News

Financial Life Management

Financial Education

The 2020s are teaching investors more than any textbook ever could

Reflecting on the lessons learned by patient investors through nine market shocks in six years, and why that education matters more than any textbook.

Read more

Whitepaper

Financial Life Management

Are you ready to retire?

Discover 9 essentials you need to know before work becomes optional.

Read more

News

Financial Life Management

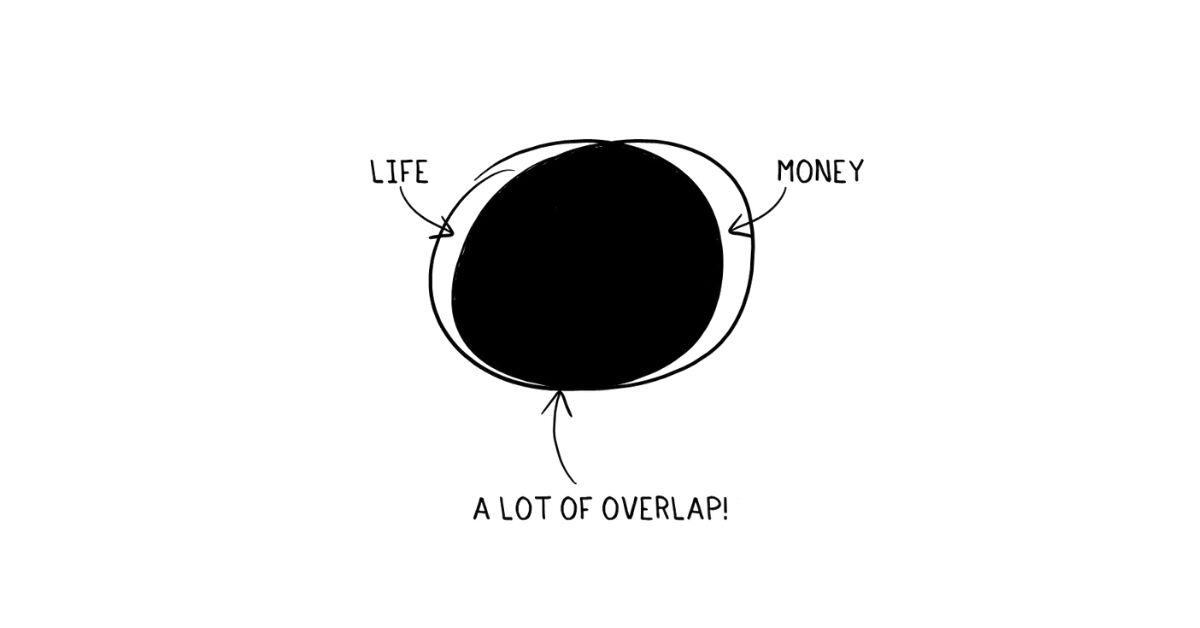

Why smart people interfere with good financial plans that are working

When money is tight, the investment contribution feels like the most flexible line in the budget.

Read more

News

Financial Life Management

The most expensive words in finance you don't notice

The subtle financial phrases that quietly cost investors the most over time.

Read more

Article

Financial Life Management

Business exit planning for internationally mobile founders

Essential insights into business exit planning for internationally mobile founders, focusing on preparation, tax strategy, and family dynamics for a successful transition.

Read more

Whitepaper

Employee Benefits

Group health insurance in the Middle East: what CEOs need to know

Are you a CEO or otherwise lead a company of 20 or more people?

Read more

News

Financial Life Management

Why playing it safe with your savings is riskier than you think

The ideal savings rate is something your family can sustain month after month.

Read more

Whitepaper

Financial Life Management

Pursuing a better investment experience

10 key principles to improve your odds of investment success.

Read more

News

Financial Life Management

How much to save? It's more than you think

Why most people significantly underestimate how much they need to save for financial security.

Read more

Article

Employee Benefits

HR guide: Supporting your employees during times of regional conflict

A practical resource for UAE HR professionals covering mental health support, and how to get more from your group medical insurance.

Read more

Article

Financial Life Management

Returning to the UK in 2026: Your complete financial guide

Guide to returning to the UK in 2026: Navigate tax, financial planning, and residency challenges for a smooth transition back home.

Read more

Article

Financial Life Management

How to invest in times of war

Discover how to safeguard your wealth during times of war and geopolitical turbulence.

Read more

Whitepaper

Employee Benefits

5 red flags your group medical insurance isn't working

Is your group medical insurance working for you or against you?

Read more

News

Financial Life Management

Why chasing gold and silver gains misses the point

The risks of pursuing commodity momentum instead of focusing on long-term investment strategy.

Read more

Article

Financial Life Management

International trusts, foundations and modern estate planning: what actually matters now

Explore the evolving landscape of estate planning, where trusts and foundations play pivotal roles in wealth preservation and succession for modern families.

Read more

News

Financial Life Management

Should we worry about market concentration?

Whether increasingly concentrated equity markets pose a meaningful risk to investors.

Read more

Whitepaper

Financial Life Management

Your wealth security checklist

A practical guide to protecting your family, wealth, and your future in uncertain times.

Read more

Article

Financial Life Management

13 reasons you may need a financial life manager in 2026

When life changes, money changes. And when money changes, life changes. These transitions in life are inevitable and something we will all go through.

Read more

News

Financial Life Management

Beneath the surface: the quiet work of a real financial life manager

What genuine financial life management looks like beyond product sales and portfolio reviews.

Read more

Article

Employee Benefits

Global benefits director? Discover the value of local support in managing UAE employee benefits

Discover the importance of local expertise in managing UAE employee benefits, ensuring compliance, cost-effectiveness, and timely support for global benefits directors.

Read more

Article

Financial Life Management

Employee Benefits

Understanding financial regulation in the UAE: what expats should know about AES

Is AES regulated in the UAE? Explore the regulatory landscape for financial services in the UAE and understand how AES ensures compliance and consumer protection for expatriates.

Read more

Whitepaper

Financial Life Management

Private banking vs. financial life management

The differences when it comes to long-term investing.

Read more

News

Financial Life Management

Why spending on experiences feels more meaningful than material purchases

The behavioural economics behind why experiences tend to deliver more lasting satisfaction than things.

Read more

News

Financial Life Management

Why AES International is attracting the next generation of financial advisers

How AES's culture and fiduciary model appeals to a new generation of financial planners.

Read more

Article

Financial Life Management

Transferring a UK pension overseas: what's actually changed, and the questions worth asking before you sign anything

The lifetime allowance is gone and pensions face UK IHT from 2027. Here's what actually applies before transferring a UK pension abroad.

Read more

News

Financial Life Management

Five year-end financial moves every wealthy family should make

Practical end-of-year planning steps for high-net-worth families to protect and grow their wealth.

Read more

Article

Financial Life Management

Autumn Budget 2025: What Rachel Reeves’s plans could mean for global HNWIs

Discover how Rachel Reeves's 2025 Autumn Budget could impact global high-net-worth individuals and why waiting for facts, not rumours, is crucial for financial planning.

Read more

News

Financial Life Management

Why being a fiduciary firm transforms everything: Lessons from AES International's journey

How committing to the fiduciary standard reshapes client relationships and the entire business model.

Read more

News

Financial Life Management

UK Budget 2025: Essential Guide for British Expatriates and Non-Residents

A practical breakdown of Budget 2025 and what it means for British expats and non-residents.

Read more

News

Employee Benefits

10 Questions That Could Save Your Company Money on Medical Insurance in 2026

The key questions HR leaders should ask before renewing group medical cover to avoid overpaying.

Read more

Article

Employee Benefits

10 questions that could save your company money on medical insurance in 2026

Transform your insurance negotiations by asking these 10 crucial questions to optimise benefits, reduce costs, and enhance employee satisfaction.

Read more

News

Financial Life Management

Why traditional retirement planning is outdated

Why conventional retirement frameworks no longer fit the reality of modern expat lives.

Read more

Article

Financial Life Management

7 essential financial truths for wealthy professionals in Dubai with $1M+ who want to retire - and stay retired

Discover seven essential financial truths that help wealthy professionals in Dubai retire successfully and maintain their financial independence throughout retirement.

Read more

News

Financial Life Management

It's never too late to put your finances in shape

Why financial recovery and rebuilding is possible at any age or life stage.

Read more

News

Financial Life Management

No need for Fomo: You're not missing out. You're investing smarter.

Why disciplined, long-term investors should ignore the fear of missing out on market trends.

Read more

Article

Financial Life Management

Why spending more in retirement might be the smartest decision you ever make

Discover why spending more in retirement might be a smarter financial move, and learn strategies to ensure your wealth lasts while enjoying the lifestyle you desire.

