give you an unbiased review for free. It might give you a clearer picture of what you’re being sold.

Financial planning can be difficult as is. Ensuring you make the right decisions becomes all the more important for your financial future.

Another aspect to beware of while starting your financial planning journey is hidden costs and commissions. High-earning international executives often become the target of financial 'salesmen' who disguise themselves as financial planners and confuse you with technical jargon so you don't understand what exactly you're paying for.

Hidden costs are toxic and while many countries are taking steps to reduce them, investors are not completely out of the woods. Costs have become more important than ever. They play a significant role in performance and returns but with them decreasing, playing fields between funds are narrower and using cost as a sorting mechanism becomes harder.

Understanding exactly what you’re paying can be challenging.

Working with a regulated financial planner will give you an added advantage. They’ll be able to reveal charges and fees you may have missed or were concealed in the fine print. They lure you in with lofty promises of free advice or high growth, dangle current uncertain events at you, but like doctors, lawyers, accountants, etc.; professional financial planners (fiduciaries) never cold call. They’ll wait to hear from you first, because everything should begin and end with you.

They’ll listen intently to your goals, recommend a strategy you’re comfortable with, provide clarity on why it works for you and give you the confidence to believe in it and leave it alone. This is the secret formula to a successful investment experience.

Hidden fees and commissions can devastate returns, leaving expat investors with far less saved than they’d hoped for. A black hole in their financial futures.

You need to be made aware of this, so you can make better, more informed decisions. Your financial future is far too important to be left in the wrong hands. If you’re unsure of anything, or simply need to know where to start, give us a call.

We are proudly fee-only financial planners who put investors first before anything else.

Ever heard of an investing black hole?

Essentially, your money is sucked in and never seen again. Don’t believe me? Read this client’s story.

Our client, Andrew, is all too familiar with them.

He moved to Dubai from London in 2016. His company set him, his wife and children up handsomely, with relocation, housing, schooling and healthcare costs all paid for.

With more disposable income, he hoped to invest more and possibly retire early to spend time with his family. Unfortunately, as a busy, high-earner in Dubai, he became an easy target for unsolicited sales calls.

A charismatic financial salesperson contacted him, offering to meet at a nearby coffee shop to chat about his investment options.

“You need to take full advantage of your tax-free salary and cash in on the current market volatility. Transferring your life savings into an offshore bond is the best decision for your future.”

Andrew was won over.

He withdrew his £600,000 pension and invested all of it into the offshore bond recommended by the trusted salesperson.

However, his investment hadn’t grown in two years – despite a raging bull market. Those inflation-beating returns he was promised were nowhere in sight. With his retirement and his family’s financial future on the line, he desperately sought a second opinion.

After scrutinising his investment, the results were shocking. He unknowingly agreed to a 10-year lock-in period, paid his ‘financial planner’ an initial 7% product commission and 4% on the underlying investments…

An eye-watering 11% (£66,000) disappeared into the abyss on the day he transferred his money. But this was only the tip of the iceberg for him.

He was charged:

It gets worse.

If Andrew withdrew his funds within the initial charging period of 10 years, exit penalties would apply.

It was clear the damage was done. But, truth be told, the damage wasn’t irreparable.

The Middle East is littered with similar stories caused by a financial services industry that’s systemically broken.

While he couldn’t make up contractual losses, he could move on.

The journey would be difficult.

It would begin with a simple chat about him and his life, not about money…

Cases like Andrew’s often start with an unsolicited phone call from a ‘financial expert’.

They lure you in with lofty promises of free advice or high growth. They dangle current uncertain events in front of you. But like doctors, lawyers and accountants, professional financial planners (fiduciaries) never cold call.

They’ll wait to hear from you first, because everything should begin and end with you.

They’ll listen intently to your goals, recommend a strategy you’re comfortable with, provide clarity on why it works for you, and give you the confidence to believe in it and leave it alone.

This is the secret formula to a successful investment experience.

Having the correct retirement savings strategies helps you make the right financial decisions that get you closer to your ideal future. Understanding the benefits of saving money for retirement, putting money aside monthly can help you reach your retirement goals a lot faster and can act as buffers in case of emergencies.

Here are some of the ways retirement savings can be beneficial:

Retirement savings act as a safety net in case of financial crisis, with protecting retirement savings being crucial for long-term security.

