A partner at a global law firm once told me, “I’ve been climbing what feels like a wealth mountain for 25 years… but I've no idea how to enjoy it once I get to the summit".

That line stuck with me.

Because it sums up the paradox of wealth: you’ve worked hard, built an extraordinary portfolio - often many millions - and in theory, you could retire tomorrow.

But without the right system, even wealthy professionals in Dubai can see their freedom quietly slip away.

Over the last two decades, I’ve seen families with $10m+ portfolios drift back into work. Not because they needed the money, but because their perfect plan fell apart when life veered off script.

The truth is, staying retired isn’t about hitting a number. It’s about applying seven essential financial truths - choices, safeguards, and habits that protect both your wealth and your well-being, wherever life takes you across Dubai and the wider GCC.

Let’s explore them.

1. "Safety" isn’t what it seems

A friend of my father retired with a sizeable nest egg and kept millions in cash. It gave him comfort, a sense that no matter what happened, he was insulated.

But over time, his real wealth quietly eroded.

Inflation was the silent predator.

To the untrained eye, nothing seemed wrong.

But our planning software told a different story: his heirs lost millions in compounded growth that was never captured.

This is the first trap many wealthy retirees fall into: mistaking familiarity for safety.

Cash feels safe.

Dividends feel safe.

US large caps feel safe.

But safety in retirement isn’t about what feels familiar - it’s about building resilience.

The solution is to use a tiered cash system.

- Immediate bucket: 6–12 months’ cash for unknowns.

- Short-term bucket: 2–5 years’ expenses in high-quality bonds.

- Long-term bucket: Global equities — the family fortress that protects you against decades of inflation.

This tiered model means you’re never forced to sell investments in a downturn, while still compounding wealth for the long run.

Cash alone won’t keep you safe.

Only structure will.

2. Taxes don’t retire when you do

One executive came to us a year after leaving work, frustrated.

His regular salary had stopped, but somehow his tax bill was higher.

The culprits?

Mandatory pension withdrawals, dividend income, and cross-border complexities pushing him into higher brackets.

Many professionals assume taxes taper off in retirement.

In reality, they often become more complicated - especially for families with international holdings, UK pensions, offshore accounts, and property in multiple jurisdictions.

The solution here is multi-jurisdictional tax planning.

- Begin in your 40s, not after you’ve retired.

- Use partial transfers into tax-efficient structures.

- Structure philanthropy and charitable giving to offset liabilities while supporting causes you care about.

- Sequence withdrawals from different accounts to avoid triggering unnecessary brackets.

Retirement isn’t the end of taxes.

It’s a new phase that demands coordination.

3. Lifestyle clarity is worth millions

A Dubai executive insisted she needed $12m to retire.

“I can’t downsize,” she said, thinking about her villa.

But when we unpicked her real priorities - travel, entertaining, being near water - the house wasn’t essential.

She trialled two months in a waterfront apartment in Portugal.

She spent less, felt more alive, and her retirement number dropped by millions.

She opted for a lifestyle reset.

- Identify your true non-negotiables.

- Test-drive different living arrangements.

- Be ruthless about habits you’ve outgrown.

Retirement is a rare chance to reset defaults.

Without clarity, you risk funding a lifestyle that doesn’t exist anymore.

Don’t just plan your money.

Plan your time and your environment.

4. Rigid withdrawal rules can cost you life’s best years

A private equity partner with $10m followed the famous 4% rule.

On paper, it looked perfect: $400k a year, adjusted for inflation. In reality, he was underspending.

He skipped holidays, flew economy, and denied himself experiences he could easily afford.

We modelled his plan - even under conservative assumptions, he was more likely to die with more than he started with.

His caution was costing him life itself.

What was needed? Guardrail withdrawals.

- Spend normally in strong markets.

- Cut back slightly if markets fall 10–20%.

- Pause discretionary spending if markets drop more than 20%.

Think of guardrails as barriers on a mountain road.

They don’t stop you driving, they stop you going over the edge.

Flexibility beats rigidity.

A dynamic plan often allows for more lifetime spending with less risk.

