When most high-earning professionals think about retirement, they assume they’ll need to cut back.

Be more cautious. Live off less.

But what if the opposite was true?

What if you could actually spend more, and reduce the risk of running out of money?

It sounds counterintuitive.

But after more than 20 years advising successful professionals and their families, I’ve seen it happen over and over again.

Retirement success isn’t about how much you save. It’s often about how you spend.

So in this article, I’ll walk you through a smarter way to approach your retirement income. One that allows you to enjoy the wealth you’ve worked so hard to build, without constantly second-guessing every financial decision.

Along the way, we’ll cover:

- Why traditional withdrawal rules often backfire

- How flexible guardrails can increase your spending and security

- The hidden risks most professionals overlook (and how to fix them)

- Real-life stories from the families we advise

- And why the real risk may not be running out of money, but working too long and missing out

Retirement isn’t a finish line - it’s a transition

Let’s start with a mindset shift.

Too many high achievers view retirement as an on/off switch. You're either working or you're not. You're saving or you're spending. But it doesn’t work like that.

One client came to us at 49 with over $4 million saved. He assumed he’d need to keep grinding for another 5–10 years, just to be “safe.” But when we asked him to define what retirement meant to him, he said:

“Honestly? I want to wake up naturally, take four proper trips a year with my partner, and stop worrying about money.”

When we ran the numbers - stress-tested them through market volatility, inflation, and long-term care costs - we found he could retire right now and enjoy everything he’d described.

He didn’t need more money - he needed more clarity.

And that’s true for most people at this level.

Why the 4% rule is dangerously outdated

One of the most common (and costly) mistakes we see is over-relying on the 4% rule. The idea that you can withdraw 4% of your portfolio in the first year of retirement and increase it by inflation each year.

Sounds neat and simple. But real life is neither.

The 4% rule assumes:

- Moderate, steady inflation

- Predictable markets

- A flat, unchanging spending pattern

- No large, irregular life events (good luck with that)

We worked with one client with a $3 million portfolio planning to withdraw $120,000 annually.

Looked fine on paper.

But when we ran real-world scenarios - including market crashes, tax increases, and healthcare shocks - it fell apart fast.

Worse still, the 4% rule encourages underspending in your healthiest years - when you have the time, energy, and freedom to make the most of your life. That’s a tragedy we see far too often.

