[Estimated time to read: 2 minutes]

[Estimated time to read: 2 minutes]

When Timothy Gallwey published “The Inner Game Of Tennis” in 1974, he focused on the game within a player’s head.

He listed their fears, doubts and limiting self-beliefs as just a few of the tennis player's formidable opponents.

When these obstacles are removed (or at least better managed), our mind is quiet and focused, and we can focus wholly on the task at hand.

We are “in the zone.”

Every sphere of life has its inner game. Sport, work, relationships, family – each area is intimately influenced by our mental attitude.

Problems occur because you haven’t mastered your inner game.

Your outer game will inevitably suffer as a consequence.

You might wonder what makes investment so complicated. How can international investment possibly have an “inner game”?

This fascinating area has evolved into its own field — behavioural finance — reflecting that investment markets provide unusually robust data sets for analysing “judgment under uncertainty”.

Every day, international investment markets provide researchers with billions of data points for understanding how people make choices when resources are at stake and the outcome is unknown.

What differentiates the typical investor is their justification for engaging in their activity.

Ask a random amateur tennis player whether he or she could compete with Roger Federer, and the most common response will be laughter.

Yet many of those amateur investors will willingly compete with the billionaire investor Warren E. Buffett.

Despite the spectacular growth of index funds — passive investment vehicles that track market averages and minimize transaction costs — millions of amateur investors continue to actively buy and sell securities regularly.

This is despite overwhelming evidence that even professional investors are no more likely to beat the market than chimps throwing darts at fund listings.

Money managers, at least, are paid to make investment bets.

But why do amateurs believe they can outperform the professionals — or even identify those pros who will outperform? (Performance of individual mutual funds cannot be predicted with any greater degree of accuracy than individual stocks or bonds.)

Many biases and cognitive errors contribute to this costly behaviour, but a few deserve mention:

- Herd mentality

- Recency

- Confirmation bias

- Overconfidence

- Loss aversion

Each of these behaviours can cause havoc with investor returns. To get more information and detail on each of these, please watch this YouTube Video.

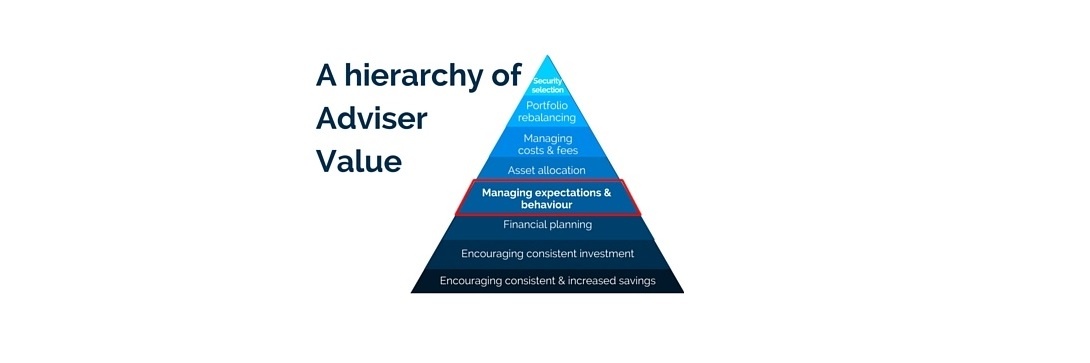

The management of the in-built human behaviour is a critical factor in getting top performance and is something a professional financial adviser will be able to help with.