[Estimated time to read: 6 minutes]

To complete my age-specific investment guides, today I want to help you if you’re in your 60s and you’re wondering how best to grow and protect your money.

As Jennifer Johnson, our subscriber who suggested I write this series of guides mentioned:

“constantly one reads about time that is needed in the market! This is hugely scary and off putting to the thousands of expats within the 40 – 60 age range…”

Of course, the longer you have to invest the better, and the higher your returns are likely to be – but that does not mean if you’re planning on retiring any time soon you should forget about investing and keep all your funds in cash.

The best laid plans…

Ideally, in our 60s, we’ll have a healthy pension pot, no debt and be looking forward to stopping work and starting a new chapter in life.

But, as Robert Burns wrote (my translation):

“The best-laid plans of mice and men often go awry.”

Because I’m a pragmatic realist, today I’m going to start from the position that perhaps, your finances are not in perfect shape yet, and you want to get on track as quickly as possible to enjoy retirement soon…

First things first, how much have you got put by, and how’s it performing for you?

Could do better!

In my professional capacity, it’s no exaggeration to say that 9 out of 10 people I help can make significant improvements to their current savings, investments and pensions.

No matter how wealthy someone is, or how financially astute, most people end up paying far too much in fees without even being aware, and as a result, their money ends up underperforming significantly.

Even if you’re not able to do anything else right now, make the most of what you’ve already got.

Don’t allow greedy financial institutions to squander what you’ve already worked hard to put aside.

Request for an X-Ray Report TM, and we will technically analyse every account you have, and work out where you can make savings and improvements.

Why?

Because a part of our role as chartered fiduciaries is to adhere to the Chartered Insurance Institute’s Code of Ethics – a core philosophy of which is acting in the best interests of every client.

I.e., no matter who you are and how much money you have, it is in your best interests to understand if you are paying too much in fees or underperforming. We will help you do this, and give you all the information you need to maximise every penny you have put by.

Keeping everything in cash is a costly mistake

One of the most common objections to investing that I come up against is people’s fear of market volatility.

People fear mis-timing, a market correction, a crash or even a prolonged bear market.

Before I address these fears, allow me to explain why keeping all your money in cash is not a good idea.

Because of the rate of inflation versus the rates of interest available on cash savings, your nest egg's purchasing power will be declining every month as inflation outpaces your return, if you keep all your money in cash savings.

Investing is still appropriate

There’s a myth that keeps too many people from achieving financial freedom - investing is volatile, it’s scary – it’s an unwise thing to do, especially the closer one gets to retirement.

But being out of the market is riskier – fact!

I wrote this yesterday – but in case you didn’t read that blog, here it is again: -