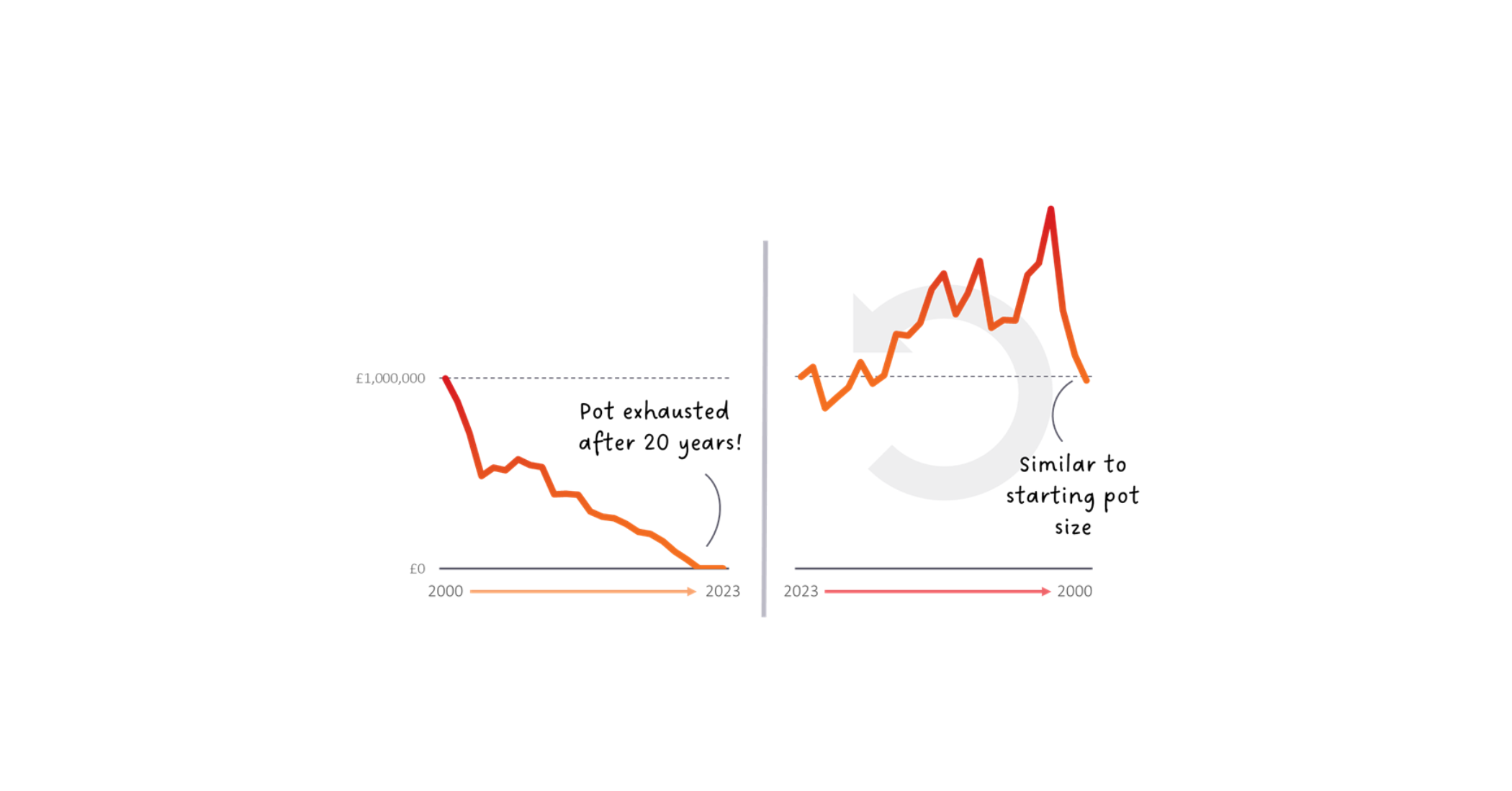

The better way: flexible spending with guardrails

So what’s the alternative?

We use guardrails - a system that adapts your spending based on market conditions and gives you far more lifestyle freedom, without added risk.

Here’s how it works, using the MSCI World Index:

- Market <10% below all-time high → Spend your full discretionary budget

- Market 10–20% below → Cut discretionary spending by 50%

- Market >20% down → Pause discretionary spending

This isn’t guesswork. It’s a clear, data-driven framework that protects your lifestyle in the long run and lets you enjoy more in the good years.

Let’s say you’ve got a $1 million portfolio:

- Essentials: $27,500/year

- Discretionary: $27,500/year

- Total: $55,000/year

In a normal market: spend the full $55K

In a moderate dip: cut discretionary in half = $41,250

In a bear market: spend essentials only = $27,500

In a bull market: spend more if you like - maybe $60K guilt-free

Compare that to the 4% rule’s $40K/year every year, regardless of what’s happening.

Which one sounds more aligned with how life actually works?

Discretionary vs essential: know the difference

Another crucial step most professionals skip is separating their spending into discretionary and essential.

One client swore he needed $180,000/year to get by. But $60K of that went to golf, fine dining, and luxury holidays - all wonderful, but entirely optional.

When you blur the lines, you end up doing one of two things:

- Cutting everything in a panic during downturns

- Spending everything blindly during upswings

Guardrails work only if you apply them to the flexible part of your lifestyle. That’s where the real leverage lies. So create two budgets:

- Essentials: food, housing, insurance, healthcare

- Discretionary: travel, hobbies, gifts, upgrades

Then let the market tell you when to spend more or less. Not the headlines. Not your emotions.

Sequence of returns: the hidden risk most overlook

It’s not just how much you spend - when you spend matters even more.

Let’s say you retire with $1 million and plan to take out $100K for a luxury trip.

But just before you do, the market drops 20%. Now your portfolio is worth $800K.

You go ahead with the trip anyway. After that, you’re left with $700K - and even if the market rebounds by 25%, your portfolio only grows to $875K.

Why? Because that $100K wasn’t around to benefit from the recovery.

