One of the most common reasons people give for refusing to invest in stocks and bonds is it reminds them too much of gambling.

After all, both are uncertain, involve risk and may result in a loss.

But avoiding financial markets for that reason is a bit like refusing to eat because it could potentially cause heartburn.

Like it or not, we all have to take risks in life.

What career you follow, where you decide to live, who you marry are all calculated gambles, based on incomplete information and an uncertain future.

The point is not to avoid these risks but to manage them.

How do you do that?

It helps to take pointers from people who manage risk for a living – people like professional card players.

Annie Duke, a cognitive scientist turned poker champion, has written an excellent book on the lessons she learned during her own 20-year gambling career.

Image credit: PokerNews

Image credit: PokerNews

In Thinking in Bets: Making Smarter Decisions When You Don’t Have All the Facts, she points out ways we can stack the deck in our favour when making any choice.

It’s a book that holds important lessons for investors, executives and anyone else who faces uncertainties – which is to say, all of us.

Here are four smart ways to immediately improve your own decision-making.

1. Admit what you don’t know

According to Duke, most of us can radically improve our ability to make good decisions simply by no longer thinking in terms of all-or-none alternatives.

It’s far better to evaluate our beliefs in terms of probabilities.

Rather than saying we believe this or that, we should think of our opinions as bets on reality – we’re 60 percent sure of this or 90 percent confident of that.

This may feel unnatural at first.

Whether the topic is Brexit or global warming or the outlook for the stock market, most of us prefer to examine a few key points, come to a conclusion and then adopt it wholeheartedly.

A far better approach, says Duke, is to look at the evidence, admit our uncertainties and put a number – even a rough number – on how confident we are.

This pays off in several ways.

For one thing, it forces us to examine both sides of an issue.

Consider your choice of which political party to support.

There’s a big difference between saying you’re absolutely convinced your party is best and saying you’re 70 percent sure.

In the latter case, you’re more likely to ponder other viewpoints and stay alert for new information.

You’re also more likely to change your mind and update your opinions.

We all hate to admit we were mistaken.

It’s far easier to say that our level of confidence has shifted from 70 percent to 40 percent.

When it comes to money, mental flexibility can help prevent many common investing mistakes.

- People who think in all-or-none terms often bet huge amounts on a single stock.

- They refuse to sell bad investments because of the faint chance they will bounce back.

- They remain committed to sectors that have done well recently and neglect to consider whether those areas are now overvalued.

Thinking in terms of probabilities can help shield you from all those errors.

2. Ignore short-term results

In her consulting work, Duke asks the people she’s working with to think back to the worst decision they made in the past year.

Almost always, she says, the examples they come up with are actually their worst outcomes.

Poker players call this “resulting”: evaluating the quality of a decision based on the quality of the outcome.

But a bad outcome doesn’t necessarily mean the decision behind it was wrong.

In poker, you can play any single hand perfectly and still lose – not because of bad decisions, but because of bad luck.

Conversely, you can win a big pot, not because you played well, but because you were extraordinarily fortunate in how the cards happened to come out.

Resulting can be dangerous if it tempts you to second-guess yourself and revise your long-term strategy based on short-term outcomes.

What really matters is the quality of the decision.

If you’ve collected information from the best possible sources, looked at potential alternatives, and allocated resources accordingly, you should stick with your strategy no matter what the immediate results happen to be.

This is particularly important when it comes to investment management.

Top financial thinkers, like Nobel prize winner Eugene Fama or Princeton professor Burton Malkiel, are remarkably united when it comes to the right way to invest.

They recommend putting your money into a well diversified portfolio of low-cost index funds that tracks major stock and bond markets around the world.

Research by independent arbiters such as Standard & Poor’s shows that this strategy beats the vast majority of actively managed money over any five-year period.

But here’s the catch: in any one year, it’s likely to lag behind the hot sector du jour.

The challenge for most investors is to keep their eyes on the long-term rather than getting caught up in whatever is leading the parade right now.

3. Put emotions on hold

The stock market can be an exciting place.

Sometimes, as with the financial crisis of 2008, it’s terrifying.

Other times, such as in the middle of the dotcom boom of the 1990s, it’s downright exhilarating.

Both extremes lead to bad decisions and big losses.

Poker players like Duke call this “tilt.”

It’s the mental fog that arises after a particularly bad or good run of cards.

At such times, you’re prone to making irrational, and possibly catastrophic, decisions.

The first step to emerging from the fog is recognising the classic indicators of tilt.

Start by examining your physical state:

- Is your heart racing?

- Is your breathing rapid?

- Are you overwhelmed by the conviction that if you don’t act right now you’re passing up a chance you’ll never get again?

If so, it’s time to slow down.

Remind yourself of other times when you’ve felt the same way.

Ask yourself how the decisions you made on those occasions turned out.

Then take a break – better yet, a long walk – and talk yourself through the potential pros and cons of your situation.

Write down your reasoning.

In just about every case, the hard labour of putting your emotions down on paper will reveal that your situation is not quite as dramatic as you first thought.

Some simple precautions can ensure your behaviour under tilt doesn’t lead to permanent damage.

In the case of your stock and bond portfolio, an excellent idea is to write up an investment policy statement with the help of your financial adviser.

Ideally, you should do this during calm times, when you first set up your account.

The statement should set out the specific actions you and your adviser will take under a wide range of conditions, from a major market fall to an unexpected run of great returns.

Having a policy statement in place goes a long way toward ensuring you won’t get carried away by the emotion of the moment.

4. Know the numbers

In her early playing days, Duke heard a more seasoned player comment,

“It’s all just one long poker game.”

It was a reminder to take the long view of things, to keep both wins and losses in perspective.

Think of your investments the same way.

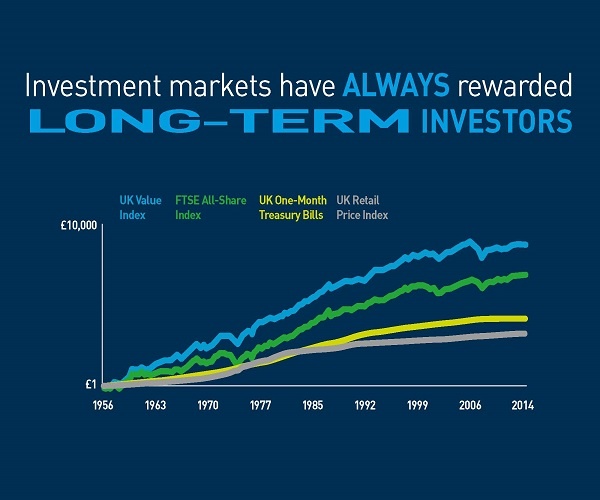

The most recent edition of the Credit Suisse Global Investment Returns Yearbook, compiled by professors at London Business School, shows that stocks have beaten other investments, hands down, over the course of many decades.

Since 1900, stocks have outpaced bonds by 3.2 percent a year and cash by 4.3 percent a year.

They’ve also trounced housing, which despite its recent hot streak has actually been a money-losing proposition on average, once maintenance costs are taken into account.

The authors of the yearbook calculate that the potential return from stocks has fallen in recent years but is still substantially better – by 3.5 percent a year, to be exact – than the potential payoff from holding cash.

For people who are willing to tolerate a bit of risk, the case for investing in a globally diversified portfolio of stocks and bonds remains overwhelming.

In fact, if you manage your risk, instead of letting it manage you, it’s one of the best bets going.