Read more

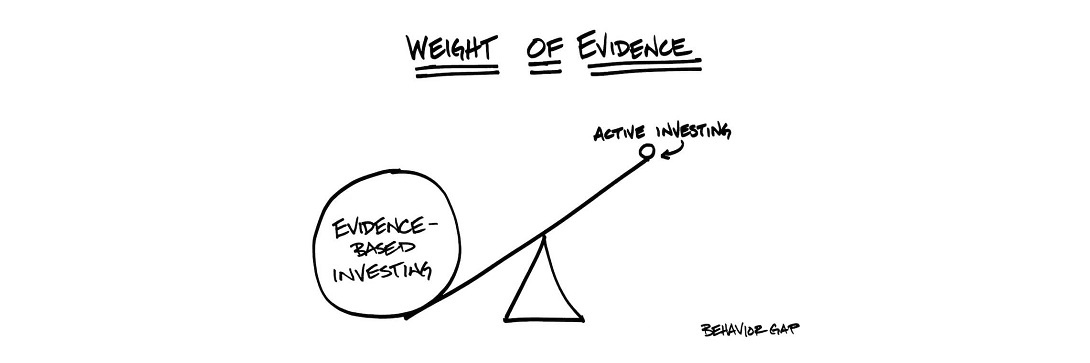

Article

Financial Life Management

Why boring investing still wins in Dubai, and what an investment philosophy actually is

Most investors chase the next hot pick. Here's why a disciplined, evidence-based philosophy beats it, with the data behind it.

Read more

News

Financial Life Management

Why it's important to align your money choices with your values

How values-based financial planning helps people make money decisions with greater clarity and purpose.

Read more

News

Financial Life Management

Why temperament matters more than tactics in investing

How emotional discipline consistently outperforms clever strategy for long-term investors.

Read more

Article

Financial Life Management

If my clients ever worry they’re missing out on big gains - here’s what I tell them about building real wealth

Learn why staying invested in a diversified portfolio is the key to real wealth, even when it feels less exciting than chasing market hype.

Read more

Article

Financial Life Management

5 big retirement regrets (and what you can do now to avoid them)

Discover the top five retirement regrets and learn actionable steps to avoid them, ensuring a fulfilling and regret-free retirement.

Read more

Article

Financial Life Management

How to know if you can retire early (10 clear signs you're closer than you think)

Discover the signs that indicate you might be ready for retirement sooner than you think, without sacrificing your lifestyle or financial peace of mind.

Read more

Article

Employee Benefits

Top benefits of group health insurance for employees in UAE

Discover the strategic benefits of group health insurance for employees in the UAE, including improved retention, better access to care, and cost efficiency for your business.

Read more

Article

Financial Life Management

How the wealthiest 1% actually save for retirement

Discover how the wealthiest 1% save for retirement with simple, effective strategies to build sustainable wealth and secure financial well-being.

Read more

News

Financial Life Management

Knowing the future may not make you a better investor

Why predictive thinking and market forecasting can actually undermine investment returns.

Read more

Article

Financial Life Management

Earning 6 or 7 figures? That doesn’t mean you’re ready for retirement

How high earners can secure a financially stable retirement, even amidst inflation and tax uncertainties.

Read more

Article

Financial Life Management

The buy-to-let myth: Property investment vs. pension returns

People have been obsessed with property for years. Is buy-to-let property really a substitute for a well-invested pension pot?

Read more

Article

Financial Life Management

Still UK domiciled at heart? Why that no longer decides your inheritance tax bill in Dubai

UK inheritance tax no longer depends on domicile. Here's what the new residence-based rules mean for British expats living in Dubai.

Read more

Article

Financial Life Management

Will your children and grandchildren squander the wealth you build?

Discover how financial education and smart planning can ensure your children and grandchildren sustain and grow your hard-earned wealth.

Read more

Article

Employee Benefits

Health Reimbursement Arrangement (HRA): Your complete guide

Discover how Health Reimbursement Arrangements (HRAs) in the UAE can offer flexible, cost-effective healthcare benefits for your employees.

Read more

Article

Financial Life Management

10 investments you THINK are safe (but actually aren't)

Discover the hidden risks in investments you think are safe. Learn how experienced investors redefine risk and protect your wealth from erosion.

Read more

Article

Financial Life Management

Anyone retiring within the next 5 years: here are 3 ways to boost your wealth

Discover how the final five years before retirement can significantly boost your finances through smart planning and strategic investments.

Read more

News

Financial Life Management

Consistency and patience key to becoming a successful investor

Why steady habits and a long time horizon beat market timing for building lasting wealth.

Read more

Article

Financial Life Management

Trading vs investing: what’s the difference?

Understand the crucial differences between trading and investing to make informed financial decisions and build sustainable wealth over time.

Read more

Article

Financial Life Management

Is this the best, low-cost retirement country for active people?

Discover a retirement destination for active individuals seeking a sun-drenched, outdoor lifestyle with favourable taxes and great cycling opportunities.

Read more

Article

Financial Life Management

The real reason the stock market crashed (and what smart investors are doing)

Discover why the latest stock market crash isn't causing smart investors to panic and learn how to navigate market volatility with confidence.

Read more

Article

Employee Benefits

How to choose the best business health insurance in UAE

Guide to choosing the best business health insurance in the UAE, focusing on cost management, employee well-being, and strategic planning for sustainable growth.

Read more

News

Financial Life Management

How understanding empathy can lead to better financial decisions

The role emotional intelligence plays in making wiser, more considered financial choices.

Read more

Article

Financial Life Management

9 essential money rules for the wealthy - laws of money (plus one bonus you can’t ignore)

( Laws of money ) Learn 9 essential Money rules (plus a bonus) for effectively managing and growing wealth, from investment strategies to budgeting principles.

Read more

Article

Financial Life Management

Stop worrying about the future - there's a smarter way to build wealth

Perfect foresight won't guarantee financial success. A solid, adaptable financial plan is key to navigating market uncertainties and achieving goals.

Read more

Article

Financial Life Management

What can you learn about money, delusions and happiness from Donald Trump?

Learn about the impact of recency bias, economic misconceptions, and the true sources of happiness through an analysis of Donald Trump's rhetoric and historical economic data.

Read more

Article

Employee Benefits

How health insurance companies in Dubai deal with pre-existing conditions

Learn how health insurance companies in Dubai manage pre-existing conditions and what it means for your coverage or business plans.

Read more

Article

Financial Life Management

Investment biases: these psychological traps are costing you money

Learn how psychological traps can affect your decisions and how to make more rational investment choices.

Read more

News

Financial Life Management

Tracking performance is a stepping stone toward more meaningful results

Why measuring progress in investing is a foundation for achieving better long-term outcomes.

Read more

Article

Financial Life Management

Should you buy gold? Here's what Warren Buffett would say

Should you invest in gold? Discover Warren Buffett's perspective on gold's long-term returns compared to stocks and why it might not be the best store of wealth.

Read more

Article

Financial Life Management

After two decades in financial life management, I’ve realised almost everyone gets the same thing wrong

How much do you really know about investing and financial planning? And, is it enough to for you to manage your finances alone? Read this.

Read more

Article

Financial Life Management

Retirement withdrawals: why timing matters more than you think

Learn why timing your retirement withdrawals is crucial and how to manage sequence risk, ensuring your financial stability through market ups and downs.

Read more

Article

Employee Benefits

7 mistakes to avoid when buying corporate health insurance plans in Dubai

Avoid costly corporate health insurance mistakes in Dubai. Learn the common pitfalls and how to choose the best plan for your business and employees.

Read more

Article

Financial Life Management

Trump’s return: What his re-election means for investors

Explore the potential impacts of Donald Trump's second term on financial markets, with insights into his promises, team, and governing style.

Read more

News

Financial Life Management

Why do we feel guilty about money?

The psychology of financial guilt and how it quietly shapes spending, saving, and giving behaviour.

Read more

Article

Financial Life Management

Cognitive bias cheat sheet: A simple guide to thinking smarter

Learn how cognitive biases shape your decisions and discover strategies to think smarter, avoid costly mistakes, and enhance decision-making skills.

Read more

Article

Financial Life Management

Investing in 2025: how to stay calm and confident in uncertain times

Stay calm and confident in 2025: Discover strategies to navigate turbulent times effectively.

Read more

Article

Financial Life Management

This is the price disciplined investors pay for the best long-term returns

Learn how disciplined investing and embracing volatility can lead to long-term financial success despite short-term market fluctuations and corrections.

