Forty-six-year-old American, Amber Rhinehart and her fifty-two-year-old German husband, Johannes, took a financial risk when they moved abroad.

The couple has spent most of their careers working overseas.

That’s why Amber’s American Social Security retirement income will be far less than it otherwise would have been if she had stayed in the United States.

And Amber says Johannes won’t receive anything from the German government pension plan.

Amber works as an IB curriculum coordinator for an international school in Ghana.

She began saving for her retirement when she was twenty-nine and plans to be financially independent in 19 years, when she reaches sixty-five.

She and Johannes have two children, ten and eight years of age.

The couple invests about $60,000 USD (€56,532) a year in a portfolio of index funds.

But their portfolios are separate, for tax purposes.

“Johannes teaches at the same school I work at,” says Amber. “He will likely retire about five years before I do.”

She adds, however, that neither of them will put their feet up when they quit full-time work.

“I like the idea of being active in the International Baccalaureate community in some capacity after retiring,” says Amber.

That said, Amber wants the comfort of knowing she’s financially independent when she quits her full-time job.

Amber’s and Johannes’ portfolios are worth about $250,000 USD (€235,000) each.

They are also each adding about $30,000 USD (€28,266) a year.

But will that be enough?

Amber hopes it will be.

According to the German Federal Statistical Office, the median household income for people working in Germany is about €5,000 a month, before taxes.

Amber and Johannes hope to spend a similar amount when they retire.

But they won’t have to pay rent or mortgage costs.

This year, Amber and Johannes plan to buy a home in Berlin, mortgage-free, with money they have in a non-retirement account.

Unfortunately, however, inflation will take a really big bite.

The buying power of €5,000 per month will be a lot less in 19 years, when Amber retires.

Nobody knows the future inflation rate.

But developed world markets have averaged an inflation rate of about 3.5 percent per year over the past 100 years.

Some years, inflation has been far lower.

Other years, it has been much higher.

But if inflation averages 3.5 percent annually over the next 19 years, the equivalent buying power of €5,000 a month (€60,000 a year) in 2023, will be about €9,612 a month (€115,350 a year) in 2042.

Amber hopes her portfolio will provide enough income and capital appreciation to cover half that amount each year, while Johannes’ portfolio covers the other half.

In other words, Amber will need her portfolio to generate about €57,676 per year, indexed to inflation.

