Funding your life goals: How much is enough?

Winning the lottery or start saving early are two ways to get to the average £1m plus that a couple that live in the UK will need to meet all their basic needs of getting married or entering into a civil partnership, buying a home, raising children and retiring.

The £1m figure is revealed in new research from the UK bank, Lloyds, but the reality for most of us is that we'll need much more than that. We take a look at why.

Where you live will determine how much you actually need to acquire in order to meet your life goals. Different parts of the world have vastly different costs of living, as our series of blogs has shown. The Big Mac Index is well known its help in comparing purchasing power across the globe.

But £1m seems like a good starting point for financial planning, so what else did the survey of British couples find? The cost of getting married was just £11,168 and the average 3 bedroom house in the UK is now £175,000, according to the survey. But these figures mask huge regional differences, of course. London and SE property prices are on a different level from those in - say – Scotland or Wales.

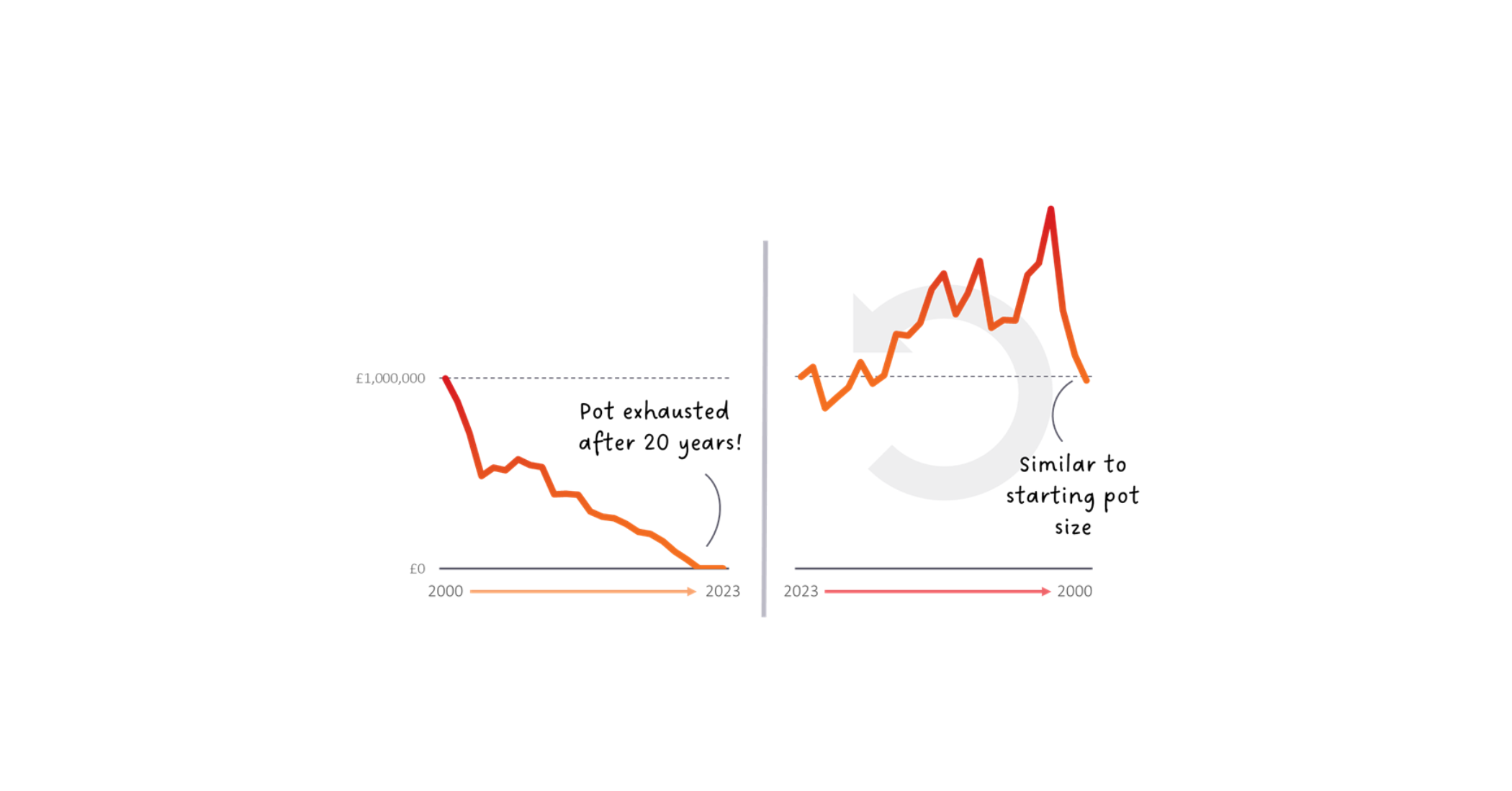

The biggest cost, according to the survey, though was actually the amount of money needed to form a basis for retirement: £685,000. This for most people is an enormous sum to consider and one we covered in a previous blog. The trouble is that in one important sense, this average figure isn't correct. This figure represents the amount needed for retirement today: it takes no consideration of the future. For example, a 60 year old retiring today who started saving 30 years ago would have seen inflation over that 30 year period of nearly 200%, based on figures from the annual Retail Prices Index (RPI) from the Office for National Statistics, which could mean that in ten years time even £1m might be enough, on average, to fund all your life goals.

So if we don't win the lottery, what’s the best way to make sure we have enough ? The answer, perhaps sadly for some, is to save and to start early. The research found that those people who started saving early in life are over 50% more likely to own a property and investments in their 40s and 50s. Of those 45 to 64 year olds of today who started saving seriously before the age of 25, more than half now own their own home outright. Similar figures are also true for stocks and shares investors.

So now we know the cost of funding all our life goals (on average). For many of us, it's an answer we don't want to hear because the current average figure of £1m feels enormous. It probably means we will have to go without, or delay some purchases we want to make. It probably means feeling boring and saving regularly from as early an age as possible. None of these things fit neatly into todays world of 'I want it, so I'll get it now' culture, encouraged by advertising. But the reality for most of us is that we won't build the next big technology start up company or win the lottery to help us along the way. Even if we did, the discipline of financial planning would put us in a better place when we collected our pay-out!

The answer therefore is to start saving as soon as possible, once the basic requirements of living and paying off any high cost debt, are covered.