The importance of saving for retirement early cannot be overstated - compound interest works its best magic with time and the earlier you start saving the better.

Retirement savings can act as an emergency fund in unforeseen situations.

These savings, overtime, can also help you clear out debts and outstanding loans that overall help you reduce monthly expenditure and interest payments.

Segregating monthly income is the method used to decide on an amount you can save on a regular basis. This can help you identify your spending habits and rectify them, enabling you to save even more to reach your ideal future faster.

Executives at higher levels are usually required to move or travel a lot as part of the job, and we receive questions from expats and clients from around the world who need a financial planner. Ever so often, those high-earning executives living as expats, choose a local financial planner over us. We can certainly understand the urge to look into the whites of their eyes, after all, you should be working with them for a very long time (Not to mention putting your trust in them to guide your financial journey).

But choosing a financial planner purely so you can meet face-to-face brings a unique set of risks. Facts don't change our minds. Friendship does.

James Clear wrote a blog about why so few innovations become a commercial success. He concludes that, as humans, we are creatures of habit, we dislike change and resistance to it is human nature.

Disruption conflicts with our established beliefs which historically we’ve relied upon for survival. It can alienate us from our tribe. What has this got to do with where your financial planner is based?

Consider this.

1. Fiduciary: investor ratio

The earth’s surface area is approximately 510 million km². If, like me, you’re English and both happy and used to UK standards of regulation/protection. You have 130,395 km² of inhabitable English space, put otherwise, you have 509,869,000 km² of expatriate living space in which you need to hope a well-qualified, regulated and ethical face-to-face financial planner lives.

The overseas talent pool for well-qualified financial planners is small. The number of well-regulated and transparent firms is perhaps even smaller. The chances of you living in an area where you have face-to-face access to a highly regulated, knowledgeable financial professional is slim.

The chances of both you and the financial planner staying in that area (let’s say within 500 km²) over the number of years a relationship exists, is likely very small. Finding an independently certified fiduciary is not only the best thing you can do for your financial planning but the best way to ensure your peace of mind that your financial planner is truly on your side.

2. Cost

Commission-based salespeople are normally happy to travel (even by plane) so they can either sell you a product, churn your funds or press you for referrals. Even if you think you’re not paying – the products they sell more than cover these costs.

Ultimately it is you who pay these costs through the often-hidden charges on these products, a second time through under-performance, and a third time through exit penalties!

Would you prefer seemingly ‘free’ advice from face-to-face salespeople OR to reduce your costs, increase flexibility and maximise your returns?

After all, costs compound over time and diminish your returns.

3. Company vs. individual

The traditional financial services industry promotes ‘lone wolves’. Typically self-employed salespeople who try to sell as many products as possible in order to make the biggest commission.

By their nature, many of these ‘salespeople’ also move cities, companies or even countries fairly often. You’d have to start all over again and find a new financial planner. However, when you work with an ensemble practice – your relationship is with the firm, not a person.

Yes, people come and go, but your relationship remains with the firm and the team within it. This gives you added protection and peace of mind, knowing your financial future isn’t in the hands of a single person.

4. Regulation doesn’t work if you move countries

As an expat from country A and living in country B, you may move back to country A after a few years or move on to a new country entirely.

The regulatory system will likely not support you and many people fall between the cracks. If you choose a local financial planner, you’d have to find a new one in each country you’re in, making the process confusing and tiresome.

An international firm will likely be able to work with you wherever you are in the world. The clients we have today, have comfort in knowing we’re with them for the long haul.

Lets start by answering what a regulated financial planner means:

In the UK, the FCA requires all financial planners hold financial qualifications equivalent to at least a Level 4 qualification within the national Qualifications and Credit Framework. This means the financial planner must be educated in financial advice more or less to university degree level to practice, and have controls and is regulated by a legal authority as a firm in order to look after clients.

It never ceases to amaze us at AES International, the number of people who ask us why it is important they use a regulated financial planner. It is tempting to answer this with another question: would you use an unlicensed dentist, doctor, lawyer or any other professional? A better answer, though, would be that seeking professional advice is absolutely critical to avoiding catastrophic disaster when it comes to financial planning, too.

So why is it so imperative you receive regulated financial advice?

There are countless reasons why you should ensure that the advice you receive is given by a regulated financial planner.