Read more

Article

Financial Life Management

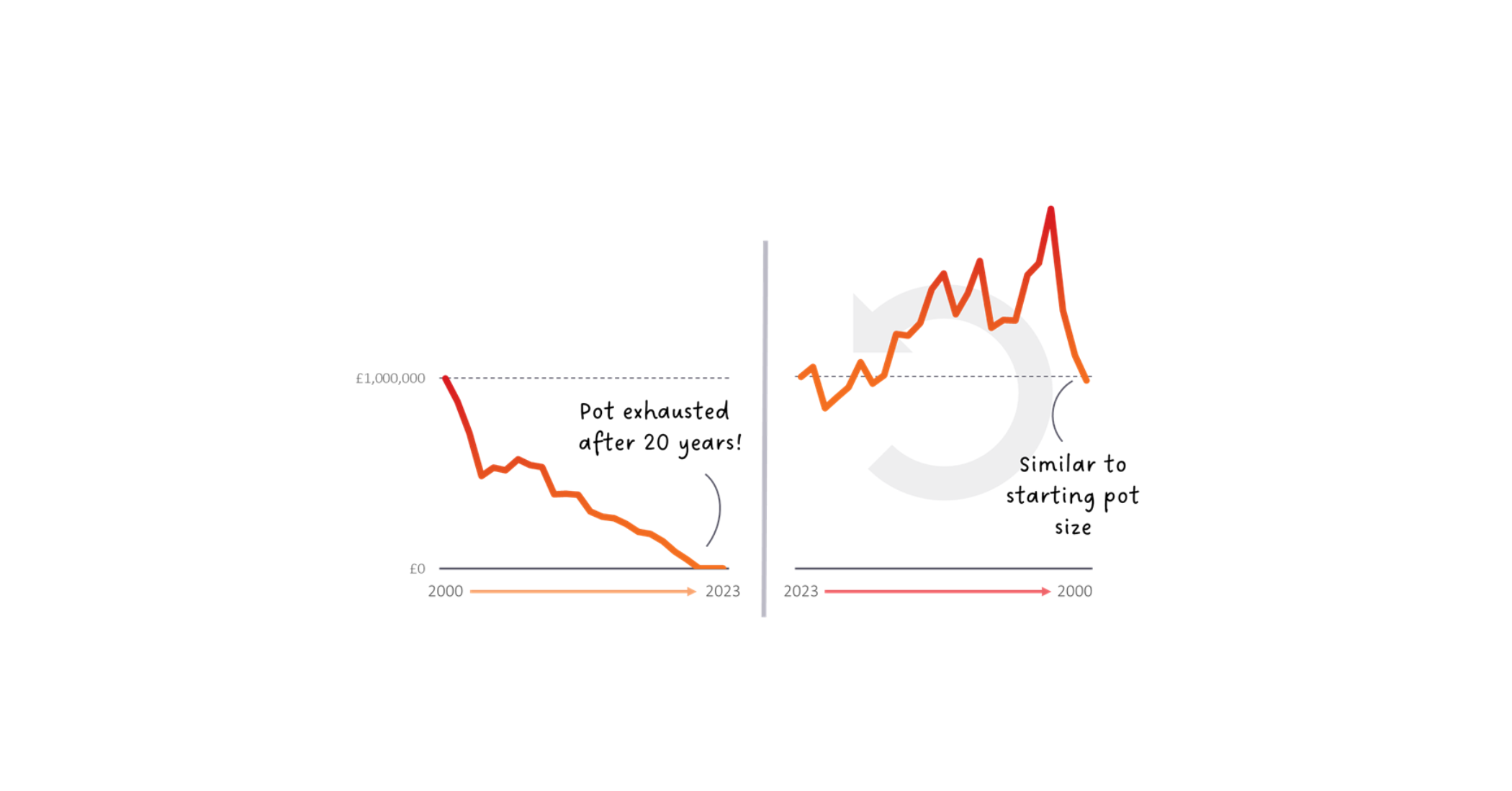

How retirees could go broke with the 4% rule

Discover the surprising truth about gold as an investment - is it as stable and lucrative as you think?

Read more

Article

Employee Benefits

How HR managers can choose the right group health insurance in the UAE

Discover how to choose the right group health insurance in the UAE, focusing on employee well-being, cost management, and strategic wellness programmes for long-term benefits.

Read more

News

Financial Life Management

What are you gaining or giving up in pursuit of financial success?

The real trade-offs people make when chasing wealth — and whether the sacrifices are worth it.

Read more

Article

Financial Life Management

I just received a lump sum, should I invest it all now, or gradually?

Deciding between lump sum and gradual investing? Learn which is the better choice, backed by historical evidence and market trends.

Read more

Article

Financial Life Management

Could you be making this $1 million mistake without realising it?

Compare your investment returns and learn why balanced portfolios often outperform all-stock portfolios.

Read more

Article

Financial Life Management

The uncomfortable truth about building wealth for your future

Discover the powerful, often overlooked secret to wealth building that can lead to genuine financial freedom over time.

Read more

News

Financial Life Management

How to future-proof your finances while living in the moment

Balancing present-day spending with long-term financial security without sacrificing enjoyment.

Read more

Article

Financial Life Management

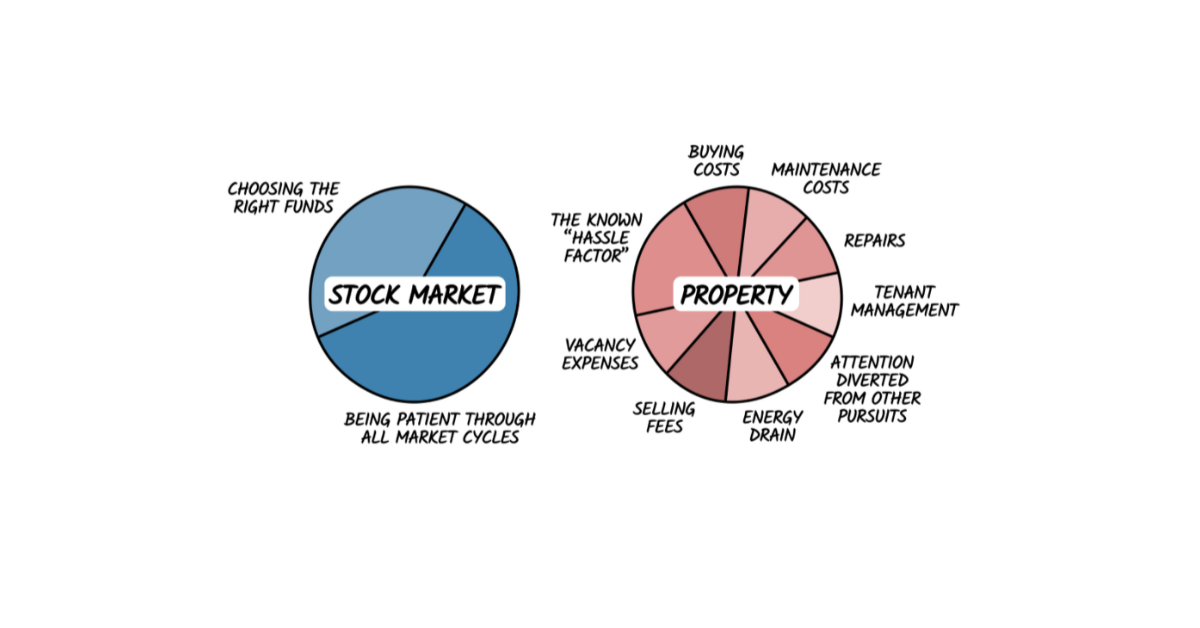

The hidden costs of ownership: property vs the stock market

Explore the hidden costs of property ownership versus stock market investments, highlighting the real expenses, effort, and opportunity costs involved in both.

Read more

Article

Financial Life Management

The sleep-well strategy: Why 'boring' investors always win in the end

Discover the hidden power of 'boring' investing. Learn why systematic, evidence-based strategies quietly build sustainable wealth and bring peace of mind.

Read more

Article

Financial Life Management

13 money truths I’m passing to my kids - that every parent should too

13 essential financial principles every parent should teach their children to build lasting wealth and financial resilience.

Read more

News

Financial Life Management

How to achieve the best returns with time, patience and discipline

The three core traits that separate successful long-term investors from the rest.

Read more

Article

Financial Life Management

After a decade of repeating myself - what's happened in the markets?

Stay calm, remain invested, and focus on the long-term. Learn how staying the course has proven beneficial over the past decade.

Read more

Article

Financial Life Management

Before you invest with a private bank, read this

Private banking in Dubai: Our independent reviews look at their suitability for international professionals and include our own expert verdict.

Read more

Article

Financial Life Management

Inside the minds of the wealthy: 6 ways they grow their wealth

Discover six strategies wealthy individuals use to grow and preserve their wealth for future generations.

Read more

Article

Financial Life Management

How my friend fell for an investment con, and the 6 red flags she missed

Learn how one woman was deceived by an investment con artist, the six red flags she missed, and how you can protect yourself from similar scams.

Read more

News

Financial Life Management

How the power of discipline shapes your financial well-being

Why financial discipline is the single most important foundation for building lasting wealth.

