A pension and a mortgage are the two biggest financial responsibilities you'll ever have.

But when times are tricky, as they are currently in the UK, which should you prioritise?

Homeowners have been racing to make extra payments on their mortgages as borrowing expenses skyrocket. The average two-year fixed rate has surged nearly threefold, jumping from 2.52 percent in July 2021 to 6.85 percent at present, resulting in a significant increase in monthly payments.

The hardest hit in the UK have been the 1.4 million borrowers who have transitioned from a low-cost fixed mortgage rate this year.

There have also been reports of borrowers making large overpayments to reduce their balance and cut the interest they'll pay when their rate rises.

So, would taking this approach jeopardise your retirement?

In short, yes.

Moving money away from your retirement fund or pension is risky.

For a start, depending on how much money you divert, it could cost you in employer contributions and tax relief, which is likely to damage your retirement plans.

Mortgage vs. pension

So, what should you do with surplus cash?

The answer isn't simple.

A mortgage is the biggest debt most people will ever have.

There's also an undeniable sense of empowerment around becoming 'mortgage free' - not simply for financial reasons, but also to have the feeling of security that comes with removing such a large debt.

But underestimating the true cost of retirement can leave you in trouble.

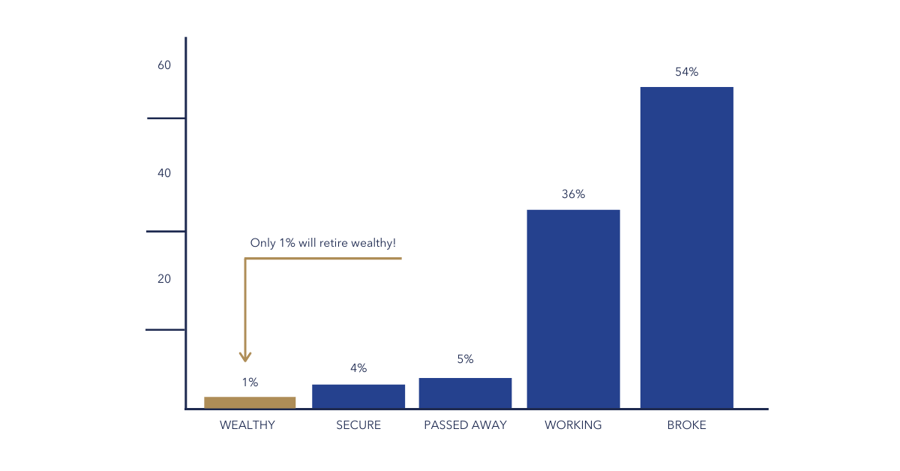

In the UK, about 60% of middle-earning private sector employees who contribute to a pension save less than 8% of their salaries, according to the Institute for Fiscal Studies.

Add to this rampant inflation, which added around a fifth to the cost of a basic standard of living in retirement in 2022.

So in this sense, most people will need to save more into their pensions or face a risk of running out of money in retirement.

To answer whether it's better to put extra cash into your mortgage or your retirement pot, you need to seriously consider lots of variables including interest rates, investment growth and of course, your age.

Interest rates in the UK are thought to be nearing their peak after the 14th rise in a row took place in August.

In this scenario, it may be right for you to prioritise maximising your pension contributions, for long-term benefits.

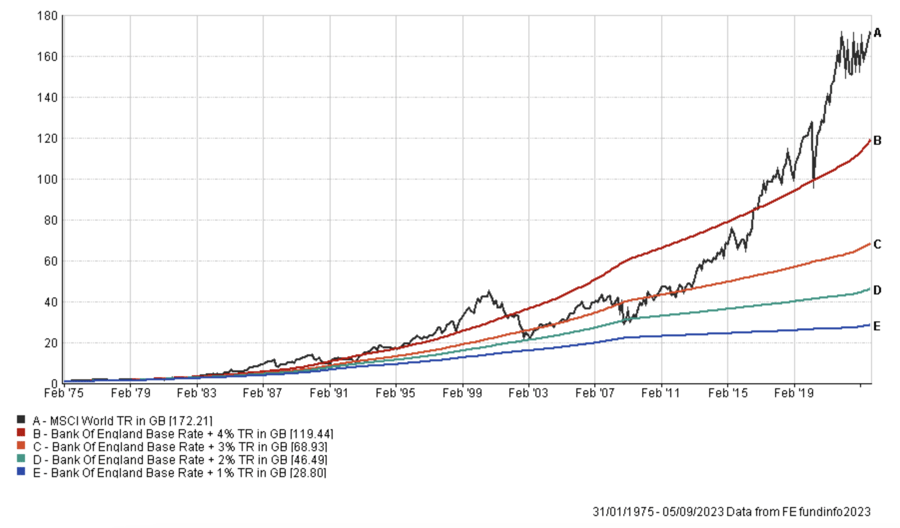

Also, the below chart shows that an equity-heavy portfolio should substantially outperform your mortgage over time, whereas a portfolio containing more bonds might not.

