Gold is often viewed as a safe haven that will protect you from inflation, market crashes, anarchy and even the total failure of a major currency.

But in my view, it has no place in your portfolio.

Gold is often said to have an inverse relationship with stocks and a direct relationship with inflation, giving it the allure of being a valuable diversification asset to include in investment portfolios.

But don't be fooled by shiny things.

Any investment can be placed in one of four main categories:

- Cash flow producing assets

- Commodities

- Currencies

- Collectibles

Which category does gold fall into?

Gold has some limited use in industrial production, meaning that it could be viewed as a commodity.

It may also form part of many of your collectibles.

But neither of these drive the demand for gold.

In most cases, gold is used as a store of value. In other words, people buy gold, hoping to sell it for more later.

It's certainly not a cashflow producing asset.

Warren Buffett explained why this is so important in a 2012 article, using a brilliant analogy.

At that time, the world's gold stock was worth about 9.6 trillion US Dollars. For that amount of money,

"You could buy all of the crop land in the US - 400 million acres with roughly $200 billion of annual output - and 16 ExxonMobils - each one earning $40 billion annually. Still after buying those assets, you would have 1 trillion U.S. dollars in cash leftover."

Buffett explains that a century from now, the 400 million acres of crop land will have produced a massive amount of output regardless of the currency regime at the time.

Exxon will have produced trillions of Dollars in profits for shareholders, while also growing its assets to be worth many more trillions.

The gold will have remained unchanged in size and will still be unable to produce anything.

As Buffett says,

"You can fondle the gold, but it will not respond."

Buffet's argument makes logical sense, but does it hold up under scrutiny?

An inflation hedge?

Claude Erb and Campbell Harvey conducted a thorough analysis of gold in their 2012 paper, titled The Golden Dilemma.

First, they looked at gold as an inflation hedge.

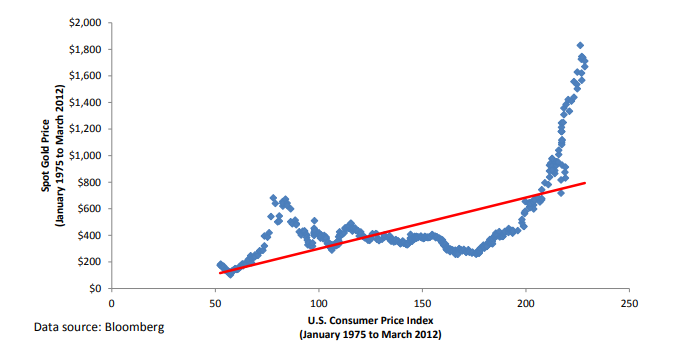

Taking gold returns going back to 1975, just after the U.S. had just come off the gold standard and when US citizens were once again able to own and trade gold, right up to March, 2012, they found that gold has not been a good inflation hedge over the short or long-term due to the volatility of its real price.

The red line shows that on average the higher the level of the Consumer Price Index (CPI), the higher the price of gold. This line roughly portrays the implied price of gold - if gold was driven by CPI. However, as you can see, the price of gold swings widely around the CPI.

The inflation derived price of gold and the actual price of gold have rarely been equal.

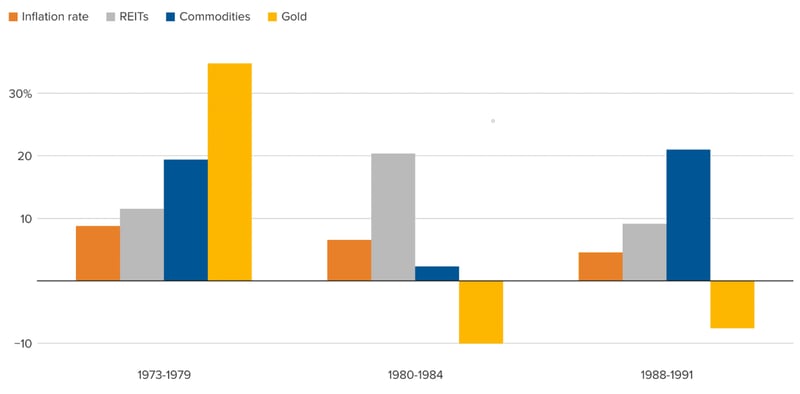

Investors worried about rising consumer prices may want to consider other asset classes. But again, gold is really not a perfect hedge, when looking at the returns of various asset classes during periods of above-average inflation.

In short, there’s no guarantee if there’s a spike in inflation, gold will also generate above-average returns. The below chart shows total returns for commodities, Real Estate Investment Trusts (REITs) and gold during inflationary periods. Gold has a mixed track record during past periods of high inflation (source: morningstar).

(If you happen to have a debt that's due in 2,000 years, then gold might just be the perfect way to keep your purchasing power intact. Erb and Harvey did find that, going all the way back to Emperor Augustus who ruled from 27 BC to 14 AD, gold has proven to be quite the inflation hedge when measured against military pay.)

Campbell and Harvey said,

"In normal times, gold does not seem to be a good hedge of realised or unexpected short-run inflation. Gold may very well be a long run inflation hedge. However, the long run may be longer than an investor's investment time horizon or lifespan."