Read more

Article

Financial Life Management

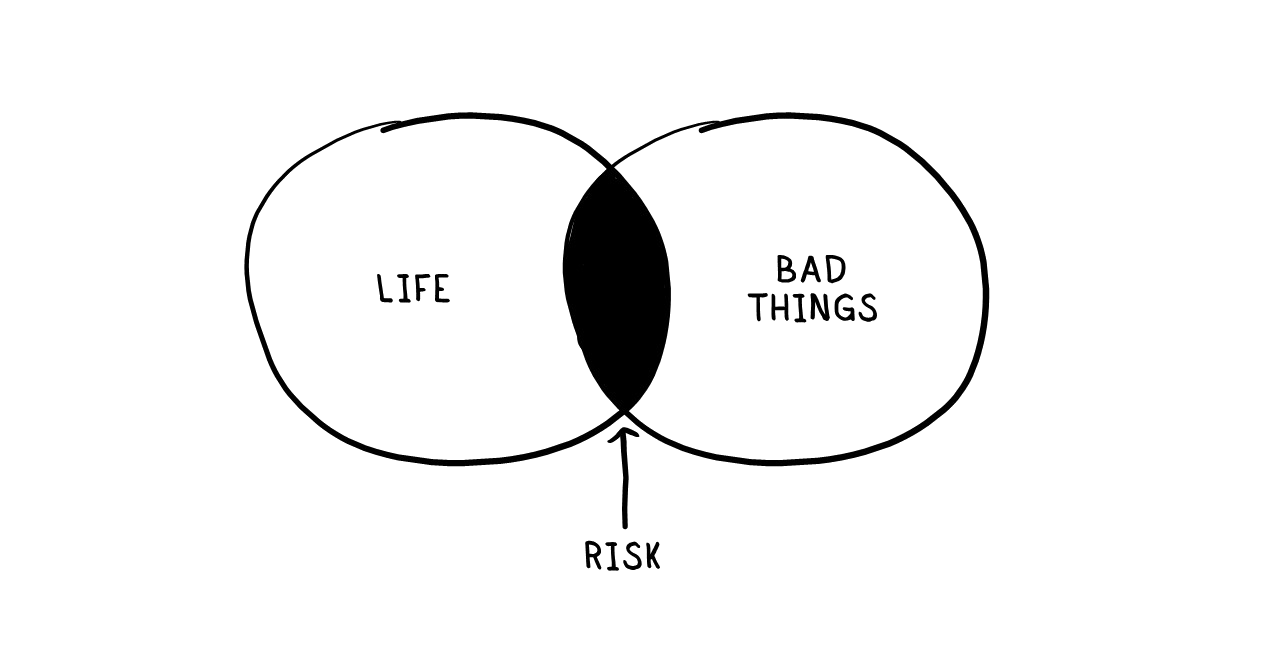

What risk really is, and why it's everywhere

Risk is inevitable in every aspect of life and investing; understanding and managing it is key to achieving potential rewards.

Read more

Article

Financial Life Management

10 reasons why investing is simple, but not easy

Investing is simple, but not easy. Learn how to navigate the complexities of your investment strategy with discipline and sound advice.

Read more

Article

Financial Life Management

How to use probability in finance to make better decisions

Learn how probability is used in decision making, from probability in statistics to business, finance, and trading applications. Understand market probability with real examples.

Read more

News

Financial Life Management

How understanding financial beliefs can lead to better money decisions

How inherited money beliefs shape — and sometimes sabotage — the financial choices we make.

Read more

Article

Financial Life Management

Wealthy expats in the UAE: 5 money secrets you should know

Wealthy expats in the UAE: Discover the financial secrets of the wealthy how to avoid common traps that hinder wealth accumulation.

Read more

Article

Financial Life Management

How much of your portfolio should be in 'shiny and exciting' investments?

Discover why a simple, diversified portfolio is the key to long-term financial success in investing, despite the allure of 'shiny' opportunities.

Read more

Article

Financial Life Management

Revealed: this is why you don't save enough or spend too much

Explore your relationship with money and how it impacts your financial decisions and financial health.

Read more

Article

Financial Life Management

The cost of living in Dubai for senior international professionals [3 points to consider in 2024]

Cost of living in Dubai for senior international professionals. Are you factoring these 3 costs into your financial plan? Updated for 2024.

Read more

News

Financial Life Management

Why your spending must align with your values

Why meaningful spending — not just budgeting — is the real key to financial contentment.

Read more

Article

Financial Life Management

This is what 'bad behaviour' as an investor looks like

Discover the impact of bad investor behaviour and how to combat market volatility with a diversified portfolio.

Read more

Article

Financial Life Management

How to navigate life's inevitable changes (financial, family, work, health and legacy)

Learn how to navigate life's constant changes by embracing resilience, coping strategies, and managing expectations.

Read more

News

Employee Benefits

From burnout to balance and the role of law firm health policies

How progressive health policies help law firms protect their people and retain top talent.

Read more

Article

Financial Life Management

Why 'more money' is NOT a goal

Discover why pursuing 'more money' should not be your goal. Learn how to shift your focus towards embracing 'enough' for a fulfilling and independent future.

Read more

Article

Financial Life Management

The Trump-Biden battle begins: how will markets react?

The Trump-Biden battle begins: Discover how markets may react to the US election.

Read more

News

Financial Life Management

Why true happiness lies beyond money

The research-backed limits of wealth as a driver of wellbeing and what actually matters more.

Read more

Article

Financial Life Management

"How can I maximise my returns in the short term?"

Learn how to navigate the complex world of investing by asking the right questions and focusing on long-term financial goals.

Read more

Article

Financial Life Management

How do elections affect the stock market?

Explore how elections worldwide impact the stock market and why trying to predict outcomes may be futile.

Read more

Article

Financial Life Management

The surprising truth: children likely increase your wealth

Discover the surprising truth: parental responsibilities can lead to better financial habits and planning for the future.

Read more

News

Financial Life Management

Why a good financial plan doesn't have to be complicated

Why simplicity — not complexity — is the hallmark of a truly effective financial plan.

Read more

Article

Financial Life Management

"Aside from the activity I see, what else is happening with my investments?"

Discover the hidden investment activities on your portfolio and the importance of a systematic approach to achieve long-term financial success.

Read more

Article

Financial Life Management

Do you need a financial health check? Here's how to tell

Learn how to give your finances a health check with expert advice on stopping financial bleeding, stabilising your finances, and building long-term wealth.

Read more

Article

Financial Life Management

Is it wise to begin investing when stocks are at an all-time high?

Andrew Hallam, author of Millionaire Teacher, shares why all-time highs don't scare him when it comes to investing, as well as his strategy for success.

Read more

Article

Financial Life Management

The role your emotions play in high-stakes decisions

Why diversification is key to avoiding FOMO and regret in investing, and how a well-diversified portfolio can optimise long-term returns.

Read more

News

Financial Life Management

Why avoiding temptation is an investor's most important skill

Why resisting short-term impulses is the defining skill that separates successful investors.

Read more

Article

Financial Life Management

Why diversification means you don't need to worry about FOMO or regret

Discover why diversification is key to avoiding FOMO and regret in investing, and how a well-diversified portfolio can optimise long-term returns.

Read more

News

Employee Benefits

Telemedicine: How soon will UAE residents get comfortable with online consultations?

Exploring the adoption curve for telemedicine and what's driving or slowing uptake among UAE residents.

Read more

Article

Financial Life Management

The stock market is volatile for the first time this year. Here's what to do

Understand market volatility and embrace the fluctuations as a long-term investor. Learn how to navigate market declines and stay focused on your financial goals.

Read more

Article

Financial Life Management

Should you begin investing now, or wait?

Learn why starting your investment journey now is crucial. Waiting could cost you thousands. Dive into the data with Andrew Hallam.

Read more

Article

Financial Life Management

Your experiences with money make up 0.00000001% of what’s happened in the world, but 80% of how you think it works

Discover how your core financial beliefs shape your thoughts and actions in life. PLUS, find out your own money personality in two minutes.

Read more

News

Financial Life Management

Why money should be viewed as a tool and not a goal

Reframing the purpose of money as a means to a fulfilling life rather than an end in itself.

Read more

Article

Financial Life Management

Investment mistakes you don’t even realise you’re making [case study]

Learn about the hidden investment mistakes that could be costing you millions, without you even realising it.

Read more

Article

Financial Life Management

Investment risk and the importance of staying in the game

Learn about the importance of managing investment risk and staying in the game financially, and in life.

Read more

Article

Financial Life Management

Why you're scared of investing (and what to do about it)

Discover why fear holds you back from investing and learn practical ways to overcome it. Take control of your financial future and live with fewer regrets.

Read more

Article

Financial Life Management

What could you learn from a rich retiree who lives on $14,000 a year?

Andrew Hallam tells the inspiring story of a rich retiree living on $14,000 a year, sharing valuable insights on happiness, wealth, and living well without excessive materialism.

Read more

News

Financial Life Management

What are the steps to achieving financial freedom?

A practical framework for building genuine financial independence, step by step.

Read more

Article

Financial Life Management

Why your flourishing future is at risk if you don't have a clear strategy for your life

We know winning in life’s journey isn’t about ‘products’. And 'managing your money' is only the tip of the iceberg.

Read more

Article

Financial Life Management

Dare to compare your investment results with your colleagues and friends?

Discover why comparing your investment results to others can be misleading and how a diversified portfolio of index funds can outperform most hedge fund managers...