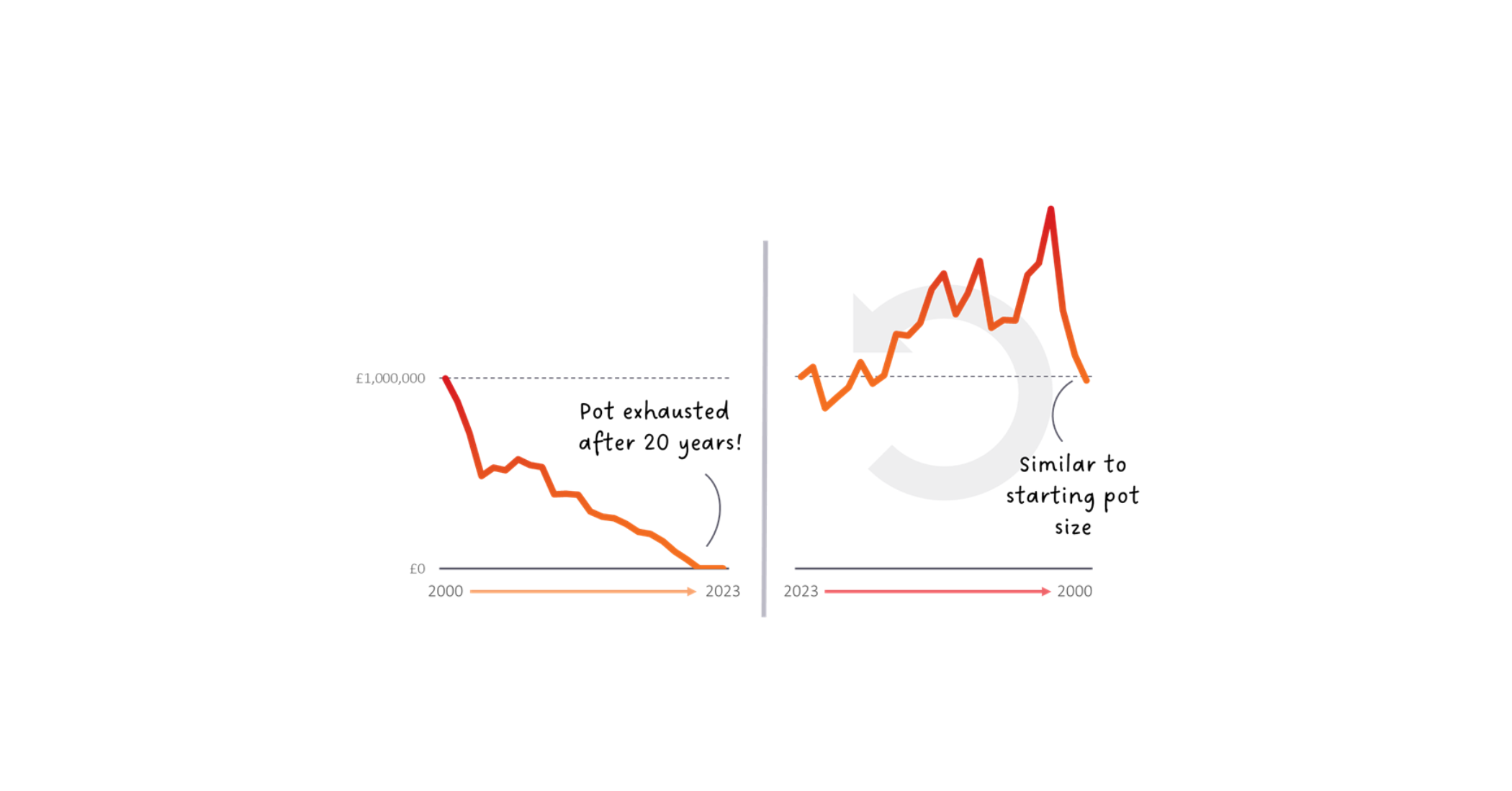

This brings us to the 4 percent rule of thumb.

Back-tested studies suggest that if a retiree withdraws 4 percent of their portfolio’s value during their first year of retirement, and increases the withdrawals each year to reflect the rising cost of living, the money should last at least 30 years, if it’s invested in a diversified portfolio of index funds.

In this case, the €57,676 per year that Amber requires would need to be 4 percent of her portfolio’s value.

To figure out her portfolio goal size, we simply multiply €57,676 by twenty-five.

That brings us to a portfolio goal size of €1,441,900.

57,676 is 4% of 1,441,900

and

57,676 x 25 is 1,441,900

You might recall that Amber’s current portfolio value is about $250,000 USD (about €235,000).

She is adding about $30,000 USD (€28,266) to her portfolio each year.

If Amber keeps this up over the next 19 years, she would reach her goal if her money averaged 4.71 percent a year.

As shown below, if her portfolio averaged 7 percent per year, her portfolio would be worth about €1,980,396 in 19 years.

That would provide Amber and Johannes with even more retirement income.

| Amber's portfolio value goal in 2042 | €1,441,900 |

| Amber's portfolio value in 2023 | €235,000 |

| Amount Amber is adding to her portfolio each year | €28,266 |

| Future Portfolio Value in 2042 at the following annual rates of return | |

| 4% | €1,308,550 |

| 5% | €1,500,209 |

| 6% | €1,722,531 |

| 7% | €1,980,396 |

| 8% | €2,279,431 |

| 9% | €2,626,116 |

Source:moneychimp.com

What’s more, Amber and Johannes will earn money working part-time after they quit their full-time jobs.

This will give them an even greater financial cushion.

Research suggests this part-time work should also help them live longer and happier lives as well.

The couple’s salaries will also likely increase over time, allowing them to invest even more over the next several years.

And when Amber turns seventy, she will be eligible to earn $12,000 USD per year in U.S. Social Security payments.

As for future medical costs, as residents of Germany, they will qualify for the socialised German medical plan.

Nobody can see the future, so we can’t plan for every possible outcome.

But if Amber and Johannes continue on the solid path they’re on, they should easily achieve their retirement goals.

Andrew Hallam is the best-selling author of Millionaire Expat (3rd edition), Balance, and Millionaire Teacher.