Here are four key ones:

1. Protection

To be regulated, a firm needs to be a registered legal entity. It needs financial resources (known as capital adequacy), professionally qualified individuals, and systems and controls that are adequate for looking after clients. This means that you can have confidence that the company will not simply disappear.

2. Fair treatment

Regulated firms must follow strict rules ensuring the advice they provide is suitable for your needs, appropriate, and fair. In the UK this falls under an Financial Conduct Authority (FCA) initiative called “Treating Customers Fairly”.

3. Qualified advice

The analogy about the doctors and dentists may seem obvious – I am sure you also wouldn’t want an unqualified electrician to wire your house, an unqualified mechanic to service your car or an unqualified plumber to fix your pipes. However, the international financial marketplace is littered with unqualified salespeople. It simply does not make sense to trust something as critical as your financial well-being to someone with no qualifications. Qualifications matter.

4. Fair recourse to complain

By using a regulated financial planner you will have a proper course to ask for redress if you feel a product has been mis-sold to you or you have lost out financially from having received poor advice. Regulated firms have well documented, careful, comprehensive and prompt complaints handling procedures. If you are not happy with their response you may be able to complain to an Ombudsman (independent adjudicator), or in some cases directly to the regulator who will investigate to ensure you get fair treatment.

In the event something does go wrong with the product you have taken out or the advice is wrong, you may be eligible for compensation from the firm, and more importantly, even if the firm is not in a position to pay, there is still recourse available. As an example, advice given by an FCA regulated firm in the UK is covered by the Financial Services Compensation Scheme (up to a specific limit): for regulated investment advice, for example, you can claim compensation up to a limit of £50,000 if a firm is unable to pay). None of this is available from an unregulated firm.

Regulated firms also have to have professional indemnity insurance in place which may pay compensation if they have made an error. An unregulated firm will not have this cover in place leaving clients exposed to a great deal of unwelcome risk.

In the right situations, a financial planner can make your life easier and help you live your life the way you always wanted. Hire a financial planner if:

1. You’re a high earner

If you’re a high earning senior executive supporting a globally-minded family (£500,000 pa+), chances are you are time poor. You may have the ability to save a lot of money but not know the right way to take advantage of the various structures and facilities available to you.

Private banking, Lombard lending, cash-flow planning and evidence-based investment – can all protect and multiply your wealth.

2. You have a high net worth

Higher-net-worth individuals (£1 million+) also have a unique set of financial issues.

From coordinating large balances spread across different types of accounts, to advanced estate and tax planning strategies, there’s a unique skill set involved in efficiently managing an especially large amount of money.

A boutique, fee-only financial planning firm dedicated to helping high-net-worth individuals should be your first port of call.

3. You’re nearing or in retirement

There are big financial questions that retirees and near-retirees have to answer.

These might include: "Am I financially ready to retire?" and "What’s the best strategy for withdrawing from my various retirement accounts in order to both meet my needs and make my money last as long as possible?"

These questions have a big impact on your retirement lifestyle and your family's future. That’s why having a financial plan for lifetime security is essential—it ensures that your wealth is structured to support you throughout retirement, no matter how long you live.

None of these questions are easy to answer on your own. Each has a number of nuances and strategies that can be difficult to understand or implement without the help of a professional who knows this stuff inside and out.

Most people in this stage of life could at least benefit from a one-time consultation with a financial planner who specialises in retirement planning.

4. You’re starting a family

Getting married and having kids both introduce a lot of new financial challenges.

From joining finances, to managing the new costs of having children, young families have a lot of financial responsibilities on their plate.

Then there is estate planning, life insurance, university…

A good financial planner will help you navigate and prioritise all of these responsibilities so that you can create a secure and enjoyable life for your family both today and in the future.

5. You have a very specific planning need

Certain situations call for specialised knowledge that many people, and for that matter many professionals, don’t have. Expert witness, divorce, borrowing a lot of money etc.

Caring for a family member with long-term care needs involves a much different set of planning strategies than most people encounter, for example.

If you find yourself in a unique situation like this, finding a financial planner with specialised knowledge in that specific situation can help you make the right decisions. AES specialises in helping successful international professionals with their financial planning and tailor it to help them achieve their individual financial goals.