Read more

Article

Financial Life Management

Feeling unmotivated to make a change? Use this simple tool to find out why

Feeling unmotivated? Discover the reasons and learn how to tap into your existing motivation to make positive changes in your life.

Read more

News

Financial Life Management

Seven ways to achieve your money goals

Actionable steps for setting meaningful financial targets and following through on them.

Read more

News

Employee Benefits

UAE HR managers need more than price quotes to pick right group health insurance

Why HR leaders must look beyond cost when selecting employee health cover — and what to consider instead.

Read more

Article

Financial Life Management

7 powerful financial levers to take control of your financial situation

Take control of your financial situation with these 7 powerful financial levers.

Read more

Article

Financial Life Management

A retirement haven for the rich and the budget-conscious

Discover this European paradise for retirees and digital nomads. With stunning landscapes, low living costs, enticing tax schemes, and affordable healthcare, it's a haven for the rich and budget-conscious...

Read more

Article

Financial Life Management

This simple scale shows how close you are to mastering your wealth

Don't let another year slip away without reaching your full potential. Demand more from yourself and unlock your flourishing future.

Read more

News

Financial Life Management

Is money the key to a good life?

Examining whether wealth is truly the foundation of a good life or if other factors matter more.

Read more

Article

Financial Life Management

What money can't buy: the four dials of a well-lived life

Discover the four key factors that contribute to a well-lived life, and which of these factors money can impact.

Read more

Article

Financial Life Management

Does currency hedging make a difference for investors?

Discover the impact of currency hedging on investor returns and portfolio volatility, and whether it makes a difference for global stocks and bonds.

Read more

Article

Financial Life Management

From indexing to systematic investing: Nobel prize-winners know best

Discover how Nobel prize-winner David Booth helped revolutionise investing through indexing and systematic investing.

Read more

Article

Financial Life Management

Why so many investors buy into complexity, when simple will do

Discover why so many investors are drawn to complexity when simplicity is often the better choice.

Read more

Article

Financial Life Management

What should you do with free or discounted company shares?

Discover what to do with free or discounted company shares and the risks and benefits of keeping or selling them.

Read more

News

Financial Life Management

Why a calm investment philosophy is key to financial success

How staying composed and avoiding reactive decisions is central to achieving long-term financial success.

Read more

Article

Financial Life Management

Is your wealth really destined to disappear after three generations? The truth about this fear-based myth

Dispelling the myth that intergenerational wealth transfers fail. Learn how a positive and purposeful approach can lead to successful outcomes.

Read more

Article

Financial Life Management

The paradox of wealth: Why the wealthy worry about losing it all

Explore the fears and anxieties that plague the very wealthy, and learn how loss aversion and money beliefs shape their mindset.

Read more

Article

Financial Life Management

Structured products - what lies beneath...

Discover the hidden truth about structured products and why they may not be the best choice for long-term investors.

Read more

Article

Financial Life Management

Why this European retirement destination is a longstanding favourite

Discover why this place is a beloved retirement destination. From stunning landscapes to its affordable cost of living and excellent healthcare.

Read more

Article

Financial Life Management

Here's what returns you can really expect from the stock market

Learn what returns you can realistically expect from the stock market for your retirement planning.

Read more

Article

Financial Life Management

Why you shouldn't tell your children to invest

Discover why telling your children to invest may hinder them. Learn a better strategy that allows them to make smarter financial decisions.

Read more

News

Financial Life Management

How to make your money work for you

Practical strategies for putting savings and investments to work rather than letting them sit idle.

Read more

Article

Financial Life Management

“I’m an engineer in Dubai with a UK pension. Should I transfer to a QROPS or a SIPP?”

What's the difference between a SIPP and a QROPS? And are you making the right decision to transfer your executive pension?

Read more

Article

Financial Life Management

“Our retirement withdrawal plan beats the 4% rule,” say these clever retirees

Thinking about retirement and portfolio withdrawals? Discover how Roberto and Gwen challenged the conventional 4% rule and embraced Guyton and Klinger's flexible approach.

Read more

News

Employee Benefits

UAE medical insurance needs more ways to keep rates in check

Why the UAE's medical insurance market needs stronger mechanisms to control escalating premiums.

Read more

Article

Financial Life Management

The only formula you'll ever need for creating secure, easy-to-remember passwords for everything

Discover the superpower to creating secure and easy-to-remember passwords that will protect you from hackers.

Read more

Article

Financial Life Management

How two lawyers, currently earning $500,000, admit they struggle to make ends meet (case study plus our thoughts)

Two high-earning lawyers have a combined salary of $500,000, but why is it still not enough? We share our thoughts on this couple's spending.

Read more

Article

Financial Life Management

Why this is Europe’s favourite retirement destination

Discover why this is Europe's top retirement destination. With its beautiful beaches, friendly locals, and affordable cost of living, it's no wonder retirees are flocking to this charming country.

Read more

News

Financial Life Management

How lifestyle creep can derail your financial plans

The quiet danger of upgrading your lifestyle as income grows — and how it erodes long-term wealth.

Read more

Article

Financial Life Management

The most powerful tool EVER for your finances (and how you can use it today)

Find out how starting investing early can lead to significant wealth accumulation.

Read more

Article

Financial Life Management

Could you pass the game show test if you wanted to buy gold?

Discover the surprising truth about gold as an investment - is it as stable and lucrative as you think?

Read more

Article

Financial Life Management

Dimensional vs. Vanguard

Dimensional and Vanguard: Why a chartered financial planner will make either choice more successful for successful families living overseas.

Read more

Article

Financial Life Management

Should you invest with a financial adviser? (Here's what the research says)

Discover how Vanguard's research proves advisers can add value to investors' bottom lines through these five points...

Read more

Article

Financial Life Management

This could be the world's best investing checklist

Learn from the wisdom of Charlie Munger and improve your investment strategy with these ten timeless principles.

Read more

Article

Financial Life Management

Should I pay off my mortgage early or boost my pension?

Should you pay off your mortgage early or boost your pension? Explore the pros and cons, considering interest rates, investment growth, and your age.

Read more

News

Employee Benefits

UAE health insurance: Will residents pay higher co-payment charges on their medical bills in 2024?

Whether UAE residents face higher out-of-pocket medical costs as insurers look to manage rising claims.

Read more

Article

Financial Life Management

What’s the perfect investment allocation?

Discover the perfect investment allocation to suit your personality and financial goals, and learn why there's no one-size-fits-all approach to investing.

Read more

Article

Financial Life Management

The pros & cons of owning a rental property vs. stock market investing

Explore the pros and cons of owning a rental property vs. investing in the stock market. Discover why property is a popular investment and the psychological benefits it offers.

Read more

News

Financial Life Management

Why mindset is just as important as money for a happy retirement

How attitude and psychological preparedness shape retirement satisfaction as much as financial readiness.

Read more

Article

Financial Life Management

Is investing in the S&P 500 a good idea?

Is investing in the S&P 500 a good idea? Discover the past performance, active management, and the benefits of diversification in this insightful blog post.

Read more

Article

Financial Life Management

Why do these investors want their portfolios to drop?

Discover why some investors actually want their portfolios to drop in value and how these individuals take advantage of market downturns...

Read more

Article

Financial Life Management

How to plan for an unknown future: the positive side of uncertainty

Learn how to plan for the future when nothing is certain and discover the importance of resilience and non-financial ways to build strength.

Read more

Article

Financial Life Management

Achieving financial well-being: 25 actions for successful families living overseas

Achieve financial well-being and secure your family's future with these 25 actions for successful families living overseas.

Read more

Article

Financial Life Management

This is your money personality - and it's driving all your financial decisions

Your money personality is driving your financial decisions. Uncover the beliefs that shape your financial choices and learn how to improve.

Read more

News

Financial Life Management

How can we overcome the fear of spending?

Understanding the psychological barriers that stop people enjoying their money and how to move past them.

Read more

Article

Financial Life Management

The Magnificent Seven stocks and what they mean for your portfolio

Discover the significance of the Magnificent Seven stocks in the Nasdaq 100 and what this means for your portfolio.

Read more

Article

Financial Life Management

How much money do you need for a rich retirement? (includes 5 different cities)

Discover how much money you need for a rich retirement in different cities around the world.

Read more

Article

Financial Life Management

Should you add gold to your portfolio?

Discover the truth about investing in gold. Is it really a safe haven, a good hedge against inflation and a good addition to your portfolio?

Read more

Article

Financial Life Management

How this couple retired early and how you could too

Find out how you can retire early and live a fulfilling live, just like this couple did. All it takes is careful planning and tough choices.

Read more

Article

Financial Life Management

The secret to spending more in retirement, without ever running out of money

Discover how you can enjoy a comfortable retirement without the constant worry of depleting your savings.

