[Estimated time to read: 4 minutes]

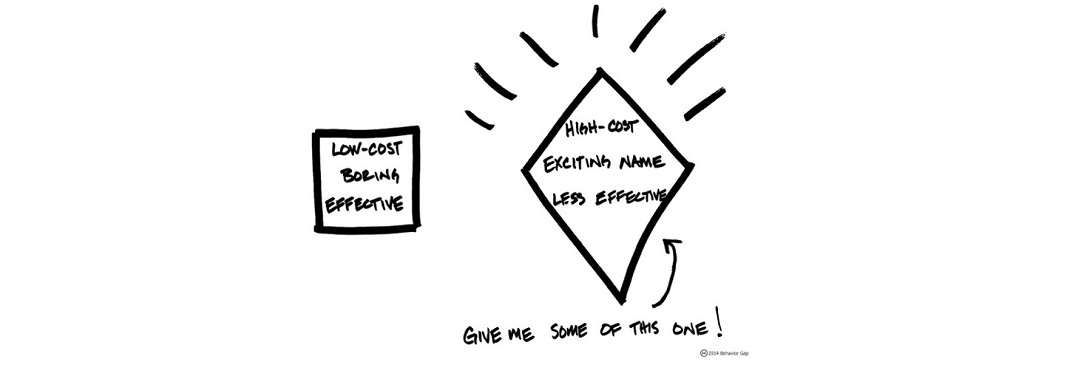

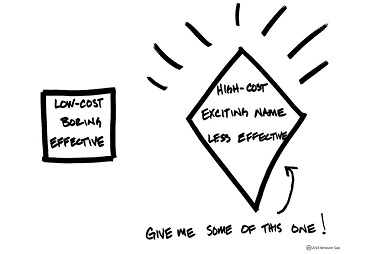

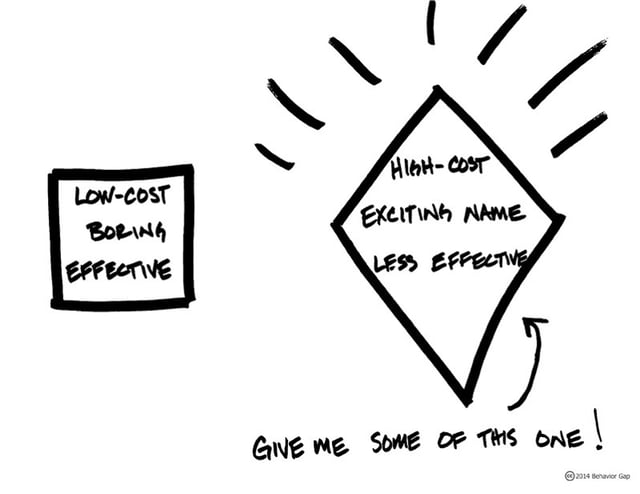

"Straightforward, lacking in imagination"

This is the investment style championed by the Nobel Prize winning Economist, William Sharpe.

Contrary to our natural desires, brain-numbing boredom is the ONLY truly enlightened state when it comes to investing.

Chasing boredom does require a little discipline.

As human beings, our ‘emotion’ often leads us to do exactly the opposite.

Nobody can deny that certain ‘rush’ experienced when betting our hard-earned cash on the markets.

But this is speculation and not sensible investment…

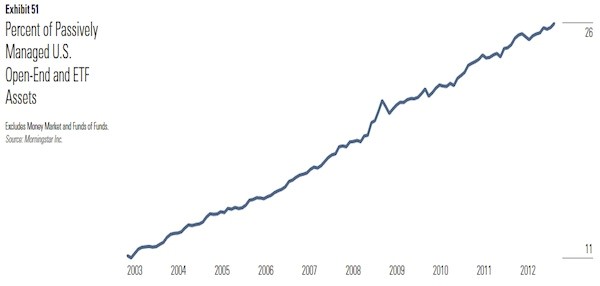

Sharpe, and indeed ‘average Joes’ worldwide with over $5 trillion invested, refer to ‘passive investing’ when they explain their dull desire for the doldrums.

Before we look at what’s “Kind of weird, but VERY profitable” – we need to understand 3 simple things.

First, why chase boredom?

Knowing the outcome of an investment really does kill the thrill. Nevertheless, it is 100% the best scenario for investors.

Second, what is ‘passive or evidence-based’ investing?

It’s investing to track the markets, rather than to beat the markets.

Passive investing aims to gain exposure to a portfolio of securities representative of an index or market. It’s humble aim to see your portfolio rise and fall with the overall trend.