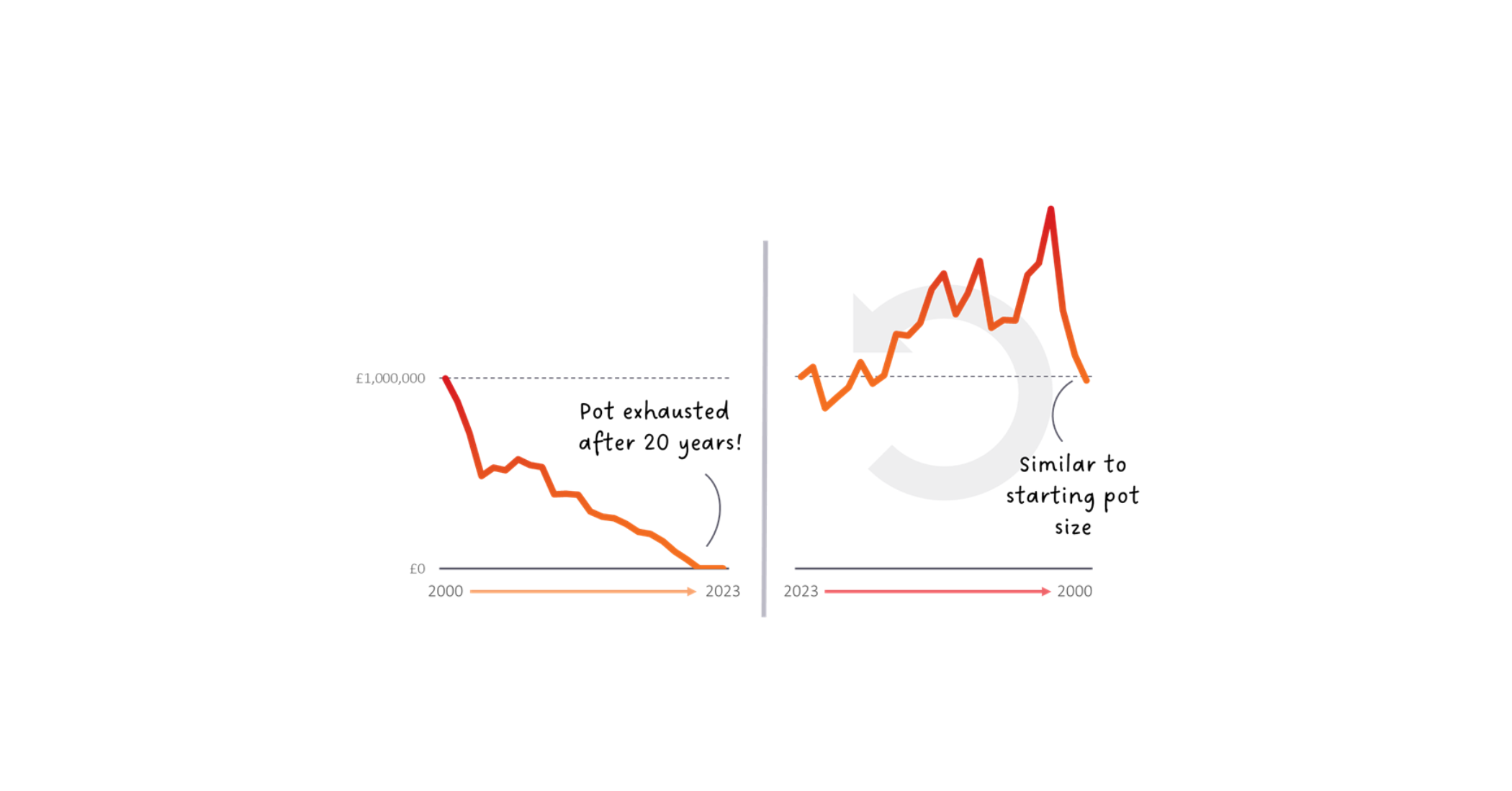

The Schwab Center for Financial Research studied the financial impact of market timing in a bid to find out if there was any basis for this universal fear.

They assumed hypothetical investors had $2,000 to invest once a year, every year for 20 years from 1993 onwards.

The perfect hypothetical investor timed their annual investment at the very lowest point of the market and returned $87,004 over 20 years on a $40,000 investment.

The worst hypothetical investor timed their annual investment at the very highest point of the market – and returned $72,487 over 20 years on a $40,000 investment.

The worst performer was the cash investor who, during a time when interest rates were much better than they are today, ended up with just $51,291 on a $40,000 investment because they saved instead of investing.

Accepting this fact, it’s important to know how to invest in your sixties, seventies and beyond.

It’s not what you do, it’s the way that you do it – that’s what gets results!

Whilst I can only generalise rather than give specific advice in this article, we usually recommend that our clients draw between 3 and 4% a year from their portfolio to pay for their retirement.

Through so doing, all the calculations say you are least likely to run out of money.

When structuring a portfolio for a client in their 60s and beyond, we also look to match a client’s risk level to their ability to take risk - and as such, the older one gets, it’s usual to take on less risk because there is less time, relatively speaking, to recover from any negative market movements or losses.

We therefore always allocate between cash, bonds and equities – and as a client gets older it is likely that we would increase allocation to bonds and reduce equities proportionately.

That is however a massive and basic generalisation – and my colleagues and I would be more than happy to talk with you, in detail, and go through our recommendations for you personally.

There is one key fact to keep in mind no matter what…

Stay passive!

Passive investing – i.e., tracking an index – is the lowest cost, highest potential returning approach to investing.

No matter whether you’re 18 or 80…be a passive investor if you want to be a successful investor.

You can rethink retirement

I appreciate that all the foregoing may be moot if you know you are not going to have ‘enough’ to retire on. I use the inverted commas because enough is a relative term…

If you cannot afford the retirement you’d anticipated, you can change your thinking about retirement.

Here are just a few ideas: -

- Work (and therefore save and invest) for longer;

- Go part-time if you don’t want to stay full-time, your income will supplement a smaller pension;

- Turn a hobby into a money-making venture to supplement your retirement income;

- Retire to a lower cost country;

- Or spend your home country’s cold winter months living cheaply abroad in a warm climate – you’ll save money and probably have a better life!

As expat financial teacher Andrew Hallam said in an interview with my boss Sam recently:

“If you can fog a mirror, if you’re living and breathing and thinking, it’s never too late.

I used to think I needed plenty of money to retire, but I’ve met people who retired (even at relatively young ages) with surprisingly little.

Because they have their minds and their ingenuity, they’ve found some really cool, creative options.”

In other words, don’t be defined and restricted by a traditional interpretation of retirement, you can rethink and remake retirement to suit yourself.

A helping hand whenever you need it

As mentioned above, together with my colleagues we’re happy to help in any way we can.

No matter what - I strongly recommend you have an X-Ray Report TM – because it will highlight any ways you can make more of what you’ve already saved, invested or placed in a pension.

It is not a subjective second opinion – it is facts laid bare in plain English.

Beyond that, we’re here to offer advice and solutions if you’d like some guidance.

Just because you’re in your 60s – or even your 90s – that doesn’t mean you should give up managing your money for the strongest possible financial returns.