At a dinner recently, I got talking to a friend of a friend.

Naturally, once she found out what I do, the conversation turned to money.

She told me about the first time she earned over $100,000. Hitting six-figure status was very important to her.

It was a marker of success.

She's since gone on to earn much more:

"The thing they don't tell you is that more money comes with more responsibility, more pressure, more demands, and ultimately, less flexibility, autonomy, and freedom", she said.

Turns out, chasing money without first examining her relationship with money turned out to be the wrong choice for her.

The relationship with money needed to be there first.

Relationship with money

If you don't know you have a relationship with money, you probably don't have a very good one.

But what does it mean to 'have a relationship with money?'

We all have relationships with living beings - partners, family members, friends, colleagues, even pets and other animals.

But how can we have a relationship with someTHING?

It's a good question.

By analogy, think about your car.

Some people take good care of their car so that it'll take good care of them. Some people don't really care about it and thus don't care for it, taking it for granted.

Some people keep it immaculately clean, and to others, the cleanliness of their car isn't something they think people should care about - or that a dirty car means it's doing its job!

Some people know exactly how it works and how to fix it if something goes wrong. Others wonder if they have to take their car in just to have antifreeze put in.

As we see with a car, it's possible to have a relationship with an inanimate object.

Money is no different.

Whether you know it or not, you have a relationship with money; everyone does. Whether it's good or bad, and whether you want to or not, this relationship exists.

It can be complicated

Many of us don't know we have a relationship with money, but even for those who do, it's not always a great relationship.

Maybe you make pretty good money but aren't saving as much as you'd like.

Perhaps you spend more than you know you should, on things that aren't important to you.

It could be that you're afraid of money and don't ask for it, leaving you a habitual underearner.

Maybe you make good money, are saving, and not spending too much, yet you still feel anxiety and stress when it comes to money.

Or, you and your partner have very different feelings about money, leading to money fights.

Money is stressful for most people and made more stressful if we have a complicated relationship with it.

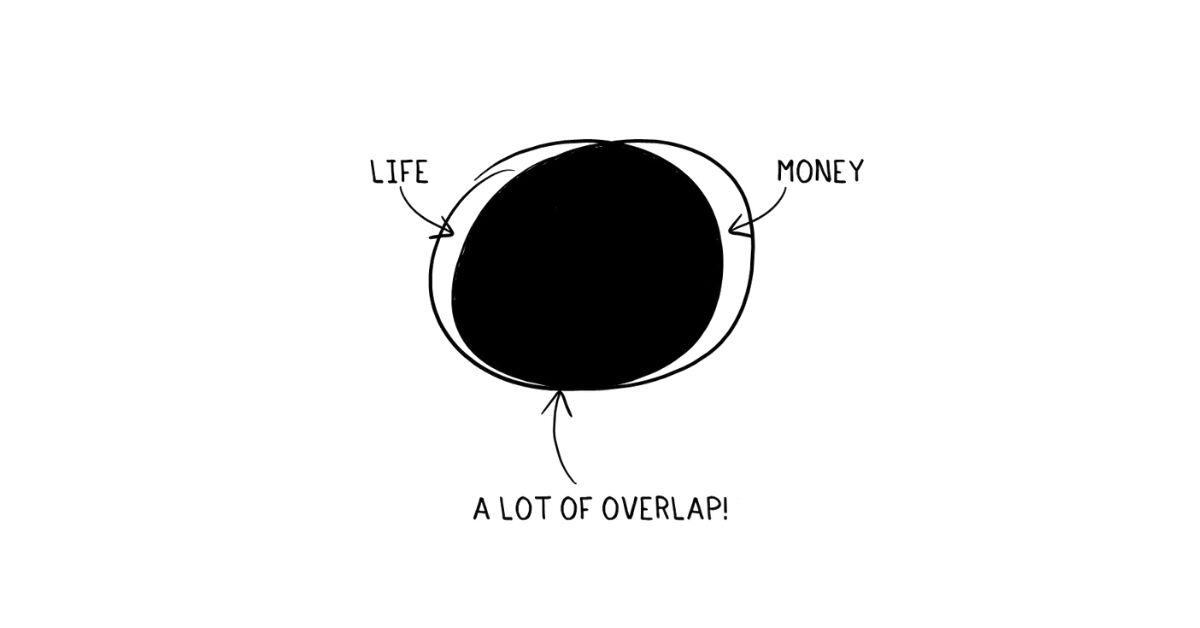

Money is everywhere

It's no wonder money is so stressful, it touches every area of our lives.

Property: Do you rent or buy? How much can you afford? How high should your fixed expenses be? What's the rate on your mortgage?

Career: How much will you make? Are there ways to keep taxes low? Are you making what you're worth?

Well-being: Do you want to relax? Can you afford to take some time off? Does your form of relaxation cost money? How much?

