Every financial decision is driven by one of two fears:

The fear of losing money...

Or the fear of missed opportunities.

The former is far more common.

The fear of losing money is a primal instinct, deeply ingrained in our psyche.

This is reflected in the concept of 'loss aversion'. It turns out, the pain of losing money is psychologically twice as powerful as the pleasure of gain.

This means we're typically much more likely to avoid investing because we fear the potential losses...

This manifests itself as indecision, inaction, inertia, apathy, inattention and internal resistance.

This isn't wrong.

It's human.

Even the most successful, intelligent, wealthy individuals find investing scary.

But in the modern world, the consequences of doing what feels safe in the short term, is always the most damaging in the long term.

In fact, it's typically more carcinogenic to your future purchasing power (and thus your future life opportunity) than the unaided human mind can calculate and comprehend (the complexities of compounding).

A caring, empathetic, professional planner helps you visualise this opportunity cost and, using prudent assumptions, can put an exact number on this to enable greater decision integrity.

This doesn't necessarily mean investing, but understanding more deeply the right option for you, your family and your future.

The reality is that long-term investing is hard.

The biggest reasons more people don't practise long-term investing are that:

- It flies in the face of anything taught to us – that is, short termism – where most influencers/experts come from;

- It requires a painful degree of patience because it's only over long periods of time that the market eventually gravitates toward value;

- Evolution plays mind tricks upon us;

- Our attention spans and holding periods are shrinking; and

- Noise is deafening.

Given all of this, sensible long-term investing has become an increasingly difficult and contrarian endeavour. And so, not many investors have the wisdom, guidance or the wherewithal to practise it.

So below are 5 of the most common reasons why people fear investing, as well as some thoughts on how to overcome them.

1. Fear you'll lose money

We're human.

We love stories and we've all heard many about family and friends who've lost money.

Hundreds of thousands of years of evolution haven’t wired our brains to deal with money but to use our finely tuned ‘fight or flight’ response mechanism to keep us alive.

Everything that may be considered ‘good personal finance’ today could have been disastrous to our ancestors.

For example, our ancestors didn’t lose much if they ate all their food at once; they can just find more tomorrow (retirement didn’t exist).

But if they failed to avoid a lion – game over.

The brain therefore pays way more attention both to surviving today rather than thinking about tomorrow, and to avoiding risks rather than seeking pleasure.

A lion in the wild.

RED LINES ON A SCREEN.

These couldn’t sound more different.

But both can cause fear.

Indeed, disembodied threats in modern life are no less ‘real’ than the ones that ROAR.

What’s the natural response to a falling market?

For many, it’s like seeing the lion.

In both cases, we’re wired to get away from the threat as quickly as possible. In the case of the lion, that makes perfect sense. In the case of long-term investment, it may turn out to be an over-reaction.

To overcome this fear?

First, change your mindset; understand that genuine investing isn’t like gambling.

Investing has been thoroughly researched by the academic community. There’s plenty of independent, peer-reviewed, and time-tested evidence, dating back to the 1950s. Several of the academics responsible for it have won a Nobel Prize in the process.

It’s about making high quality, calculated decisions to grow your future wealth, rather than letting it be needlessly eroded.

Second, diversify your portfolio.

Being well-diversified is:

- Primarily about not losing money permanently;

- About avoiding being stuck in a few companies, a sector or a country that performs poorly over an extended period of time and takes a long time to recover; and

- About sensibly capturing those areas of the market that – at a particular moment in time – are driving returns. Recently, it may have been all about US technology firms, but tomorrow it will be something else entirely.

Third, have a safety harness.

Run frequent ‘what if’ scenarios across your financial, health and life domains with your financial life manager.

This way, you’ll always have the confidence to know you’ve done your best to prepare for the unexpected.

Finally, understand your money personality.

If you fear loss more than others, it's probably your money personality driving your decisions.

Our relationship with money is almost never about the numbers. It’s about the stories we tell ourselves because of those numbers. We all come to believe certain stories based on our upbringing and our interaction with money. Our childhood experiences, parents and culture all impact this.

This behaviour is where our relationship with money is rooted, and it’s also where sound money management begins.

Find out your money personality in 2 minutes.

2. Fear you'll fall behind or miss out

This is the second most common fear I hear.

Also known as FOMO (fear of missing out on opportunities), it often prevents people from building wealth in the stock market.

Humans seem to be obsessed with those who appear to live a “better” life.

We tend to compare our investment results with our friends and colleagues.

And, one of the great misconceptions about investing is that you have to be busy anticipating and reacting to market events and opportunities.

That’s not where the evidence suggests that success lies.