Successful executives usually end up paying a lot more in taxes than they owe since they are not advised correctly. Tax and trust planning is an important part of your financial planning process and should not be overlooked.

It’s important to consider whether international trusts have a role to play in your offshore financial planning.

Whilst taxation is a fact of life, there is no law in any land that says you must pay more than you owe! And yet, that is what so many expats end up doing, simply because they have failed to plan effectively, or perhaps don’t even understand their liability for tax.

If you’re a British expat – or have assets in the UK – your beneficiaries may be liable for UK inheritance tax for example - potentially on your worldwide estate.

And there’s more to tax than just inheritance tax, there’s capital gains, income tax at home and abroad. Your financial planning needs to look at ways you can legally mitigate your tax burden, so that excessive taxation doesn’t undermine your overall financial plan.

Trusts can play a very important role in reducing tax liability – but because there are many different types of trusts, it’s critical to ensure you have the right one in place and that’s where expert planning really could pay for itself.

Risk depends on a variety of factors - individual to you, the investor. Understanding this can make a massive difference to your financial goals. Of course, there are complex mathematical models that attempt to quantify risk, but these on their own are never likely to be enough. Risk factors to be considered in financial planning often come down to a host of other factors, like what is happening in your investment portfolio, what your consumption needs are at a specific time or what’s happening with your career and income.

Sometimes you will hear risk being defined in terms of volatility, or the degree to which an individual investment goes up and down in price. But this is an over-simplification and doesn’t take into account all the individual elements that come into play. For instance, if your stock portfolio is gyrating wildly from day to day, this is not going to mean much if your investment horizon is 20 years or more. Ultimately, what you are worried about is a permanent loss of capital.

Finally, in assessing risk it’s important to distinguish systematic risk from non-systematic risk. The first is something you can’t avoid; it goes with the territory. For instance, shares are considered riskier than bonds and for that reason they offer a higher expected return. Non-systematic risk you can manage. If your entire portfolio was in banking stocks ahead of the global financial crisis, that was concentration risk – a type of non-systematic risk. You could have managed that by diversifying across different sectors.

There are other types of risk, as well:

The overall rule is that you want to take risks that are related to a reward.

In general, markets reward risk over the long-term, provided you are sufficiently diversified and disciplined and pay attention to factors within your control, such as costs and taxes; and of course having a financial planner that you trust can make the world of a difference to how much clarity, confidence and control you have, even in the most uncertain and challenging times.

World events can of course have an impact on the markets. Businesses and their leaders can see their lives and investments disrupted when this happens.

You may be feeling uneasy about this volatility and the impact it might have on your financial plan and investments.

Market volatility can test even the most confident investors. For some, though, they understand the opportunity this presents.

Focus on what's important

It’s the best advice at times like these.

For those with a financial plan and strategy matching their capacity for risk…

The questions to ask are these:

The answer to both of those questions should be a resounding No.

The fact that markets are lower than they were a little while ago shouldn’t affect your financial plan at all. The problem with market volatility is that it tends to divert our focus and we land up focusing on the wrong things.

When you’re thinking about falling markets, the uncertainty surrounding Brexit, the strains in US-China trade relations, etc. they all seem very important.

If, instead, you focus your mind on your long-term financial plan, which should be designed to withstand these episodes, you’ll have a much healthier sense of perspective.

Part of the answer to avoid being affected by market changes and volatility lies in choosing the right asset allocation through a strong financial plan.

But here’s the rub – the right asset allocation for one person could be entirely wrong for you. Many un-diversified investors are feeling the discomfort and exposure for simply not preparing for the worst.

Here's why.

The financial markets can be unpredictable. Yet, fund managers often promise the equivalent of endless sun which rarely ends well.

Luckily there’s an answer to this cycle of unrealistic hope.

It’s called diversification.

Diversified investors will not hang their hopes on one asset class, sector, country, or stock. They’ll spread their exposure across shares and bonds, different markets, industries and currencies.

Diversification increases the reliability and predictability of returns. Looked at another way, it smooths the way and reduces the sudden bumps in the investing road.

The ups may be less spectacular, but the downs will also be less stomach-churning. Like well-prepared travelers, diversified investors are ready for a range of outcomes.

If the stock market is roaring ahead, they can have sufficient exposure to enjoy the benefits of that growth. But when shares are down, they can also be protected under the relative shelter of government bonds.