Read more

Article

Financial Life Management

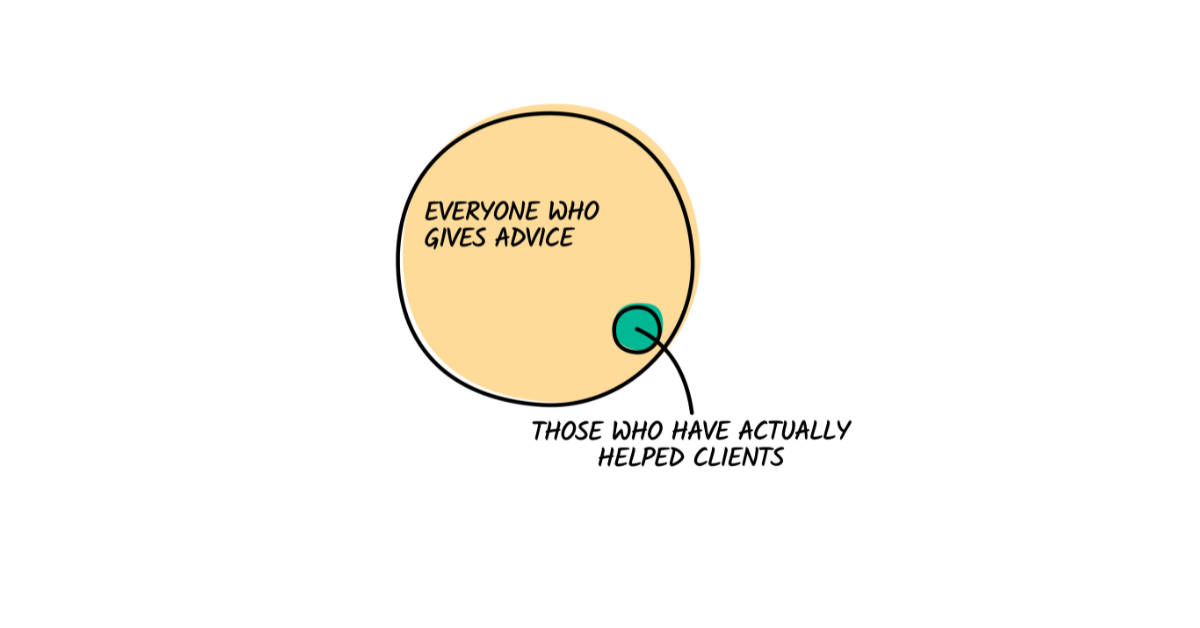

What is good (and bad) financial advice?

Discover the importance of good financial advice and, perhaps more importantly, what constitutes bad financial advice (with 3 areas to watch out for).

Read more

News

Financial Life Management

Why the power of memory can lead to sound financial choices

How drawing on past financial experiences — good and bad — can sharpen future money decisions.

Read more

Article

Financial Life Management

Why the 60/40 portfolio is not dead

Discover why the 60/40 portfolio is not dead and why including bonds in your investment strategy is crucial.

Read more

Article

Financial Life Management

How will lower birth rates affect pensions, stocks and property?

Lower birthrates coupled with longer lifespans are going to make an increasing retirement age inevitable...

Read more

Article

Financial Life Management

The only 6 questions you need to ask when choosing who manages your money

Time-poor people often do little or no research before meeting a financial adviser. The result is trusting your gut instinct. Here's why this is a bad idea...

Read more

Article

Financial Life Management

Could you match the investment returns of my dead Uncle Arthur?

If Uncle Arthur had a diversified portfolio of index funds, he'd have thrashed the investment performance of almost everyone you know. Here's how.

Read more

Article

Financial Life Management

Renting vs. buying: A simple calculation to help you decide

How do you approach the rent vs. buy decision? Here's my simple calculation to help.

Read more

Article

Financial Life Management

Warning: Avoid these investments like the plague, says Buffett and Munger

On an equal risk-adjusted basis, private equity and hedge funds don’t beat the long-term performance of a diversified portfolio of index funds...

Read more

Article

Financial Life Management

Offshore savings plan? Here's what's changed since you signed up

Holding an offshore savings plan? Here's what it actually costs, where it came from, and how to find out if a better option now exists.

Read more

Article

Financial Life Management

Unpopular opinion: high dividend stocks don't make the best investments

Long term, a stock’s price increase is directly related to the rise in that company’s intrinsic value. The more money that company gives away in dividends, the less potential its share price has to grow...

Read more

News

Financial Life Management

Why making your bed every day can boost your wealth

The link between daily discipline and habits and the financial behaviours that build long-term wealth.

Read more

Article

Financial Life Management

Here's how a cycle crash led to an important lesson in business and life

Research suggests that when we commit to random acts of kindness, it improves our strength, our life satisfaction and our health...

Read more

Article

Financial Life Management

10 key principles of our investment philosophy

Investment philosophy is a really big subject. So we’ve distilled the key points of our own investment philosophy into 10 key things to remember.

Read more

Article

Financial Life Management

Are you rich, or are you wealthy?

Rich and wealthy may seem like similar words, but they hold entirely different meanings that can play a crucial role in shaping your financial destiny.

Read more

Article

Financial Life Management

No sugarcoating: What would happen if everyone invested in index funds?

If every penny in the markets were invested in index funds, we would have a broken market...

Read more

News

Financial Life Management

Why it's OK not to know everything about investing

Why embracing uncertainty and humility — rather than overconfidence — leads to better investment outcomes.

Read more

News

Employee Benefits

Are your group medical claim numbers so far this year already giving you heartburn?

What rising group medical claims mean for UAE businesses and how to get ahead of escalating costs.

Read more

Article

Financial Life Management

UK National Insurance and the State Pension - here's what expats need to do (step-by-step)

The deadline is fast approaching for UK expats to plug any gaps in their UK National Insurance contributions - here's what you need to do.

Read more

Article

Financial Life Management

Periods when to make money chart: when to buy & sell using the Benner Cycle

Periods When to Make Money chart explained using the Benner cycle chart and Samuel Benner chart, including periods when to make money PDF and Google Benner cycle chart insights.

Read more

Article

Financial Life Management

How to build (and destroy) generational wealth

Learn the secrets to building and preserving generational wealth while avoiding common pitfalls that can lead to its demise.

Read more

Article

Financial Life Management

How much can retirees withdraw from their investments each year?

People assume they can see the future. Nobody can, of course. Regardless of what happens, flexibility is key. Use the 4 percent rule as a base, and operate from there.

Read more

News

Financial Life Management

Happiness and wealth: why you can't have one without the other

Exploring the relationship between financial security and happiness — and why each depends on the other.

Read more

Article

Financial Life Management

An ideal climate and great benefits - could this be the perfect retirement haven?

From the weather to the perks, learn why this place might just be the perfect spot to settle down and enjoy your golden years.

Read more

Article

Financial Life Management

Is this 46-year-old woman saving enough to retire? Some simple maths can help

Backtested studies suggest that if a retiree withdraws 4 percent of their portfolio’s value during their first year of retirement, and increases the withdrawals each year to reflect the rising cost of living, the money should last at least 30 years, if it’s invested in a diversified portfolio of index funds.

Read more

Article

Financial Life Management

What happened to SVB? I'll explain

Silicon Valley Bank (SVB) was thriving. Credit losses were fairly low and it enjoyed a tripling of deposits between 2019 and 2021. So, what happened?

Read more

Article

Financial Life Management

Longer, better, happier: Unveiling the surprising key to longevity in retirement

Conventional retirement might be over-rated. I’m not suggesting you die at your desk. But research suggests a flexible view of retirement might beat retiring early.

Read more

Article

Financial Life Management

7 Japanese concepts to transform your life ( Japanese way of living )

Discover the Japanese way of living through 7 Japanese principles of life, including kaizen and ikigai. Explore Japanese philosophy, rules, and timeless life principles

Read more

Article

Financial Life Management

10 Essential Questions for Long-Term Investors to Ask in 2024

Explore 10 key questions every long-term investor should ask in 2024. Learn how to assess mutual fund performance and refine investment strategies for success.

Read more

News

Employee Benefits

Making gains from a group insurance cover? It is possible

How UAE businesses can structure group insurance to deliver genuine value rather than just compliance.

Read more

Article

Financial Life Management

Most British expats are wrong about the taxes they’ll pay after moving back to Britain

Calling all British expats moving home. Don't get caught out by tax misconceptions.

Read more

News

Financial Life Management

Here's what living to 100 means for your investment portfolio

How dramatically longer lifespans should reshape the way people approach retirement and long-term investing.

Read more

Article

Financial Life Management

Looking for a magic formula in investing? This is it

Looking for a magic formula for successful investing? This is the closest you'll get.

Read more

Article

Financial Life Management

Is your praise and support making your children weak?

Not experiencing failure or criticism can impact even the most gifted kids. When kids don’t face adversity, can they overcome life’s challenges as adults?

Read more

Article

Financial Life Management

The value of probabilistic thinking [plus 3 examples for investors]

This mental model involves trying to estimate, using maths and logic, the likelihood of an outcome. Including 3 examples from the world of investing.

Read more

Article

Financial Life Management

[Updated for 2023]: The differences between QROPS, QNUPS and SIPPs

If you’re researching your pension options, this comparison of QROPS, QNUPS and SIPPs is for you. updated for 2023.