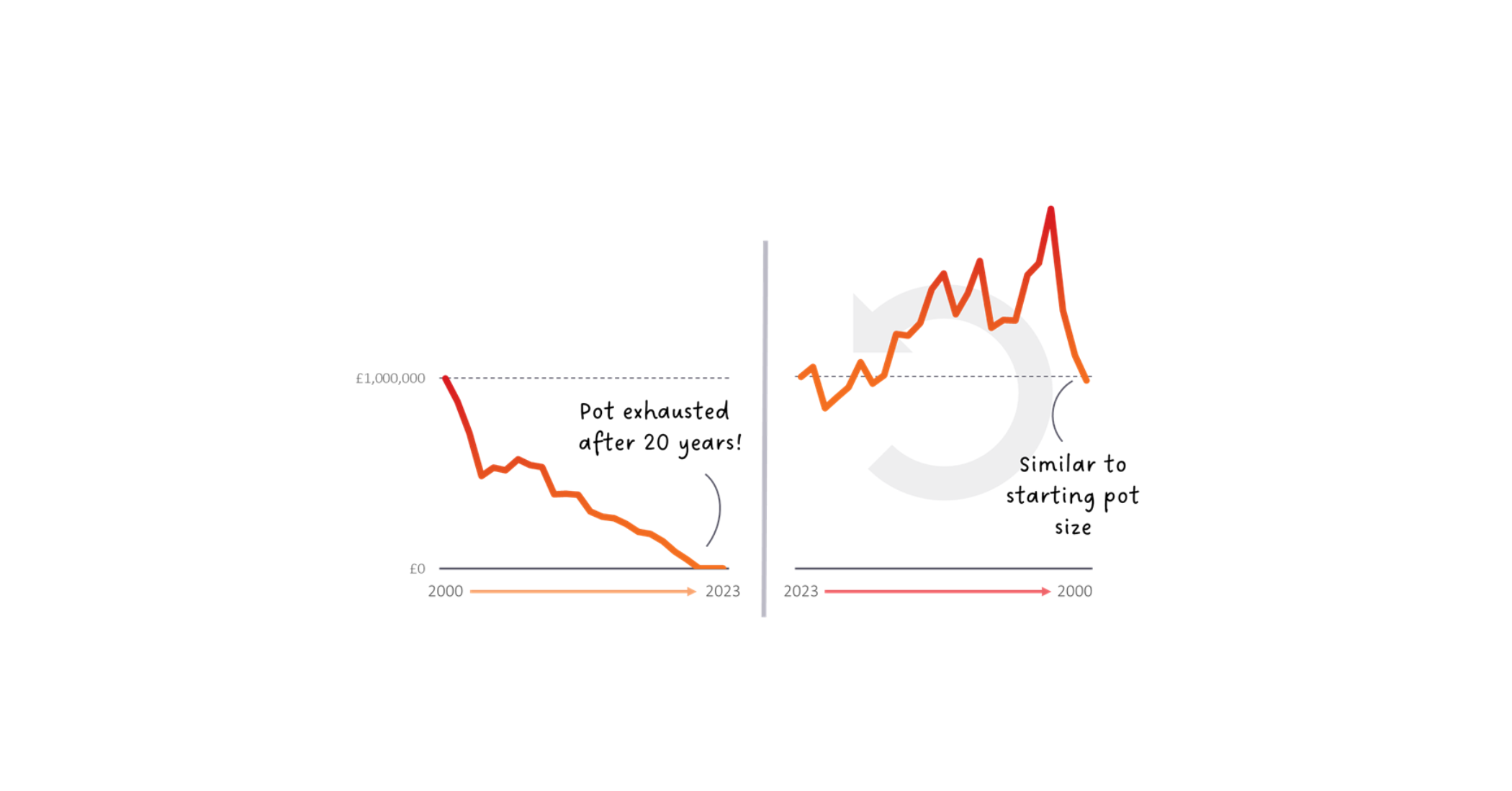

5. Concentration feels safe, until it isn’t

From 2000 to 2010, the S&P 500 delivered flat returns.

A retiree with $1m invested only in that index, withdrawing 5% annually, would have run dry in 16 years.

A globally diversified retiree? They finished richer than they started.

The framework to consider here? Simple. The Great Companies of the World.

- Don’t just own US equities. Own businesses globally.

- Diversify across sectors, geographies, and asset classes.

- Avoid home bias - familiarity is not protection.

Concentration feels safe because it’s familiar.

But in retirement, familiarity can quietly be the riskiest position of all.

Diversification isn’t dilution. It’s protection.

6. Legacy and lifestyle must be balanced consciously

A strategy consultant in his late 40s told me: “I want the kids to be looked after, but I also want to enjoy what I’ve built.”

Noble goals.

But when we modelled his plan, it leaned heavily toward legacy - cautious withdrawals, minimal spending.

He had a money personality focused on vigilance and commitment.

But he was unconsciously prioritising his heirs at the expense of his best years.

Time to consider the 'Spending vs. Ending' ratio.

- Decide what percentage of wealth is for you.

- Decide what’s truly meant to be passed on.

- Build your drawdown plan accordingly.

Trying to maximise both enjoyment and legacy, without clarity, often leaves you in no man’s land.

You underspend out of guilt, and you leave behind more than you intended.

Define your ratio.

Clarity avoids regret.

7. The biggest risk is the one no one talks about

A client once admitted, “I’ve planned for everything… except getting old.”

It’s uncomfortable to face, but ageing brings complexity: long-term care, incapacity, sudden loss.

Ignoring it can devastate families, emotionally and financially.

Model to age 100.

- Stress-test for illness, disability, or sudden death.

- Put the right insurance and legal documents in place.

- Tailor care planning — don’t buy one-size-fits-all products.

Planning for decline isn’t pessimism.

It’s the ultimate form of protection.

Bringing it all together

Here’s the paradox of wealth: the more complex your finances, the easier it is to overlook the basics.

Safety, taxes, lifestyle, withdrawals, diversification, legacy, and long-term care - these aren’t just “nice to haves.”

They’re the system that keeps you retired.

If you want to stress-test your own plan against these truths, we’ve put together a free HNWI Retirement Checklist. It’s the same framework my team and I use with successful professionals across the GCC to make sure they’re not just financially ready, but life-ready.

Because retirement isn’t the finish line.

For wealthy professionals in Dubai with $1M+ portfolios, it’s about applying these seven essential financial truths so you can not only retire, but stay retired with clarity and confidence.

It’s the summit of your first mountain - and the start of your second.