If protesting were an Olympic sport, France would own podiums like Zeus on Olympus.

Ferry workers have blocked the Eurostar channel tunnel line. Railway strikes are commonplace.

Farmers have dumped manure, rotten vegetables, eggs and milk in front of traffic.1

But today, the French aren’t crying over a load of spilled milk. About a million angry people spilled onto the streets in April.

Imagine you’re a sixty-year-old factory worker. Your daily grind might be a mental root canal. You have 730 days until you can retire with benefits. But then the government says, “We’re sorry. You need to grind it out for longer than you thought.”

France isn’t the only country increasing its retirement age. And it won’t be the last.

To figure out why, stroll through a playground. In the 1960s, they were filled with giggling children on swing sets and slides. But by the 1970s those children began to dwindle. By the 2000s, playgrounds were like towns after the local mine had closed. Today, they’re almost empty.

No, those missing kids aren’t playing video games at home. They just weren’t born.

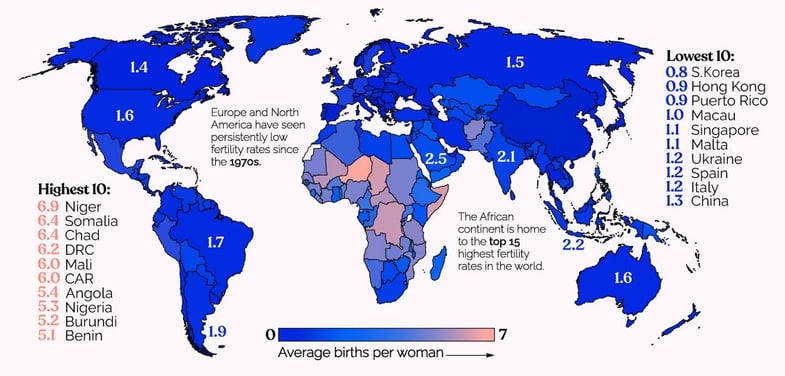

To maintain our population, women need to have an average of 2.1 children. But fertility rates have plunged every decade since the 1970s. In 2010 a whopping ninety-eight of the world’s countries had fertility rates below 2.1. By 2021, that number had grown to 124 countries. By 2030, 136 countries are projected to have a lower than replaceable birth rate.2

This isn’t just a rich country thing.

As shown below, women in South America are averaging just 1.7 children. Even India (despite the 2.1 shown below) has recently dropped to 2.0.3

Low birth rates are seeds of population decline

Source: The Visual Capitalist: World Bank Data

Source: The Visual Capitalist: World Bank Data

Meanwhile, as our population ages, more grey heads are strolling parks and watching birds. Auntie Joan and Uncle Tom are living longer too. They don’t smoke. They have access to better medical treatments, and they understand the importance of healthy food and exercise.

But the tax-paying population (which supports those retirees) is getting proportionately smaller. That’s why countries are raising their retirement ages.

According to a study commissioned by the nonprofit group, The Club of Rome, trends suggest the world’s population will grow from its current 7.96 billion to about 8.6 billion by 2050… simply as a result of today’s population living longer. As people die, many won’t be replaced. At that point, the global population is expected to decline.4

The average human is older today than at any time before. And there are fewer kids in diapers, playing on swings, and starting their first jobs. That means property prices and the stock market will likely be affected.

If you measure success based on GDP, you might say this is bad for everyone. But there are silver linings and things we can do.

For starters, your diaper-clad children or grandchildren should have an easier time affording their own homes.

Sure, we could open our world to migrants from the planet Vulcan. But if that doesn’t happen, property prices should stop shooting up. They might even level or begin to decline. Supply will exceed demand.

The stock market could limp as well. There will be fewer people buying Toyotas, toothpaste and Teddy Bears. Business profits won’t soar as high. Financial columnist Scott Burns and Economist, Laurence Kotlikoff talked about this in their book, The Clash of Generations: Saving Ourselves, Our Kids and Our Economy.5

They argued that if stock returns will be lower you’ll need to do several things right.

First, buy less stuff. This will benefit the environment and free up more money for you to invest. If, over the next 30 years, stocks earn lower returns, your retirement could be saved if you invest more money.

For example, over the 30 years ending May 31, 2023, a diversified portfolio with 70 percent in global stocks and 30 percent in global bonds averaged 7.37 percent per year.6

What if, over the next 30 years, such a portfolio averaged 6 percent instead of 7.37 percent? I’m not saying that will happen. But it might. And if it does, it would be smart to buy fewer things and invest more than you otherwise might.

Kotlikoff and Burns also warn how painful mistakes could be. That’s why they recommend sticking to a diversified portfolio of index funds. Don’t waste money on gambles like crypto-currencies, private equity, hedge funds, actively managed funds, individual stocks and market timing.

By investing more money, intelligently, you will be prepared.

You can’t control what investments will rise or fall. But you can control your spending and how much money you invest.

That’s better than a picket line, no matter where you stand.

Sources

- The Local France: The Craziest French Protests You’ll Find Hard to Believe

- The Economist: The Economics of the Great Baby Bust

- Science: India Defuses Its Population Bomb: Fertility Falls to Two Children Per Woman

- The Guardian: World Population Bomb may never go off as feared, finds study

- The Clash of Generations: Laurence Kotlikoff and Scott Burns (MIT Press)

- AES International: The Difference Between Growth and Value Stocks Over Time

Andrew Hallam is the best-selling author of Millionaire Expat (3rd edition), Balance, and Millionaire Teacher.