Diversification works because different parts of financial markets aren’t perfectly correlated. As one asset class goes down, another may go up. Shares (a growth asset) and bonds (a defensive one) are the classic example.

But diversification also applies within asset classes. In your stock portfolio, you can spread your risk across sectors in your financial plan. Instead of putting everything in technology, materials or financials, you can have a bit of everything.

And instead of sticking to one country, you can diversify internationally across developed and emerging markets.

You can diversify within a bond portfolio as well, spreading your holdings between government and corporate bonds, between long-term bonds and short-term bonds and bonds of higher credit and lower credit.

And in case of an unexpected event, you can have a portion of your investments in cash.

Ultimately, diversification works because you are giving yourself more choices, consequently reducing the impact these twists can have on your financial planning and income.

Along with hidden high fees, behaviour is the main reason why investor's don't make the returns they should.

As international chartered financial planners and wealth managers, it's vital that we communicate this message effectively.

How do you avoid making the common investment mistakes that other investors make?

Know the way you naturally think and then do the opposite, and if you can't, hire a chartered financial planner to manage your emotions and your investments so that your financial plan stays on track to reach your life goals.

Investing forms a major part of your financial planning and can be both the reason you reach your financial goals and the reason you don't, if done incorrectly.

The traditional financial services industry is designed to benefit them and not you. Like a casino – the system is designed so the ‘house always wins’. Speculation is encouraged as each trade generates more fees and commission. The industry thrives on misinformation, using sales tactics and lofty promises to lure you into poor decision-making.

That was until the evidence-based investing philosophy and indeed evidence-based financial planning, began.

Today, it’s become a global challenger to the status quo of Wall Street banks and international brokerages.

A growing movement based on Nobel prize-winning research, evidence-based investing delivers better results. Academically proven, peer-reviewed and grounded upon fact not fiction.

This philosophy captures the returns of the market through a low-cost, diversified and long-term investment strategy.

Always using scientific evidence to maximise investment returns while minimising risk from market downturns.

In other words, whatever you decide to do, make sure you have an evidence-based reason for doing it, and always be prepared to amend your plan when the evidence necessitates a change.

The result?

Happier, more fulfilled investors who finally have a sense of financial freedom. An end to the anxiety and worry stemming from a broken traditional financial services industry.

'With great power, comes great responsibility' could not be more true for high-earning international professionals, there are too many things to take care of and very few hours in a day. But having a good financial planner in these situations will help you stay calm and give you clarity, confidence and control over your finances and ideal future.

If you stick to these five basic principles of investing, we promise you won’t go far wrong:

1. Keep costs down

Keep costs down by using low cost exchange traded funds (ETFs) or index tracking funds where possible.

Most good financial planners will also have negotiated discounts on actively managed funds, and can pass on the discounts to you, which can also help keep costs down.

2. Diversify

This is perhaps the most complicated part of investing, and getting this right can make a big difference over time.

You may need some help getting started with this. But one thing it is commonly agreed you must do is diversify.

If all of your money is in one asset class – equities, for example – and that asset class falls out of favour, your portfolio will take a big hit.

By spreading your investments around different assets you will help minimise some of the downturns and take advantage of more of the upturns.

3. Invest regularly

Investing is a discipline. You need to have a plan and stick to it. Once you know how much you can invest each month, invest it without fail – regardless of what markets are doing (see point four).

4. Don’t react to, or try to time the markets

Reacting to market movements isn’t investing… it’s trading, and is a full-time job for some people – most of whom still get it wrong most of the time, according to the evidence. Equally, no one can time the markets with any degree of sustainable success. Don’t try and find a needle in a haystack, own the haystack and buy the whole of the market. Stay invested for the long-term.

5. Don’t be sold to

Once you have created your investment portfolio, stick to it.

Do not let anyone make you stray from your path with the unlikely promises of “guaranteed” or “amazing” returns. There is no short-cut, just persistence and discipline.

If it sounds too good to be true, then it almost certainly is.

But, if you remember these five golden rules and hang tight, even in worrying times, your financial plan should still be on track.

Of course working with a regulated financial planner will make this much easier. A financial planner has many roles, not only do they help you decide on the right portfolio for your ideal future, they also help you stay on track when the markets test you, manage your emotions when you're unable to and save you from making any decisions that may eat away at your returns.

