It's mid-point of the year, so a good time to look back again at the 60/40 portfolio...

Do 'experts' still predict it's demise?

There's a famous tale from 1895.

Mark Twain, while feeling unwell in London, discovered that a journalist had prematurely written his obituary.

Twain reportedly responded with, "The reports of my death are greatly exaggerated."

My thoughts on the the death of the 60/40 portfolio, are somewhat similar.

Successful investing is based on three essential elements:

- Using logical thinking to select the assets within your portfolio;

- Relying on empirical insights to understand long-term asset characteristics and their interactions (along with shorter-term exceptions); and

- Having the courage and discipline to stick with a sensible portfolio strategy during challenging periods.

By combining bonds and stocks in a portfolio, investors can strike a balance.

Less volatile, high-quality bonds act as a counterweight, minimising potential losses or even providing stability during market downturns.

Generally, when stock markets face turmoil, frightened investors tend to seek refuge in high-quality bonds, driving down yields and increasing bond prices.

(This relationship doesn't always hold true, as demonstrated in 2022 and 1994).

Despite personally opting for a higher stock allocation with my own investments (I've a lifelong time horizon, hold an enduring and optimistic belief in the power of capital markets and have been an investment professional for 20 years)...

I still recommended the 60/40 to clients whenever it suits their specific situation.

There's no denying the past five years have been challenging for 60/40 'balanced' portfolios, given the global pandemic, the Ukrainian war, the shift from low nominal and negative real interest rates, the highest UK inflation in four decades, and a downturn in global stock markets in 2022.

But despite all this, the portfolio still delivered returns that more or less kept pace with inflation during this period.

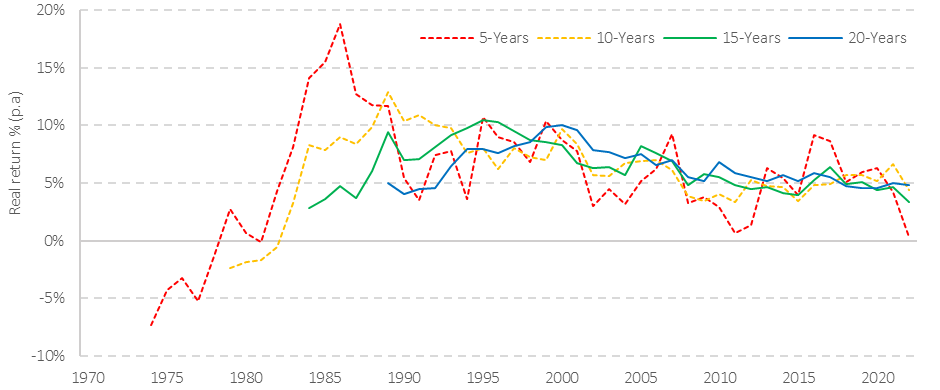

As shown below, the 60/40 structure has consistently increased purchasing power across the majority of five-year time horizons, with returns becoming more reliable, the longer investors hold.

60/40 annualised rolling real (after inflation) returns for different investment horizons

Data Source: 60/40 Balanced Portfolio Morningstar Direct © and Dimensional Returns Web

Take a look at the 1970s—a decade plagued by rampant inflation, which surged by a staggering 240% cumulatively from 1970 to 1979.

Not surprisingly, the five-year, after-inflation returns for a 60/40 balanced portfolio during this period were negative.

However, investors who persevered ultimately achieved positive real returns after 15 years, experiencing a 50% increase in purchasing power.

Those who held cash however, saw £100 drop to £85.

Investing is a long-term endeavor. From 1970 to 2022, the 60/40 balanced structure, on average, doubled an investor's purchasing power every 15 years.

Let's not forget the media is often influenced by recency bias, which in turn impacts investor decision-making.

Claiming the 60/40 balanced portfolio is dead might get clicks and accomplish their objectives, but it's statistically wrong and doesn't accomplish yours.

For example, the remarkable performance of commodity futures in 2021-2022 (a contract that obliges a buyer to purchase an underlying commodity like gold, at a predetermined future price), hides their overall underperformance compared to global stock assets over the long term (which remain undefeated).

Including assets like this in a portfolio, simply because of a brief period of strong performance, goes against both investment logic and empirical evidence.

Here's what is logical:

- Including shorter-dated, high-quality bonds as a valuable counterbalance to extreme stock markets.

- Bonds yield considerably higher returns than they did 18 months ago, meaning increased potential returns and a greater buffer against future yield increases.

- Bonds are often—but not always—negatively correlated with stocks, meaning they tend to move in the opposite direction.

- Markets are efficient, and attempting to predict which asset class will perform well in a given year is nearly impossible.

Therefore, it's crucial to have the patience to adhere to an investment strategy over the long term.

The last 5 years may have been unnerving for some, but for those where the 60/40 has been deemed suitable, the portfolio has done well to protect against rampant inflation.

The reports of its death are, to quote Mark Twain, greatly exaggerated.