Read more

Article

Financial Life Management

7 simple ways to avoid UK inheritance tax in 2023 [plus a case study]

Stop the taxman stealing your children's future wealth with these 7 simple & effective ways to avoid UK inheritance tax. Updated for 2023.

Read more

Article

Financial Life Management

Cutting through confusion: how to apply Hanlon's razor

Discover the essence of Hanlon's razor and how to apply it in your daily life. Learn practical tips on how to make better, more rational decisions.

Read more

Article

Financial Life Management

Hidden paradise: this retirement location may be the world's best-kept secret

Luxury retirement rarely comes cheap. If you’re looking for a piece of paradise, this may be one of the world’s best countries.

Read more

Article

Financial Life Management

Expat Guide to UK Property Tax: Understanding Stamp Duty and SDLT in 2024

Learn all about UK property tax, including SDLT and stamp duty, in this comprehensive expat guide. Get insights on how property taxes work for expats in 2024.

Read more

Article

Financial Life Management

The truth behind what really moves share prices

Actively managed funds that perform well during one time period usually lose their winning way. That’s why we should build and maintain a diversified portfolio of index funds or ETFs...

Read more

News

Financial Life Management

Why 'second-order' thinking is a powerful tool for money management

How thinking through the consequences of consequences leads to smarter, less reactive financial decisions.

Read more

Article

Financial Life Management

What I'm reading: How to use Occam's razor to simplify problems and solve them quickly and efficiently

Occam’s razor is one of the most misunderstood 'mental models'. But it's arguably one of the most useful. If you need a way to solve problems more quickly and efficiently... here’s how to use it.

Read more

News

Employee Benefits

UAE businesses cannot be thinking of employee health insurance as a cost

Why treating employee health insurance as a strategic investment — not an overhead — changes business outcomes.

Read more

Article

Financial Life Management

The 60/40 portfolio had a hard time offering investors much support last year. Is it still relevant?

Many are questioning if the 60/40 portfolio is still relevant, especially after last year. Here's what I think.

Read more

Article

Financial Life Management

What I'm reading: Thinking backward and the power of avoiding obvious stupidity

First-order thinking is quick and easy. “I’m hungry, I’m going to eat cake”. Second-order thinking is more thoughtful. It makes you consider the impact.

Read more

Article

Financial Life Management

What we can learn from the best and worst-performing bond funds of 2022 (plus a look at my own investments)

Bonds fell in 2022. But how far your bond funds fell depended on the risk you took… whether you realised that or not.

Read more

Article

Financial Life Management

How smart people use second-order thinking to outperform

First-order thinking is quick. “I’m hungry, I’m going to eat cake”. Second-order thinking is more thoughtful. It makes you consider the impact.

Read more

Article

Financial Life Management

5 types of recession, when they've happened and the dream scenario we all hope for (plus the nightmare to avoid)

We can't see into the future, but understanding the nature of each recession helps us better prepare for the next.

Read more

Article

Financial Life Management

What I'm reading: Circle of competence and how Warren Buffett avoids problems

Knowing what you don’t know, helps you understand what to avoid and improves decision-making and outcomes...

Read more

Article

Financial Life Management

What I'm reading #52: The world’s greatest mental models...How Elon Musk uses first-principles thinking to achieve exponential results (and you can too)

What is first-principles thinking, used by Elon Musk, and what can it do for you?

Read more

Article

Financial Life Management

The parable of the Mexican fisherman - and how your life has become bloated with unnecessary desires

The parable of the mexican fisherman is a chance to reflect on the life you're pursuing.

Read more

Article

Financial Life Management

What I'm reading #51: The map is not the territory

In the Army, before GPS, I spent A LOT of time learning ways to make sure we were in the right place at the right time. But a map of reality is not reality.

Read more

Article

Financial Life Management

Thailand: How to retire like the rich, even if you aren't yet

You could have a smaller retirement portfolio than your friends, retire earlier, and live far more luxuriously than almost everyone you know...

Read more

Article

Financial Life Management

After the latest stock market crash, it's time to invest in a 'safe' asset like gold instead. After all, gold can't perform any worse than your portfolio has, right?

Anyone who jumped into gold after giving up on a diversified portfolio of stocks and bonds missed out on a lot of money...

Read more

Article

Financial Life Management

The world's richest people DON'T do this

Your odds of success will always be better with stocks and properties. Here's the truth behind Forex trading...

Read more

Article

Financial Life Management

The recent predictions from Barclays and Goldman Sachs have investors immediately questioning their strategies next year (read before you act)

It’s the most wonderful time of the year. Wall Street’s top strategists share where they see the stock market heading. And it's sceptical about 2023.

Read more

Article

Financial Life Management

Over a period of 35 years, index fund investors earn 100 percent more money than those who buy actively managed funds

Fear, greed, under confidence and overconfidence impact most investors. The trick is to stay the course with a portfolio of low-cost index funds and then stay out of your own way.

Read more

Article

Financial Life Management

22 years ago, I was James Blunt's boring housemate. Now, I'm an equally boring investor

I've built a business around being boring, based on decades of Nobel prize-winning research. Because quite frankly, boring is better for investors.

Read more

Article

Financial Life Management

What the psychology of rats can teach you about lump sum investing

Lump-sum investments don’t always win. But, investing a lump sum, as soon as you have it, usually beats dollar cost averaging...

Read more

Article

Financial Life Management

Have you read Rich Dad, Poor Dad by Robert Kiyosaki? By listening to his beliefs, and not this proven stock market secret, you're missing out on the world's best predictor of future performance

CAPE, or Cyclically Adjusted Price to Earnings ratio, may be the world's best kept secret on future stock market performance.

Read more

Article

Financial Life Management

The 5 fundamentals about the stock market you need to know

It's easy to get distracted by the financial media. Here are 5 fundamental things about the market everyone needs to remember.

Read more

Article

Financial Life Management

If you're investing in highly diversified portfolios right now, keep adding money. You have ground beneath your feet. Everyone else is on thin ice

If you don't own a globally diversified portfolio right now, you're skating on thin ice for when the market recovery comes.

Read more

Article

Financial Life Management

Goldman Sachs has lowered it's prediction for the S&P 500 four times this year alone. But being a long-term investor means stomaching short-term guesses...

The beauty of the market lies in the fact that nobody knows what's around the corner. Not even the greatest minds on Wall Street.

Read more

Article

Financial Life Management

What I'm reading #41: Stupidly simple habits I've discovered to have the highest ROI

Investing time into high-ROI habits or daily rituals will make you both money and happiness. The goal is to focus on habits or daily rituals that work for you.

Read more

Article

Financial Life Management

Most rich-looking people are just folks with high salaries who spend a lot. Discover how the fake rich and your work colleagues could be hurting your wealth

Most wealthy people spend less than you think. If you want to build wealth, it might be best to model the spending habits of those who are truly rich.

Read more

Article

Financial Life Management

Scared about how you can protect your wealth while the global stock market crashes? The answer lies 2000 years ago in ancient Greek mythology

As global markets plunge, what action can you take to save your portfolio?

Read more

Article

Financial Life Management

Scared about running out of money in retirement? This doctor's repeat prescription for bear and bull markets means you'll never have to worry about it ever again

So far in 2022, diversified portfolios of stocks and bonds haven’t fallen anything close to the nightmarish plunges that followed 1929, 1973, 2000 or 2008.

Read more

Article

Financial Life Management

What I'm reading #39: How to apply compound interest to your everyday life

One of the most common denominators in the story of every ‘successful’ person out there: compounding.

Read more

Article

Financial Life Management

Answer 2 super simple questions to reveal if you could own a horrible financial product, and not even know it

Some investment schemes, sold prolifically in the Middle East, are like kayaks with multiple hidden holes. Could you own one of them?

Read more

Article

Financial Life Management

Anyone questioning their 60/40 investment portfolio right now needs to ignore the Google results, and read this

It's true, this go-to portfolio strategy (has suffered one of its worst years on record. But I'm still backing it.

Read more

Article

Financial Life Management

This retired professor asked his students every year how much money it would take for them to spend a year in prison. Their answer might shock you

If more money continued to boost life satisfaction, the wealthiest people you know would be the happiest. But we know that isn’t true...

Read more

Article

Financial Life Management

Single-stock ETFs: a daily dopamine rush for the brain, but a risky business for 99% of investors

Single-stock ETFs have arrived. Find out what they are and whether they pose an opportunity for the long-term investor.

Read more

Article

Financial Life Management

Why Warren Buffett bought Apple years ago, and the crazy difference between growth and value stocks over time

Most investors solely chase growth stocks. Warren Buffett, the world's greatest investors, had a different strategy...

Read more

Article

Financial Life Management

Bearish or bullish? Why our brains aren't hard wired to handle the vast amount of information thrown at us now

Right now, it's easy to be labelled "bearish". But for the long term investor, the term has no meaning. Find out why.