Relationships: Do you want to have a conversation with your partner? Does money come up? Are you both spending money in the same way? Are you trying to keep your partner from knowing how much you actually spend?

There are few financial decisions that don't involve your life somehow, and few life decisions that don't have a financial tether.

Exploring your relationship with money

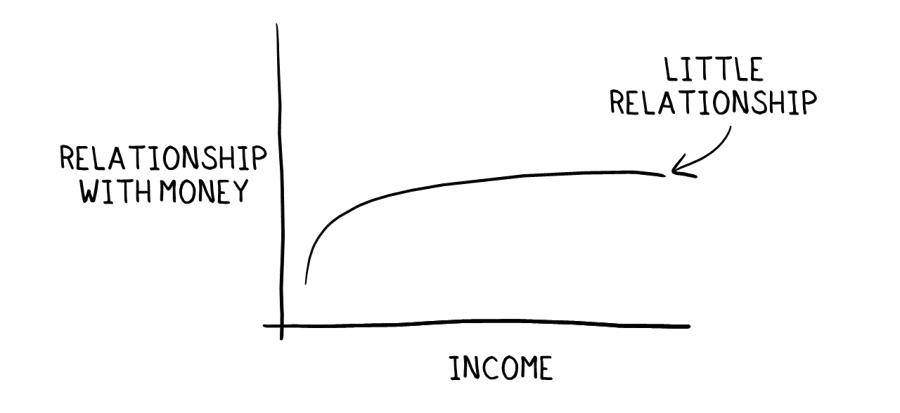

A common solution most of us jump to is that we simply need more money. That seems like an obvious solution. We perceive our issues are due to a lack of money and, therefore, if we had more money we would be better off.

If you've gone through a major promotion, job change, or financial windfall like a settlement, inheritance, or other payout, you probably know that your financial issues don't go away.

They may have changed, sure.

But if you're frustrated because you haven't been able to change your financial habits or you still suffer from financial worry, it might be time to take a look under the hood and examine your relationship with money.

It's not about how much you make.

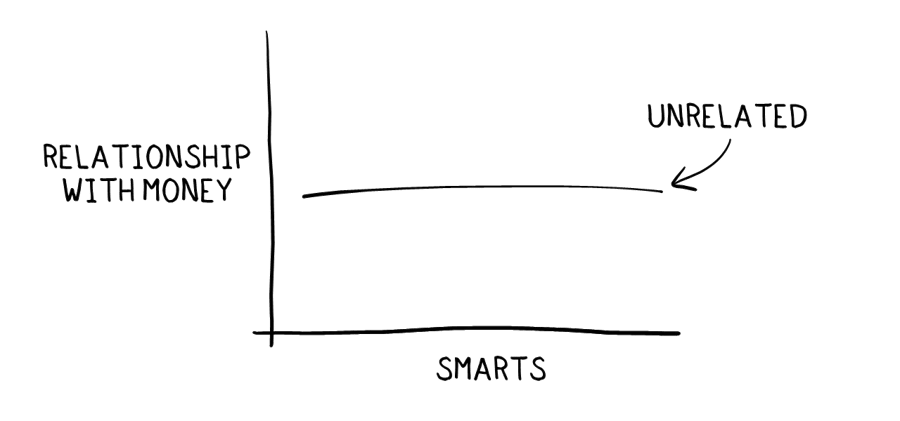

Your relationship with money isn't about how smart you are, either.

Many people have tried to fix their money issues before and haven't experienced success. Or, if there was some success, it was short-lived.

It's easy to fall into the trap of thinking that the failure to achieve lasting change is due to insufficient information or not being smart enough.

Strengthening your relationship with money isn't about how smart you are. In fact, being too smart might hurt if you believe that you can get ahead if you just do more research.

