I’ve lost count of the number of times a client tells me they’re investing in ‘bonds’ from their bank or ‘broker.’

I’ve also lost count of the amount of times these have turned out to be structured products and not bonds or ‘fixed income’ instruments at all...

To the less well-informed/ordinary investor, structured notes make perfect sense.

Advertised and 'sold' as the ideal vehicle to help you benefit from stock market performance whilst simultaneously protecting you from bad market performance.

Who wouldn't want upside potential with downside protection?

But, all that glitters isn’t gold…

Although appealing at first glance, the lack of insight into the probability of different outcomes occurring, (and the complexity of modelling these outcomes) combined with high, hidden and embedded costs, makes them a poor choice for long-term investors and their portfolios.

Academic rigour is always a wise starting place for the analysis of any asset class when considering its inclusion within your

future plan.

Here's a summary of such analysis for structured products:

| Economic rationale | Data insight | Adequate reward | Portfolio role | Robust products | Risk management |

| Payoff defined | Little research | Probably not | Poor fit/gamble | Counter party risk | Complex evaluation |

Hoping an unpredictable event doesn’t happen isn't a sensible wealth-creation strategy.

As you’ll see below, a systematic portfolio offers similar protection from losses and the potential for far greater upside gains, making structured products mostly unnecessary for building portfolios.

Why then are they sold by banks, brokers and other sales and marketing machines?

The appeal of structured products

Structured financial products or structured notes, including structured deposits (the latter of which has some FSCS protection while the former has none), involve contractual commitments from issuing banks to investors, ensuring predetermined returns based on specific market conditions.

They are debt obligations with an embedded derivative component. In other words, they invest in assets via derivative instruments. A five-year bond with an options contract is an example of one kind of structured note. The value of the derivative is derived from an underlying asset or group of assets, also known as a benchmark.

The initial appeal to the lay investor lies in the potential for profit or a full refund.

For instance, an investor might be guaranteed 50% of any increase in the UK equity market index over the next five years, with a principal refund if the market falls below the current level.

However, certain conditions, such as a market decline exceeding 15% at maturity, may alter the 'money back' promise, resulting in proportional losses.

The popularity of structured products has surged in recent years, especially during periods of near-zero interest rates.

In the UK in 2022, approximately 900 publicly offered structured products were issued, totaling around £1.5 billion. However, navigating these products isn't as straightforward as it may seem.

Let's begin with the promise of 'money back'.

It's true, the same amount is returned after a specified period, but it's only in nominal (pre-inflation) terms, diminishing some of your purchasing power.

As well as this, reliance on the issuer's financial stability is crucial (when Lehman Brothers' collapsed during the financial crisis, it left $18 billion in outstanding structured notes).

The complexity of payoff structures has also grown, each featuring a variety of upside and downside scenarios with even more attached complexities.

Many structured products these days involve multiple reference market indices (known as 'underlying'), increasing both complexity and risk.

This complexity means investors need to understand not just the promised payoff structure, but also the probability of each potential outcome, a job often requiring intricate probability modeling or a deep knowledge of option theory and pricing - and not simply something you can read in any marketing material.

As you've probably guessed however, it's something the issuer is likely to understand.

This information gap allows for lucrative pricing markups in the derivative strategy underpinning the payoff promise.

Recent research indicates markups on structured products with multiple underlyings are around 5%, compared to 2% for single underlying structures.

Unfortunately, investors bear this cost, hidden within the offered payoff structure.

Call risk, credit risk, lack of liquidity, high costs, hidden risk and inaccurate pricing are disadvantages.

The investor always pays.

The issuer always gains.

Investing in structured products seems largely driven by behavioural biases, particularly loss aversion.

Human beings feel the pain of losses twice as much as they feel the joy of gains, and investors are no different.

So when you hear there's a chance for positive returns from exposure to equity markets, for example, without putting your original capital at risk - that's extremely appealing.

Less well-informed investors typically like simple concepts and so may hear they get growth without capital risk, but not fully understand the products, risks, costs and pay-offs involved.

But, these characteristics already align with a traditional portfolio

Take a systematic portfolio, with 60% in equities (tilted to value and small-cap stocks) and 40% in bonds.

This globally-diversified portfolio provides direct access to asset classes at a lower cost.