A financial planner will be as invested in your future as you are. If you're looking for one to work with you along your investment journey, get in touch.

Is your retirement financial planning causing you anxiety? Do you neither have the time nor the inclination to get back on track? That’s where a financial life manager comes in.

Financial planning for tomorrow must start today if you hope to maintain a good lifestyle into your retirement. Pension plans, regular savings plans, and residential property are the most common forms of retirement investment strategies among international professionals, and all these investments have their place and a part to play in providing for your twilight years.

However, the best retirement investment strategy should start with solid foundations, and this is where financial planning, with the help of an independent financial planner using lifetime cash flow modelling, can help.

The starting point for a conversation between you and your financial planner is not a financial product but a holistic conversation starting with how you spend your current income. A review of your bank statements and credit card bills will quickly reveal how you live and where your financial resources are spent.

This can be broken down into the five areas showing the choices you make with your money:

This exercise can be very revealing and helps clarify for you and your financial planner how you are living and where your current priorities lie. By looking at each category of spending, you'll often be able to streamline your finances, reduce unnecessary spending, and take those crucial first steps to financial freedom.

It's worth noting that the five uses of money include income taxes because, at AES, we encourage clients to consider the impact of taxes on their global retirement fund strategies when they return home, even if they're currently living abroad.

For example, wealthy Brits will pay a 45% top rate of income tax, the French 45%, and some Americans over 50%.

Once you have completed your expenditure and budget review, the next step is to discuss with your financial planner your goals, ambitions, and dreams. Most people’s goals include one or more of the following areas: family, career, health, friends, and travel.

Your financial planner will then be able to help you calculate the financial cost of each goal and put each of your goals into a lifetime cash flow planning model, which will show your existing assets, income, debts, and future growth in easy-to-understand graphs.

If you're wondering how much money you need to retire, the answer depends on many factors—including your goals, expected lifestyle, and investment strategy. That’s why working with a financial planner can give you a clearer picture of your financial future and ensure your retirement is secure.

One of the most important concepts for investors to grasp is compounding. It’s the principle on which most great fortunes are built; it’s far more powerful than you might imagine, and an important part of your financial planning.

Warren Buffett has always been vocal about his love of compounding. It’s perhaps the number 1 reason why he remains one of the world’s richest. His fortune isn’t due to being a good investor, although he is, it’s because he’s been investing since the age of 11.

Many of us become ambitious savers only around the age of 30 when we’ve broken free from an entry-level job and start earning more money. But Buffett understood the power of compound interest long before that.

By the time he was 30, he had a net worth of $1 million, which is equivalent to $9.3 million today. He was in the 99.99th percentile. What if he only started investing at 22 years of age? Using today’s net-worth percentiles and adjusting them for 1960s-era inflation, he would be worth around $24,000 at the age of 30.

If he went on to earn the same returns that he did, he would only be worth $1.9 billion. That’s 97.6% lower than his actual net worth of $81 billion. Don’t get me wrong, $1.9 billion is still a hefty sum, but the point I’m making is that the difference of just 11 years (in terms of compounding) has had an astronomical impact on Buffett’s net worth.

It’s so easy to overlook the power that something small can have, like a child starting to invest the little they earn. Over time, that little will become a lot. It will compound into something big, possibly beyond their wildest dreams.

So, harness the power of compounding. If you haven’t started investing yet, don’t put it off any longer. And if you want to give a child a financial head-start, just invest some money for them. Simply leaving it invested will produce extraordinary long-term results.

As an international senior professional, comprehensive financial planning involves a few additional areas.

There are the 6 key considerations that go into comprehensive financial planning for expats and international executives like you:

1. Cash flow planning or cash management

One of the best routes to strong budgeting - and ultimately to stress reduction - is to prepare a cash flow plan.

It will help inform your spending and savings decisions - and importantly, flag up future problems before they arise.

Your cash flow plan will take into account your income, assets, outgoings, and other present-day information, and predict your future cash-flow in order to predict how much money you’ll have coming in and going out at any given point in your life.

Your forecast will help you plainly see expenditure, so you can better plan.

The aim of cash management like this is to help you feel more confident about your finances, and have sufficient disposable income to enjoy throughout life – i.e., so you balance spending today - and then saving for growth for your future income needs.