In fact, NOT doing something is often far harder than doing something. Sometimes investors get tempted to look through a hindsight lens at other ‘better’ performing investments or forward at ‘obvious’ future events.

This can lead to risky behaviour, such as jumping on an investment bandwagon without doing your research.

Examples include buying whatever is currently 'hot' or trying to target outsized returns (speculating).

To overcome this fear?

Remember good investing is a decades-long game.

As Peter Lynch, one of the most successful investors of all time, said:

”The real key to making money in stocks is not to get scared out of them.”

Focus on your financial plan and stick to your life strategy.

Ignore everything else and get on with your life.

3. Reacting to market volatility

Every five years (on average), we can expect a decline of about one-third, as we experienced in 2020. We all know the stock market doesn't move in a straight line, but rather fluctuates around a generally upward trend.

We call this “volatility”.

Unfortunately, we can't consistently predict ahead of time when these fluctuations will happen, or when they'll reverse.

As mentioned earlier, the natural response to a falling market is that we're simply wired to get away from the threat as quickly as possible.

When we’re calm and rational, all parts of our brain work together.

However, when we experience stress or other heightened emotions, we experience ‘emotional flooding’ and our animalistic parts of the brain overpower the thinking brain.

They flood the thinking brain with chemicals, removing logic and any reflections on the consequences from decision making, and our ‘fight or flight’ responses kick in.

When it comes to market volatility this can all push us into survival mode, and lead to bad money decisions.

No one knows when markets will go up or down. Short-term disappointment must be accepted because this, along with uncertainty, is the price of admission for better long-term returns.

It's simple. We don't time the markets because:

- No one can

- We don't need to

- It's distracting

Great results come to those willing to wait to see the fruits of their labour.

To overcome this fear?

Have a safety harness (see point 1).

Stay calm, manage your emotions and stick to your long-term life strategy. Time, patience and discipline are the ingredients required for a successful investment experience.

4. Lack of knowledge

Investing can seem intimidating and complex.

This fear stems from the Dunning-Kruger effect, a phenomenon where people with low ability at a task overestimate their ability.

Their poor self-awareness leads them to overestimate their own capabilities.

With investing, this means the LESS you know, the MORE confident you might feel.

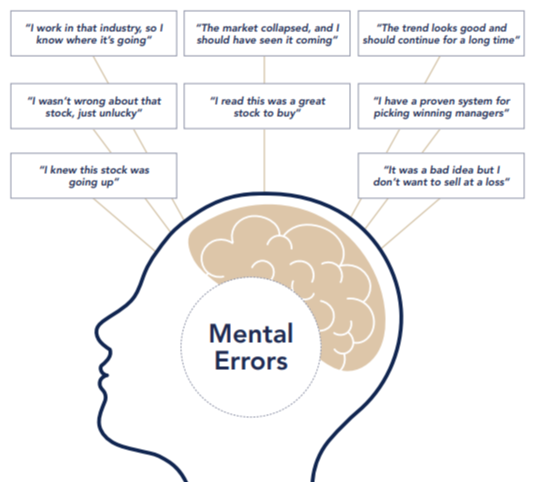

Having spent more than 40,000 hours working as a professional adviser, I know that I'll never know as much as the Nobel laureates in Economics who I rely upon. But, I often meet new investment hobbyists who tell me they have found better solutions. Wisdom suggest they are sitting upon what the Dunning-Kruger effect terms 'Mount Stupid', and are simply unaware of what they are unaware of...

A lack of knowledge or the wrong money scripts can lead to fear, procrastination and inertia.

Inertia seems to come from outside us.

We blame work, family commitments, a lack of time, or a lack of knowledge. But inertia arises from within. It’s self-generated and self-perpetuated.