As a final example of gold’s value as an inflation hedge...

On January 21, 1980, the price of gold reached a then-record high of $850. On March 19, 2002, gold was trading at $293, well below its price 20 years earlier. The inflation rate for the period from 1980 through 2001 was 3.9%. Thus, gold’s loss in real purchasing power was about 85%.

How is gold an inflation hedge when it lost 85% in real terms over 22 years?

But inflation hedging is only one reason people buy gold. A more common reason is because it's supposed to be a safe haven.

An asset that will perform well, when everything else isn't.

Is gold a safe haven?

Erb and Harvey found that 83% of the time that stock returns were negative, gold returns were positive. That's not a bad record.

If you look at the data for the gold spot price and the MSCI All Country World Index, from 1988 to 2019, they had a correlation of 0.085, which is very low, but not negative (we might expect a safe haven to have a negative correlation with stocks).

However, as gold prices declined over 30% during the worst of the financial crisis—when the hedge was needed most, it failed.

In 2022 when stocks and bonds produced double-digit losses, even though gold outperformed stocks and bonds, it failed to provide a true hedge, as it fell slightly, closing at $1,824 in 2022 after closing at $1,829 in 2021.

In 2008, when the global market dropped over 40% in US Dollar terms, gold increased 5.53%, which sounds good...

But US government bonds increased nearly 14%.

A bumpy ride

It's not obvious that gold is always going to be there to save the day when stocks crash.

Having said that, any asset with a low correlation to stocks is worth consideration in a portfolio.

With gold however, there remains a problem that can't be ignored...

Even though it has a low correlation to stocks, it also has questionable expected returns.

As Buffett explained,

"This is not an asset with any output. Gold will always be gold and it will be worth whatever someone is willing to pay for it. We may hope that it will maintain its real value, meaning an inflation adjusted expected return of zero, but historically it has had a very volatile real value."

Looking back at 1988 to 2019, the standard deviation of gold spot price has been 15.43% compared to 14.85% for the MSCI All Country World Index.

Over that same period, gold returned 3.43% annualised before inflation, while global stocks returned 7.85%.

In short, gold has been more volatile than stocks while delivering low returns.

So, despite its low correlation to stocks, gold's lack of expected returns makes it a challenging addition to any portfolio.

If we take the period from 1988 to 2019, a portfolio of 90% global stocks and 10% gold had a slightly lower annualised return than a 100% equity portfolio, but it did have slightly higher risk adjusted returns.

It would be easy now to say that gold is useful in portfolio construction.

But every Dollar or Pound allocated to gold is money that could have been allocated to something else.

A portfolio with a 10% allocation to one to five year global government bonds hedged to US Dollars instead of gold, had higher returns and higher risk adjusted returns than the 10% gold portfolio over the same time period.

Here, allocating to gold did offer a volatility reduction benefit, but there was also an 'opportunity cost' to allocating to gold instead of government bonds.

I would expect this to remain true for expected returns over different time periods.

What's the opportunity cost of putting a portion of your portfolio in gold?

Gold has no real expected return

Gold may have historically done well when stocks have done poorly, but there were other diversifying assets with better expected return profiles that accomplish the same.

Erb and Harvey also highlight an important point - being considered a safe haven on paper doesn't necessarily mean that it will safeguard the actual wealth of the owner in a true catastrophe.

Simply put, it's difficult to carry gold with you during such events, and a gold ETF wouldn't be of much help either.

Individuals who strongly advocate for investing in gold as part of a portfolio are likely not considering it as a long-term investment. Instead, they view it as a long-term insurance policy against catastrophic events such as hyperinfation.

According to Erb and Harvey's findings, the real value of gold, in terms of its purchasing power, remains relatively stable across the globe at any given time.

Let's take Brazil from 1990 to 2000, as an example. The average inflation rate during this time was 250%. The real price of gold in Brazilian terms fell by about 70%. While gold may not have been a highly successful inflation hedge in Brazil during this period, it still fared better than holding Brazilian cash, which lost almost 100% of its value.

Does that make it a good hedge?

Not really.

The actual returns of gold are not influenced by the inflation environment in a particular country. Gold remains indifferent to this and may experience significant negative real returns during a period of hyperinflation.

It can't be assumed that gold will maintain its purchasing power or generate positive real returns, simply because there was a bout of hyperinflation in the country you live in.

Gold is not a productive asset

It has a real expected return of zero.

It might keep pace with inflation over the very long-term, but that's probably longer than most people can wait.

Even as a safe haven, due to its low correlation with financial assets, gold falls short in a portfolio due to its non-existent real expected return.

Finally, while gold's purchasing power is unaffected by inflation, that doesn't mean that gold will maintain its purchasing power during periods of inflation, calling into question its ability to hedge against extreme currency events.

A final note on trading gold.

Some people will tell you it's possible to profit from actively trading gold as opposed to holding it. This may be true, just as it's true for other non-productive assets, like Bitcoin. But our business is not in trading strategies.

There are likely hundreds of YouTube channels dedicated to teaching you trading strategies for gold, and I bet that none of them cite the academic literature that I've included here.

Take from that what you will.