An additional benefit is that many cash-flow forecasts created by professional financial planners will help you spot potential shortfalls or issues before they occur.

If your plan anticipates future difficulties, such as not having enough to retire on, you’ll have plenty of warning to make alternative arrangements – like cutting spending and investing more today, so you can retire sooner and on a better income.

A strong side benefit of having a solid cash flow plan is that you demonstrate effective budgeting - which may give others confidence in your financial management, thus potentially helping you secure loans, funding, mortgages or overdrafts.

When we create a cash flow plan for you, we factor in extensive data. For example, we plan for the worst, plan for multiple different scenarios, consider fixed and variable costs and returns on investment…

And then we create your financial road-map for your future prosperity.

2. Family and protection

Are you part of the sandwich generation? In other words, those who are financially responsible for both younger and older family members? Over 1 million Britons are.

If you have a single or dual financial responsibility as an expat, it’s critical to consider how your loved ones would cope if you were to suffer an incapacitating illness or even die.

There are very few countries in the world with as generous a social support system as the UK’s. And fewer still where foreign residents are eligible for financial support in times of hardship.

As a result, you need to think not just about growing your wealth, but also about protecting your family with insurance.

There’s a range of insurances and protections available that can help cover your family and give you the peace of mind that your loved ones will remain looked after, no matter what.

In some scenarios, protecting before investing may even make the most sense. Your financial plan will help you determine your priorities, and how best to meet obligations and challenges to ensure your loved ones’ security is protected.

3. Estate planning

Having worked hard to build wealth and security for yourself and your family, the last thing you want is for an over-eager taxman to come along and rob your beneficiaries of what’s rightfully theirs when you pass away.

The fundamentals of estate planning and wealth protection or preservation need to be included in any financial plan – no matter how much or little you believe you’ll have to leave behind.

Inheritance taxes are only one part of the problem – as an expat your estate may be at risk of unfavourable laws of succession in the country in which you now live – or hold assets. Dubai is a classic example where the laws of succession are unfavourable for most expats.

A solid financial plan focuses on protecting your wealth for today, tomorrow and your future generations.

When we, as financial planners work with you on your financial plan, we will look at estate, gift, and generation-skipping transfer taxes (as well as the income taxation of trusts, estates, and beneficiaries) for example.

We’ll cover strategies for making of present and future interests, the effective use of assets providing death benefits (e.g., life insurance, commercial annuities, qualified retirement benefits etc.) The use of family businesses and investment entities as estate planning tools, the use of non-charitable actuarial techniques (e.g., qualified personal residence trusts and private annuities) in estate planning, valuation planning and estate freezing techniques.

We can even consult on post death estate planning issues and about providing liquidity in an estate.

4. Investment planning

Investment planning is the process of matching your financial goals and objectives with your financial resources, and it’s a core component of financial planning.

As a process, investment planning begins when you’re clear on your financial goals and objectives - it helps you match your financial resources to your financial objectives.

There are quite literally thousands of different investment paths you can take as an expat…by helping you set out clear and measurable goals, your financial planner can match the most suitable mixture of investments to each specific goal in the most efficient way.

5. Retirement planning

Retirement is one of the most important life events many of us will ever experience. From both a personal and financial perspective, realising a comfortable retirement is an extensive process that takes sensible planning and years of persistence.

Even once it is reached, managing your retirement is an ongoing responsibility that lasts throughout your life.

While all of us would like to retire comfortably, the complexity and time required to build a successful retirement plan can make the whole process seem daunting.

However, retirement planning can often be done with fewer headaches (and financial pain) than you might think – what it takes is some homework, an attainable savings and investment plan, and a long-term commitment.

6. Offshore banking

Offshore banking is suited to high earning professionals with around £250,000 to invest. It is an important step to take when managing wealth.

Arguably, opening an offshore bank account is the most important step for any expatriate to take when managing wealth.

Keeping your money in a country other than the one in which you live means if anything happens, you know your money is being held securely in another location.

Keeping your money outside your old home country too will help you avoid paying taxes unnecessarily.

Another benefit of having an offshore bank account is that if you move countries again, you won’t have to move your money from one country to the next – because that is a major inconvenience.

As an expat, by banking offshore, you can have all your assets arranged in one place.

Expat financial planning requires a lot of time and effort but with the right financial planner it can be the aspect that helps you reach your financial goals faster.

