A common challenge in personal finance, is deciding when to invest a sum of money.

You've just received a bonus (or 'distribution'), an inheritance, or sold your business.

Should you invest all that money over time, or now?

If you prefer video, I covered this very topic on my YouTube channel. Or you can watch it below.

This question comes up a lot when chatting with clients.

I understand the fear.

American economist Jeremy Siegel once said,"Fear has a greater grasp on human action than does the impressive weight of historical evidence".

There's often a lot at stake. Sometimes hundreds of thousands of pounds. Or more.

A common worry is,

"What if the market crashes right after I invest?"

"Wouldn’t it be better to stagger this amount over time to try and counteract any 'unlucky' timing?"

The shortest possible (and correct) answer to this, is 'NO'.

To begin, let's clarify some terms.

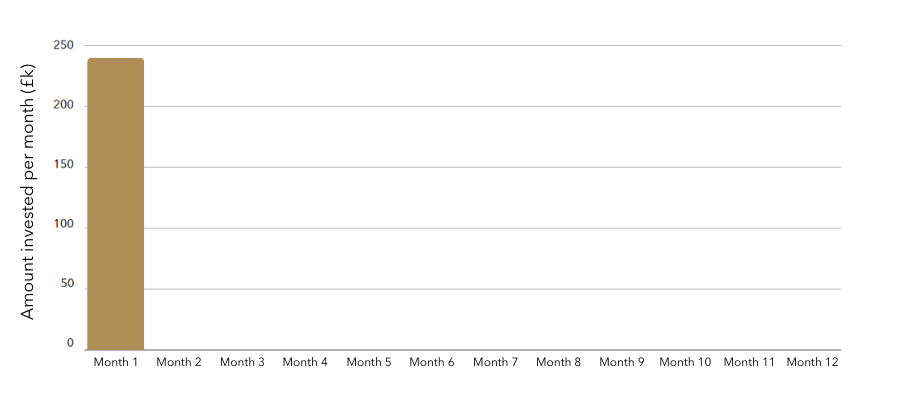

- Lump sum: Investing all your available money at once. The amount isn't important, only that the entire amount is invested immediately.

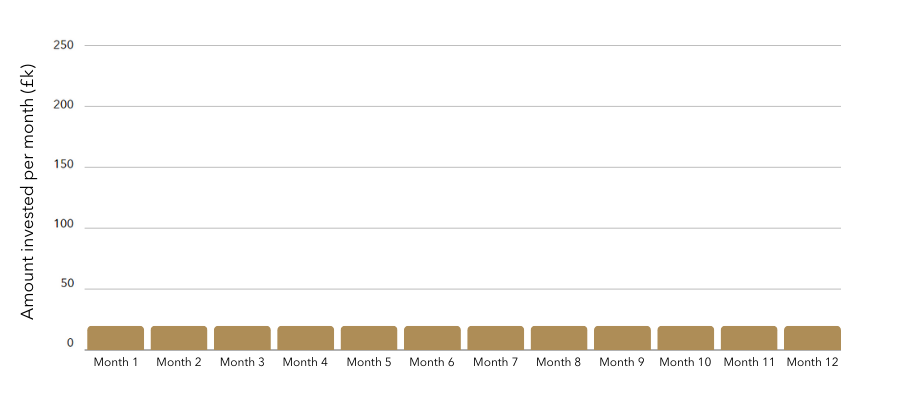

- Dollar-cost averaging (DCA): Investing all your available money over time. How you do this is your choice. However, the typical approach is equal-sized payments over a specific time period (i.e. one payment a month, for 12 months).

This is how each approach would look, investing £240,000 over 12 months:

Dollar-cost averaging

Lump sum investing

It may seem intuitive to want to drip your money into the market (say, over 12 months, as in the example above).

There's a perception that it helps you 'diversify' the cost of entry into the market, buying shares at prices that fall somewhere between the highs and lows of a fluctuating market.

But the problem comes when you consider that, over time, markets generally rise.

They go up 75% of the time and down 25% of the time.

These are good odds.

If the market increases in value each month during this example 12-month period, the DCA investor will pay a higher price on average than the investor who puts in a lump sum up front.

For a DCA strategy to work, the next 12 months would have to be the one period out of the four where the market produces a negative return (because DCA outperforms lump sum investing in falling markets).

BUT, falling markets are also when emotions run high, and sticking to a plan is most difficult.

In other words, the historical odds of DCA working, are three to one against you. You're simply more likely to buy in at higher average prices.

It doesn't matter what the time frame, either.

Whether 12 years or 12 months, the longer you wait to get your money invested, the more your purchasing power will be affected and the more you're likely to miss out on growth.