This is called sequence of returns risk, and it’s the silent killer of early retirement. Guardrails help you dodge it by reducing withdrawals in bad years - keeping your portfolio intact for the bounce back.

The lifestyle illusion: when high income hides real risk

Let’s shift gears for a moment.

We’ve worked with clients earning $500K, $800K, even $1M+ a year. You’d assume they’re financially bulletproof. But many aren’t even close to ready for retirement.

Not because they didn’t save - but because they didn’t plan.

One partner at a professional services firm came to us with over $4 million saved and wanted to retire at 52. But when we ran the numbers, he was set to run out of money by 70.

His portfolio was poorly structured, his lifestyle was under-analysed, and he was sitting on $1M in cash - losing value to inflation daily.

High income gives you options.

But it doesn’t guarantee freedom.

Emotional spending, boredom, and the hidden cost of lifestyle upgrades

We also see something more emotional, and less obvious: expensive boredom.

One client retired early with no real plan. Within two years, he’d burned six figures on start-up ideas, high-end hobbies, and luxury trips - not because he was careless, but because he was lost.

He hadn’t retired to anything - just from something.

Others try to justify every spend with, “I deserve this.” And maybe they do. But retirement isn’t a reward phase. It’s a decades-long lifestyle that needs intentionality, not indulgence.

We always ask clients: what will give your life meaning when you’re no longer chasing the next deal, promotion, or bonus?

Purpose isn’t just good for your mental health. It’s critical for your financial health too.

The wrong relocation dream can be a six-figure mistake

And then there’s the fantasy relocation.

Whether it’s the Amalfi Coast or Lake Como, many retirees dream of escaping to a slower pace of life abroad. But most approach this like a holiday, not a financial decision.

One client fell in love with Positano.

But when we asked about healthcare, visas, taxes, or how exchange rates might affect his lifestyle - he had no answers. It was a romantic idea, not a viable plan.

Here’s our advice: rent before you buy. Spend at least three months living there as a resident, not a tourist. Navigate the daily reality. And talk to a cross-border financial life manager early - not after you’ve bought the villa.

Retirement isn’t just about income - it’s about outcomes

We often ask clients four questions before we give them a retirement green light:

- What does retirement actually mean to you?

- What are you spending today - and is that accurate?

- What do you want to spend, and when?

- Have you stress-tested your plan?

Most people guess their number, or choose an age out of thin air. But unless you’ve modelled it through volatility, inflation, taxes, healthcare, and changing lifestyles - it’s just that. A guess.

We help clients forecast across three phases:

- The go-go years (50–70): active, expensive, exhilarating

- The slow-go years (70–80): gentler, more routine

- The no-go years (80+): less about travel, more about care and comfort

This way, we can tailor your portfolio, and your withdrawals, to your real life, not a textbook model.

You’ve saved the money - now make sure it lasts

Here’s the harsh truth: your money doesn’t retire, even if you do.

Too many people shift everything into cash or “safe” bonds the moment they step away from work. But without enough growth, inflation will eat your future alive - especially over 30+ years of retirement.

Instead, we advise clients to think in layers:

- Layer 1: Cash - for short-term needs and peace of mind

- Layer 2: Income - to support your lifestyle now

- Layer 3: Growth - to outpace inflation and protect your future

This structure gives you confidence and flexibility. It also allows you to enjoy your best years now - without sabotaging your later ones.

Final thought: what if you’re actually more ready than you think?

We’ve talked a lot about avoiding mistakes. But the truth is, many professionals are closer to the life they want than they realise. What’s missing isn’t more money - it’s better decisions.

And the biggest risk?

Waiting too long.

Working longer than you need to.

Missing the window when you’re healthy, curious, and energetic enough to enjoy it.

So if you’re starting to ask, “Can I afford to spend more?” or “Can I actually retire sooner than I thought?” — don’t guess.

We’ve helped hundreds of high-income individuals build flexible, sustainable retirement plans that actually match their values and their lifestyle.

If you’d like to see what’s possible for your next chapter, book a free Discovery Call. It could be the conversation that changes everything.

Related resources:

-

✅ Download the Retirement Checklist for HNWIs — used by hundreds of professionals to pressure-test their plan

-

▶️ Watch: “Avoid these 7 mistakes if you want to stay retired"