Even for international high-earning executives, planning around your finances is an ongoing process that lasts a lifetime. It may begin when you receive your first pay cheque, or when you take out a mortgage and need to plan how you’re going to pay it back!

As you live your life, and opportunities, promotions and challenges present themselves, so your financial plan will need to be adapted and honed on a fairly consistent basis.

Financial planning will involve maximising the money you earn, saving and investing for growth and stability, setting money aside for your long-term ambitions - like a house purchase or retirement, and sometimes just juggling your finances to meet all your expenses.

Every financial plan is therefore as unique as every person on the planet.

A core part of financial planning is cash-flow forecasting. That includes estimating the timing and amounts of cash inflows and outflows over a specific period. And cash-flow forecasts can factor in different scenarios, to help you make the best decisions for your wealth at any given time.

For example, a cash flow plan for a retired person who has money saved and invested in pensions and funds might look at the tax implications of drawing different amounts annually. It could also look at whether it’s more tax effective to deplete inheritance taxable assets first, leaving pension funds ‘til last.

Cash flow planning, or forecasting, is usually part of financial planning undertaken by a professional financial planner for anyone with more complex financial decisions to make. The forecast is a financial illustration – that draws out your options, and the likely consequences of the decisions you could conceivably make.

When you’ve found a professional financial planner with whom you can work, here are the 6 financial planning process steps for international senior executives like yourself to ensure you have a successful financial outcome:

1. Establish your goals in life – your financial planner will work to understand your short, medium and long-term ambitions. We believe in goal-orientated financial planning at AES, to ensure you achieve everything you set out to.

2. Work out your assets and liabilities – your financial planner will list your assets and liabilities today, and using cash flow modelling, they will look at future potential scenarios to help structure your plan to grab opportunities and avoid problems.

3. Evaluate your current financial position – how close are you to achieving your goals? Are you on track for any of your ambitions, are you opening yourself up to risk or excess tax? Your financial planner will look at every scenario with you.

4. Develop your plan – having determined your goals, identified any threats or opportunities, and with a thorough understanding of you, your financial planner in Dubai will create your road map for achieving each of your different goals.

5. Implement your plan – once this map is discussed, honed and agreed upon, the plans will be put in place so you can make the changes needed and ensure your financial future is successful.

Our financial planning clients are typically living and working as senior international professionals or affluent families managing complex wealth at least £1,000,000 or equivalent to invest.

Your financial planning process begins with a holistic approach to your financial life:

Fiduciary, basically means trusted. You'll get the same advice as our family members.

This sounds like common sense but it’s practice is extremely uncommon. In fact, AES was the first and remains the only firm in the AMEA (Asia, the Middle East and Africa) region to meet this standard of excellence.

You will never be as young as you are today and compounding works best when time is on your side. Major market events like the current market fluctuations will happen year after year and timing the market to find the best time to start investing will rob you of your financial rewards. The best time to start investing is always NOW.

Regulated financial planners are authorised to give you advice and recommend suitable financial products and investment options for you. They are regulated by a governing body to ensure that you get the right financial advice, that's best suited for your needs.

Your financial plan needs to be re-evaluated a minimum of twice a year.

If you feel like your current financial planner in Dubai (or elsewhere) doesn't have your best interests at heart and is not helping you reach your financial goals, you can always request a Discovery Call. This is a no-cost, no-obligation, diagnostic review of your existing situation (minimum value of 1,000,000 GBP or currency equivalent).

It looks below the surface - and gives you the inside information you need to make informed financial decisions and get the best results.

Technology enables us to continue business as usual no matter which part of the world your based in, so you are free to chose your financial planner globally as long as you chose a regulated financial planner.

Lifetime financial planning, put simply, means having a tailored financial plan for every stage of your life, focused around your individual needs, no matter which stage you start from, in order to help you live your best life and achieve all your financial goals and aspirations.

Markets tend to reward investors for the risks they take. The higher the risk, the greater the long-term reward could be. Remember, taking more risk doesn’t guarantee higher returns; that’s the nature of risk.

But if you stay invested and are able to resist the temptation to dip in and out of the market, you should eventually be rewarded for the additional risk you take, and that can have a positive impact on your financial plan.

We'll call, learn about you and help you decide if we're a good fit. It's that easy.