How to compare lump sum investing to dollar-cost averaging

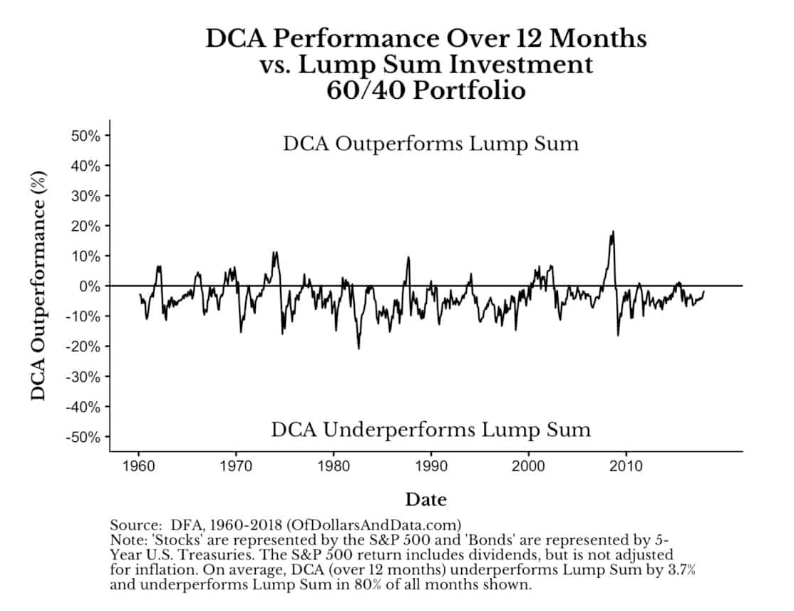

A neat way to compare the two strategies is to review how each of them grow, over the same buying period (again, 12 months, for example).

Once the period is over, whichever strategy has more money is the winner, and will continue to be going forwards (for example, if DCA has 10% more at the end of the 12 months, it will continue to return more in the subsequent months).

Below is a chart showing how DCA performed against lump sum investing in a 60/40 portfolio (this works for any portfolio over the long term, however, using a 12-month period) for each month from 1960-2018.

You can see the periods where DCA outperforms (when the black line is above 0%), are far less frequent.

In fact, the only times when DCA beats lump sum investing, is when the market is down (i.e. 1974, 2000, 2008, etc.). This is simply because, as mentioned earlier, DCA does well in falling markets because you're getting a lower average price than if you invested all at once.

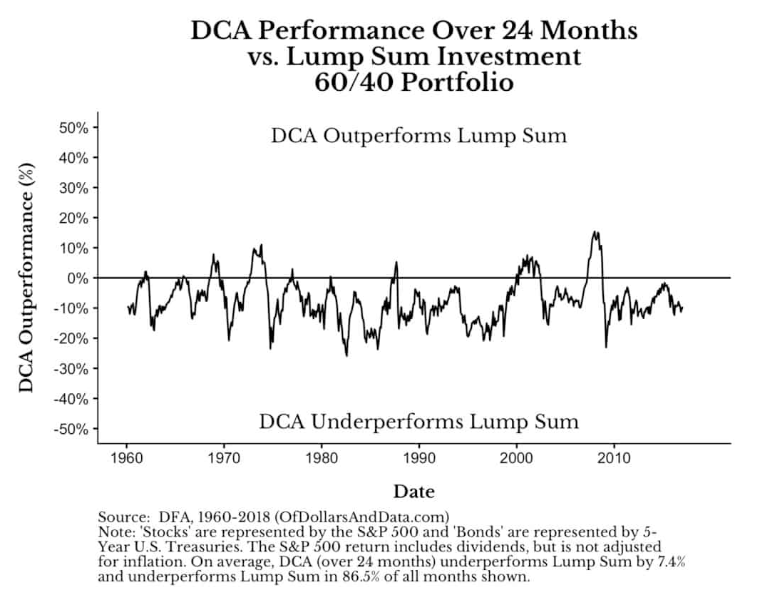

Let's look at another chart, this time showing 24 months:

The rate at which DCA outperforms lump sum investing is still clear.

If you're considering a DCA strategy now with your bonus or inheritance, you'd have to be lucky enough to start averaging-in during the handful of months above the 0% line.

Any fear you may have of a market crash needs to be balanced out by the fear of being left behind as the market shoots upward.

Is lump sum investing riskier?

Another question you'll need to ask yourself, if the above isn't compelling enough, is,

"What's my risk tolerance?"

If you're worried about a market crash, maybe your balance of risky and less risky assets isn't appropriate for you.

Is it riskier to invest a lump sum over dollar-cost averaging?

YES, it is.

Because you're investing everything right away, you get full asset class exposure.

But lump sum investing can still outperform even with a similar or lower risk portfolio.

In other words, you can still go all-in, but with a more conservative portfolio (for example, say you want to be invested in 100% stocks, but are worried about a market crash. Consider a 80/20 stock/bond portfolio, which would be better than dollar-cost averaging into an all-stock portfolio over time).

You need to ask yourself, what the largest amount of underperformance you could stomach is.

Once you know this, you can work with your financial life manager to find a portfolio that fits you AND still do a lump sum investment.

The cost of waiting

When deciding whether to invest a recent windfall all at once, or over time, the evidence is clear.

It's almost always better to lump sum invest, even on a risk-adjusted basis.

Remember:

- Every day your money isn't working for you, inflation is silently killing it.

- Every day you wait, you're paying the compounding cost of waiting.

- For investors with the goal of accumulating wealth, this is potentially a massive opportunity cost.

If you're still worried about investing your lump sum today, the problem may be that you’re investing in a portfolio that is too risky for your preferences.

Talk to a sage financial guide about a more conservative portfolio.

What’s clear is that markets have rewarded investors over time.

And time is your most important asset.

What's also clear is the greatest factor in your future financial success is likely entirely down to you - your own behaviour.

It’s not how you invest that’s by far the greatest factor in your future wealth success, so much as if and when you invest at all.

If you have no insight into how you behave and make decisions, it isn't surprising that so many miss out on the opportunity to create financial freedom now and in the future.