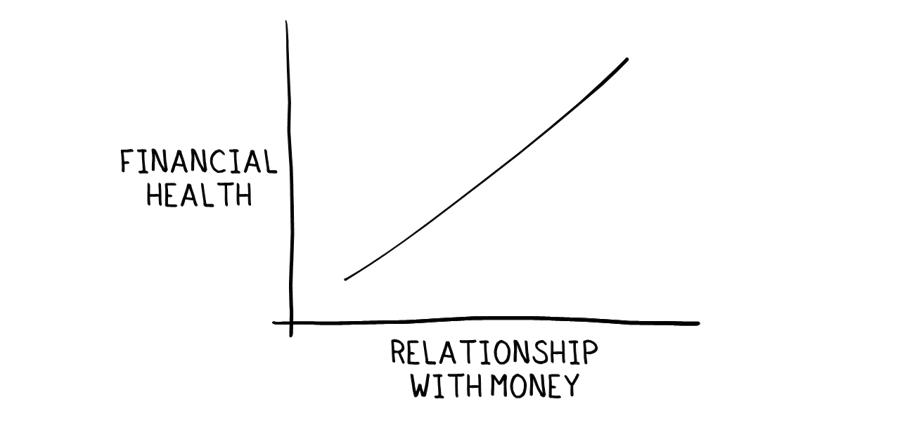

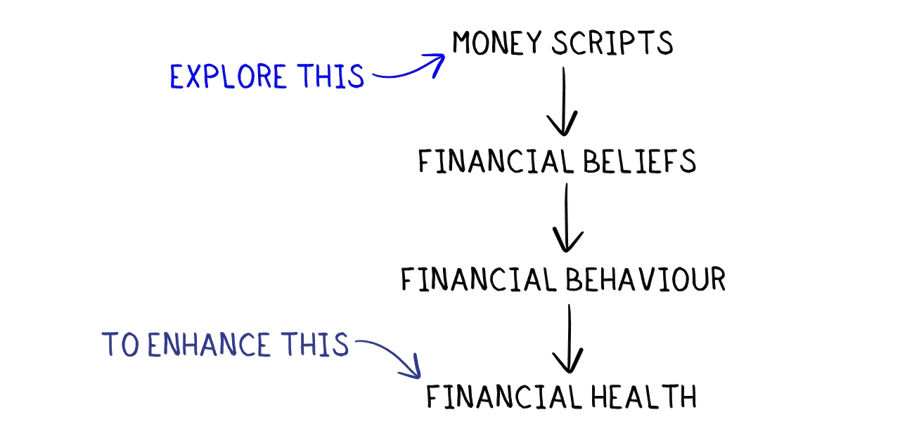

To increase your financial health, it's more important to address the hidden causes of your money troubles, which means exploring your relationship with money. In order to truly be comfortable with money, you need a better, healthier relationship with it.

Improving your relationship with money will often lead to better outcomes, less stress, and less worry.

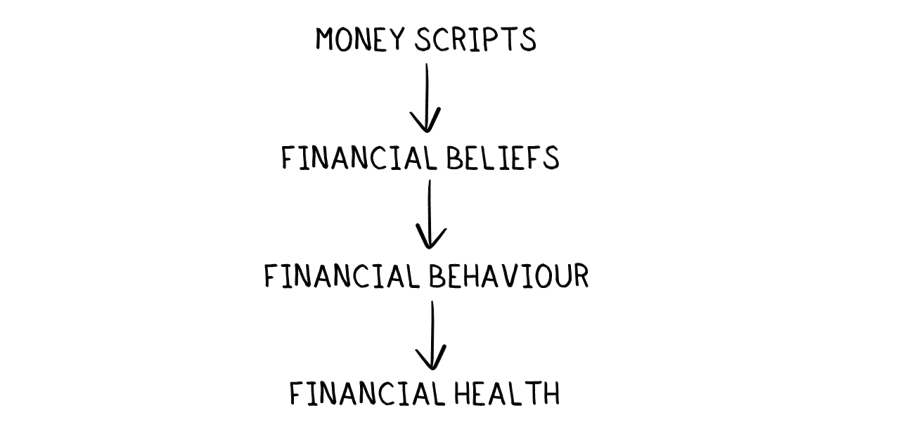

Relationship with money and money scripts

The key to strengthening your relationship with money is understanding what's driving your financial behaviours.

In financial psychology, these are called money scripts, and they determine your money personality. Money scripts represent rules that we subconsciously follow about money. They are developed through our experiences - mostly in childhood, reflect partial truths about how money works (though our subconscious treats them as whole truths), and are hidden underneath conscious awareness.

Essentially, money scripts are the stories we tell ourselves about money.

Maybe you learned that money should be saved and not spent. Or you have learned that you deserve to treat yourself. You could have learned that "rich people" (whatever that means) are bad.

Perhaps you don't think you deserve money. A money script is any rule that we make up and follow. If you don't pay attention to money and your money scripts, you are being ruled by these invisible rules.

Improving your relationship with money means exploring the money scripts that drive your behaviour.

Sometimes you'll recognise there are money scripts that have been mostly good and only slightly limiting.

Other times, you may notice money scripts that made total sense at one time in your life, but they don't make sense anymore.

You might also find money scripts that have been behind what you thought was self-sabotage. The good news is that once you know about them, you can work to change them.

New financial habits and systems can be accomplished and will lead to financial health.

You'll be able to use your money to design the life that you want.

You'll have reasonable debt that was a conscious choice.

Your financial stress will be minimal, and you'll have good habits that make it easy to do the right thing.

Financial health is attainable.

You just have to train yourself to stop thinking it's about finding more data and research.

Focus on improving your relationship with money and learn the money stories you've been telling yourself.

Life is short; don't be a slave to money.

Author and behavioural scientist Sarah Newcomb has a fitting saying: you can live “a life you love...with the resources you have.”