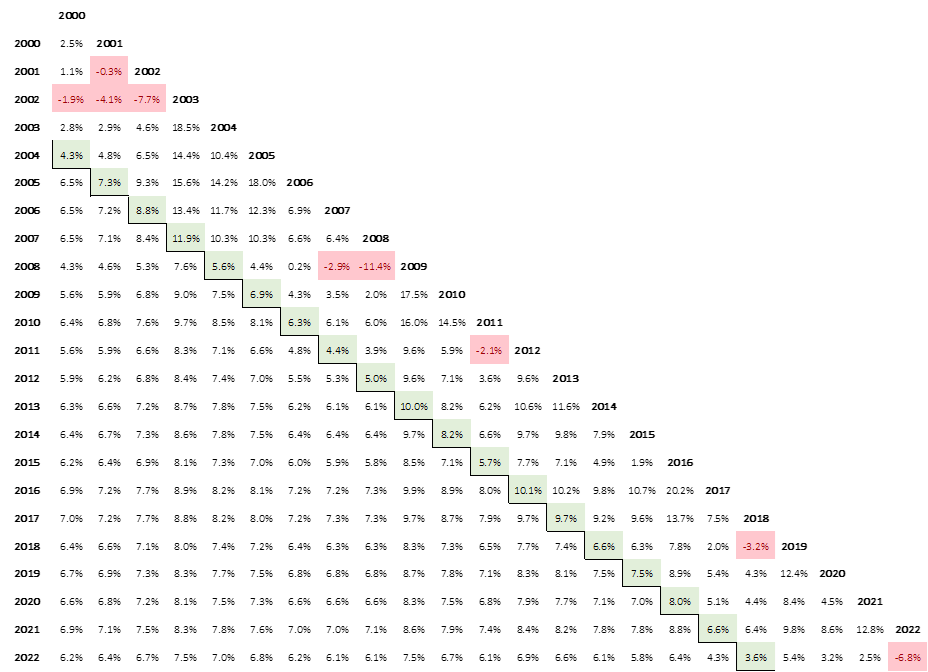

The chart below shows the hypothetical performance of such a portfolio. It protects the initial investment (usually what those who buy complicated and expensive structured products want), while also offering the possibility of making gains.

From 2000 to 2022, the annualised 5-year nominal return ranged between 3.6% (19% cumulative) and 11.9% (75% cumulative). Even after deducting product fees of, say, 0.35% p.a., all periods yielded strong positive nominal returns.

Data: Morningstar Direct ©. All rights reserved. Annualised portfolio returns (no costs deducted) – for illustration purposes only.

How and why are these structured products or bonds still being sold?

Firstly, they're lucrative for those selling them, because of high, concealed fees (and when someone's income relies on them not grasping better alternatives, it's challenging for them to realise this).

Secondly, human behaviour is influenced by both fear and greed.

The 'guarantee' of a payoff resonates with these emotions, making it easy to sell these types of products to those who may not be as financially savvy (retail or 'normal' investors).

With any purchase, buyers are responsible for examining and evaluating the quality, condition, and suitability of the goods or services on offer.

With structured notes, unfortunately, issuers are not typically obligated to disclose every detail about them. The onus is on the investor to exercise diligence and prudence.

It's wise to heed the following counsel from one of the most astute institutional investors in recent decades and former Chief Investment Officer of the Yale University Endowment, David Swensen:

"As a general rule of thumb, the more complexity that exists in a Wall Street creation, the faster and farther investors should run."

Our advice is to keep it simple.

Wise investing isn't just about hitting home runs.

It’s also about avoiding the strike-outs.

Invest in a globally diverse, low-cost portfolio of the world's best companies, and leave it alone for as long a time as possible.

You can learn more about structured notes in this article on Investopedia.

Looking for a second opinion on your situation?

For peak health and well-being, it's advisable to have an annual checkup with your family doctor. They'll ask questions, listen to you, do tests and follow a process. To keep you on track, they'll provide you with a plan.

Think of AES' Second Opinion in the same way.

Since 2004, AES has been committed to helping our clients pursue peace of mind through our collective insight, wisdom, and perspective.

Our Second Opinion will audit your current financial health, help you prioritise what needs attention and create a plan of action...

To ensure your goals and capital are aligned and you remain on track to reach your and your family's ideal future.

Would you like to schedule a call?