Passive investing contrasts with active investing – in which a professional investor tries their luck picking stocks and guessing which asset classes might be under or over-valued.

‘Guessing’ the future in other words.

Third, what’s the logic of passive investing?

Take a look at the S&P 500 (representative of the American stock market) over the past 30 years: The passive part of the market returned roughly 10.0%.

Since Passive investing tracks the markets, we can determine the total market also returned 10.0%.

Logically, the active part had to return the same.

Here’s where active management hits soft sand.

Actively managed funds are subject to some unavoidable costs. First of all, the fund manager or managers must take a cut.

After all, no service is free.

The managers must regularly buy and sell securities within the funds. This costs money.

Then the brokers must take a cut.

In addition, selling the stocks on a regular basis, the investors are realising capital gains and exposing themselves to taxation.

Passive funds, on the other hand, pay a manager not very much… to do very little. They cost between 0.07% and 0.5% to do what a chimp might passably carry out if it could be trusted not to chew the mouse / keyboard.

Note: The author acknowledges that chimps may have evolved since computers looked like this

Unlike active funds, passive managers do very little buying and selling.

The brokers don’t, therefore, take the same cut.

Taxes do not normally apply where the capital gains are not realised.

Here’s the killer quote from Sharpe’s seminal work…

“If "active" and "passive" management styles are defined in sensible ways, it must be the case that:

(1) before costs, the return on the average actively managed dollar will equal the return on the average passively managed dollar and

(2) after costs, the return on the average actively managed dollar will be less than the return on the average passively managed dollar

These assertions will hold for any time period. Moreover, they depend only on the laws of addition, subtraction, multiplication and division. Nothing else is required.”

(Source: Sharpe at the Spring President's Forum, Monterey Institute of International Studies, 2002)

What’s kind of weird, but VERY profitable?

Enter Discretionary Fund Managers!

Discretionary Fund Managers (DFMs) manage clients’ portfolios. They are actively managed in a discretionary manner.

Many manage client’s portfolios in a similar way to fund managers actively managing funds.

So…

“Should I pay somebody to actively manage my portfolio?”

In the prehistoric world of the DFMs, at least partial extinction is near – albeit unlikely to be meteor-induced.

The methods of some DFMs are at best outdated and at worst positively primordial – failing to stack up against the modern era of passive investing and Exchange Traded Funds (ETFs).

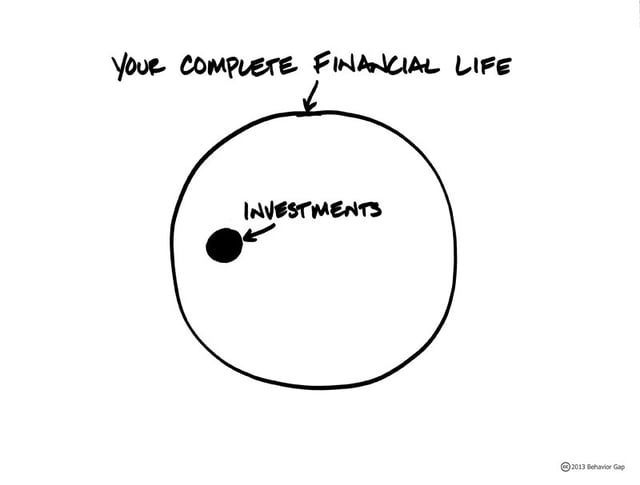

Kind of weird that the ‘dead weight’ group of DFMs form such a lucrative part of the value chain, enlisting IFA salespeople to supply clients and act as intermediaries. Particularly when investment is such a small part of your overall equation:

They also often skirt around any responsibility to explain their decisions and total costs in simple, non-opaque terms.

All they really have to do is provide an easy to use portal for the advisers to print off fancy-looking valuations and, offshore, pay those advisers handsome commissions too.

With a total expense ratio of up to 3%, these DFMs can torpedo an individual’s investments; underperforming the markets and landing the individual investor with another layer of costs.

VERY profitable… for those DFMs.

There are other passive based DFMs which add significant value and perform the task of managing complex portfolios efficiently. The investor benefits from economies of scale on trades and management tasks as well as necessary technical expertise such as hedging and re-balancing.

So what do we recommend?

Discretionary Fund Managers, can cost more than they are worth and some are truly relics of the ‘Lost World’ of modern investing.

Check out our independent reviews to gain an insight into which DFMs might be worth investigating further.

If your investments are held with any of the DFMs reviewed, we recommend you get a X-ray Review.