This overperformance can have a profound impact on your lifetime wealth but is extremely hard to calculate or envisage when the cortisol pumping through our brains is raging because of short-term financial pain.

Growth of £1 invested in global companies vs. the cost of mortgage interest

An example

Say you have a £200,000 mortgage paying an average interest rate of 6% across a 25-year term. On top of your minimum home loan and pension payments each month, you overpay £200 on your mortgage until it's cleared, about 19 years later.

For the remaining 6 years of the 25-year term (that would have been), you pay the equivalent of your mortgage payments, plus the extra £200, into your pension each month. Assuming average investment growth of 6% in a year, excluding any fees, your extra pensions will have grown to £171,455 at the end of the 25 years.

On the other hand, if you paid the extra £200 into your pension over the course of the 25 years, rather than the mortgage, you'd still be mortgage-free by the end of the term and would have a pension pot of £173,248 based on the same figures,

In other words, you'd be £1,790 better off.

This example assumes you received 20% tax relief on pension contributions from the UK Government, which tops up the pot at your normal rate of income tax.

So, if mortgage rates and investment performance are the same, the results are not too different.

The stock market and interest rates

Broadly speaking...

If the stock market is doing really well and growing at a faster rate than the interest rate on your mortgage, it's smarter to focus on saving for your retirement (putting money into your pension) first. This is because your investments have the potential to earn you more money over time.

However, if the interest rate on your mortgage is higher than what you can reasonably expect to earn from your investments, it might be a better idea to prioritise paying off your mortgage first. This means you should focus on reducing your mortgage debt before saving for retirement.

In simpler terms, if your investments can make you more money than your mortgage is costing you, save for retirement first. But if your mortgage is more expensive than what you can earn from investments, pay off your mortgage before saving for retirement.

This is why looking at the expected annualised return of a portfolio is so important as short-term performance should never cloud your calculations around long-term expected returns. From the perspective of an investor - the experience of volatility within the stock market can feel flat despite the medium to long-term trajectory of capital markets being anything but this.

UK house prices vs. global companies

And then there's tax.

If you're thinking of paying off your mortgage early and then putting more money into your pension as you get closer to retirement, you need to be careful about taxes. Even though there's no strict limit on how much you can save in your pension each year, there's a point where you'll lose some tax benefits and might have to pay extra charges.

You can get tax relief on your pension contributions, but that's based on how much you earn in a given tax year (your contributions need to be equal to or less than your earnings in the same tax year). So, if you earn £40,000 and put £50,000 into your pension, you'll only get tax relief on the first £40,000. However, if your employer contributes to your pension, this limit doesn't apply to their contributions.

There's also an annual allowance of £60,000. Anything you save into your pension above that will not benefit from tax relief on your contributions.

When choosing between focusing on your pension or your mortgage, tax relief on pensions can be a significant factor. If you pay off your mortgage first and then contribute a lot to your pension, you might not get the full tax benefits if your pension contributions exceed your taxable income. In other words, it's important to consider how taxes can affect your decision to prioritise either your pension or your mortgage.

Also, if you're in a higher income tax bracket, waiting to increase your pension savings might not give you as much tax relief as you expect.

If your income decreases as you get older and you no longer qualify for higher rate tax relief, it can be more expensive to save large amounts in your pension. In other words, your retirement savings could become less tax-efficient if your income drops over time.

Time horizon and risk

If you're considering putting extra money into your pension or paying off your mortgage faster, you should consider two things: how many years you have left until you retire and how comfortable you are with taking financial risks.

If your goal is to earn more from your investments than what you'd save by paying off your mortgage early, you'll need to aim for higher returns. These typically come from investing in the stock market. But it's important to note that this approach works best if you're thinking long-term and have a good amount of time before retirement.

So, consider how long you have until retirement and your willingness to take on investment risks.

Retirement is becoming more expensive because of inflation. People who are about to retire need to plan for higher costs of things like food, fuel, energy, and clothing.

In fact, the yearly income required for one person in the UK to have a decent standard of living in retirement, after taxes, has gone up by 12% compared to last year.

The good news is, people are starting to save more towards their golden years.

In summary

Putting money into your pension gives you a tax benefit right away, but if you pay extra toward your mortgage, it can open up opportunities like buying a bigger house or having more money available before you retire. In other words, both options have their advantages, but they serve different financial goals.

Deciding whether to pay off your mortgage early or invest more in your pension is a complicated choice. It depends on things like interest rates, how your investments are growing, and your age.

Paying extra on your mortgage can make you feel secure and free up money before you retire. However, you must think about how this affects your retirement savings in the long run.

If you neglect your pension contributions, you might not have enough money saved for retirement. This is especially concerning because the cost of living is going up, and you'll need a significant pension fund.

It's often a good idea to find a balance between paying off your mortgage and saving for your pension. This way, you can maximise tax benefits and make the most of investment opportunities.

If you're not sure how to do this, it's a good idea to work with a life financial planner who can help you make a solid plan for your financial future.