Read more

Article

Financial Life Management

Facebook, Tesla, Google and Netflix...I can hear what you're thinking. Record profits equal exciting prospects for investors. Think again.

Savvy stock buyers know that it takes more than rising business profits to make a stock keep rising. Instead, there are three main influences...

Read more

Article

Financial Life Management

Time and time again, the wealthy financially sabotage their kids' futures (spoiler alert: it doesn't stop in childhood)

One family generation builds the wealth. The next generation maintains it. The third generation destroys it. But how can this be avoided?

Read more

Article

Financial Life Management

Anyone who will be adding money to the markets for at least the next five years, needs to try this test now

Warren Buffett’s rule of thumb: Anyone who will be adding money to the markets for at least the next five years should prefer to see stocks fall, not rise.

Read more

Article

Financial Life Management

Ignore Cathie Wood: ARK investors aren't earning anywhere near those who follow this simple plan

History doesn’t repeat itself, but it rhymes. In 2020, share prices in several technology stocks went through the roof. Have we been here before?

Read more

Article

Financial Life Management

The 7 truths of my basic investment philosophy

Having a investment philosophy is vital to keeping you disciplined. Here's mine.

Read more

Article

Financial Life Management

7 timeless investing principles

Successful investing ultimately boils down to simple, common sense ideas. Simple however, does not mean easy.

Read more

Article

Financial Life Management

What I'm reading #29: 45 cognitive biases of today's world

Understanding our cognitive biases is fundamental to lowering risk and improving investment returns over time...

Read more

Article

Financial Life Management

The world’s best stock market tip

According to Andrew Hallam, the world’s best stock market tip is the one that helps the greatest number of people over the longest length of time...

Read more

Article

Financial Life Management

How to maximise your stock market returns

Every investment strategy has pros and cons. But I do believe a "good" strategy you can stick with, is much better than a "great" strategy you can’t.

Read more

Article

Financial Life Management

Warning: The danger of chasing meme stocks [case study]

Chasing individual names in hopes of catching a meme-stock phenomenon may be tempting, but the data are clear that it’s a big gamble.

Read more

Article

Financial Life Management

2022: A review at half time

The first 6 months of 2022 were pretty interesting for financial markets. It was one of the worst 6 month periods we've ever seen for stocks and bonds.

Read more

Article

Financial Life Management

How to transfer your Shell pension (Shell Overseas Contributory Pension Fund/SOCPF)

If you have a Shell pension (Shell Overseas Contributory Pension Fund/SOCPF) and are nearing retirement, you’re likely considering how best to transfer it.

Read more

Article

Financial Life Management

Sitting on cash during a bear market? Here's what to do

This bear market differs from others in recent history. So what should you consider if you have extra cash to invest?

Read more

Article

Financial Life Management

Bear markets: 5 things to remember

We are officially in a bear market. Here are five lessons I think investors should remember during this time.

Read more

Article

Financial Life Management

What I'm reading #24: Wilful blindness: why we ignore the obvious at our peril

This week, over a trillion dollars has been lost in crypto-currencies. Why, after every major blunder, do we look back and say, how could we have been so blind?

Read more

Article

Financial Life Management

One simple way to get your children interested in investing

Success in investing often has more to do with the time you have in the market than anything else. Here's how I will ensure my children start early...

Read more

Article

Financial Life Management

Crypto, gold and oil vs. the stock market

Crypto, gold, oil, value and growth investing. What does the data tell investors about how to build their long-term investment strategy?

Read more

Article

Financial Life Management

Zurich Vista Savings Plan review: fees, features, and risk factors

A review of Zurich Vista Savings Plan covering how it works, who it suits, the key risks, and whether the structure is worth the cost.

Read more

Article

Financial Life Management

What I'm reading #19: Guard your brain attic

In the world we live today, there is so much negative news through social media and television. What does that do to your mind and thinking?

Read more

Article

Financial Life Management

The current state of the markets: 5 questions answered

This week, I'm answering 5 questions about the current state of the markets.

Read more

Article

Financial Life Management

DIY investing vs. the stock market

Lagging performance by active fund managers isn't a new story. Neither is concern over fees charged by financial professionals. But is the solution to DIY?

Read more

Article

Financial Life Management

What I'm reading #15: A secret to solving the most difficult problems

Inversion is the secret to solving the most difficult problems in life, like money, and a way of thinking about what we want by considering it in reverse...

Read more

Article

Financial Life Management

How should affluent investors understand and deal with risk?

How should affluent investors understand and deal with risk? And how do DIY investors perform? Discover more in this blog.

Read more

Article

Financial Life Management

What I'm reading #14: The only scorecard that matters

Social media has taken this idea of ‘wanting to look good’ to a different level. Our happiness and satisfaction now come from how many followers we have...

Read more

Article

Financial Life Management

Goals vs. capital: Are yours aligned?

Although goals vary greatly from person to person, they can be organised within a formal investing framework. Are your goals and capital aligned?

Read more

Article

Financial Life Management

How to safeguard your family’s financial future

We help clients successfully navigate many life transitions. This blog looks at the hardest of them all, how to safeguard your family’s financial future.

Read more

Article

Financial Life Management

The 7 benefits of offshore banking

What are the benefits of offshore banking for expats and international professionals? Discover the advantages of offshore banking in this guide.

Read more

Article

Financial Life Management

Your expat guide to UK residency rules - Part 1

Expat guide to UK residency rules and their impact on senior international professionals.

Read more

Article

Financial Life Management

Family holiday home or estate: To pass on or sell?

Anyone who has ever shared property with other family members will tell you, it takes work. Should you pass on your family home, or sell?

Read more

Article

Financial Life Management

Can you time the market to maximise growth?

This week, a reader asked me, "how can I time the market to maximise growth?" Find out why this the LAST thing investors should try, and how attempting it could be a costly mistake.

Read more

Article

Financial Life Management

[Updated for 2022] The biggest risks of the 4% retirement rule

You’ve probably heard of the ‘4 percent rule’, used to determine how much a retiree should withdraw from a retirement account each year. But how does it stand up when tested against market conditions and inflation?

Read more

Article

Financial Life Management

How to maintain wealth: 7 mistakes the super affluent avoid

Over the years, we've seen many clients make mistakes when building their wealth. However, these mistakes seldom occur with the savvy affluent. Why?

Read more

Article

Financial Life Management

How to cure behavioural bias

Of all the behavioural biases that hamper our performance as investors, arguably the most pervasive and the most destructive is overconfidence.

Read more

Article

Financial Life Management

What I'm reading #8: Never ignore opportunity costs

Each decision we make has consequences with it, that are both good and bad. Getting the most out of life means using your time and money wisely...

Read more

Article

Financial Life Management

The 4 best investment platforms for global investors right now

Find out what 4 platforms AES International think are the best for senior international professionals.

Read more

Article

Financial Life Management

What I'm reading #7: You control much less than you think

People often behave as though random events can be controlled. But we can't possibly control the many, complex factors that influence outcomes.

Read more

Article

Financial Life Management

Is it worth having a financial plan?

Is it worth having a financial plan? If you have significant net worth and aren’t sure if a financial/cash flow plan is worth the effort, keep reading.

Read more

Article

Financial Life Management

How to leave a £1.7 million legacy for your children

In his latest blog, David shares what how to retire wealthy and leave a £1.7 million legacy for your children.

Read more

Article

Financial Life Management

What I'm reading #4: A powerful force shaping your behaviour

Incentives drive nearly everything. Nothing I’ve seen in the financial services 'industry' has ever contradicted it.

Read more

Article

Financial Life Management

Does money make you happy?

For 75 years Harvard have conducted a study on 725 men to determine what makes us happy. Find out the results!

Read more

Article

Financial Life Management

What I'm reading #51: Focus on things you can control, that matter

If we don't want to lose our cool, we need to get crystal clear on what we want out of life. On the things that matter to us.

Read more

Article

Financial Life Management

What I'm reading #48: Eat your marshmallows, but keep some too

This week, read about the rewards from substituting the fleeting pleasure of instant enjoyment with the deep pleasure of earned enjoyment.

Read more

Article

Financial Life Management

What I'm reading #47: Believe in the magic of compounding

This week, read about the book Warren Buffet read aged 10, which changed his life forever.

Read more

Article

Financial Life Management

Why millionaires need this 3-point plan

This is the true story of one lottery-winning couple who were losing sight of their ideal future, because they were lacking one thing...

Read more

Article

Financial Life Management

How to save £175,000 of inheritance tax

In this blog, I’m going to show you how to shave £175,000 off your estate’s potential inheritance tax (IHT) bill.

Read more

Article

Financial Life Management

What are the 5 most common offshore investment bonds for international professionals?

In his latest blog, David Norton shares the 5 most common offshore investment bonds for international professionals.

Read more

Article

Financial Life Management

What’s the cost of delay? In this investor’s case: £659,500

In this blog, you'll learn the problem with delaying your investment over time.

Read more

Article

Financial Life Management

Why inflation is such a hot topic lately