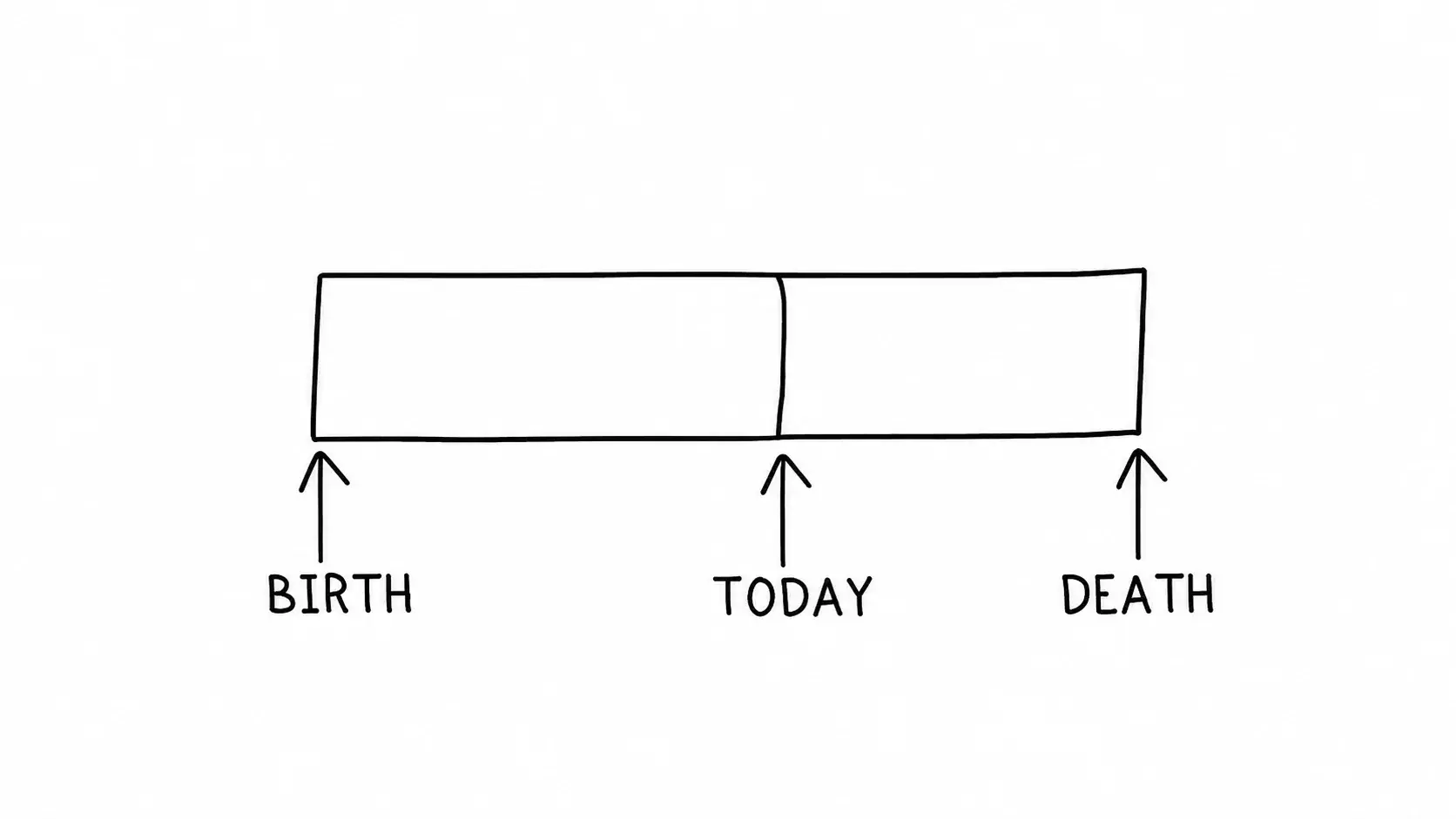

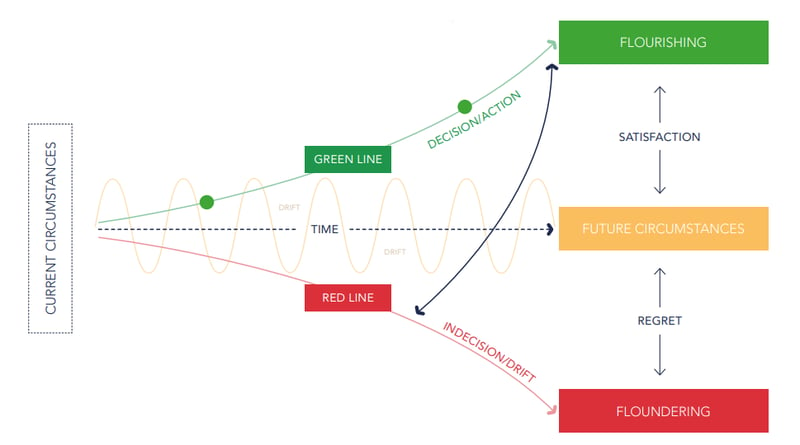

In life financial management, inertia manifests itself as ‘indecision’ and ‘drift’ (see the red line).

It’s typically more costly than can be imagined by an untrained mind and ultimately robs you of future life opportunity.

To overcome this fear?

Work with a sage and experienced guide who can help keep you on your green line (above), extrapolated from a detailed cashflow plan.

As pioneers of radical change within financial services, we do this by challenging convention, creating deep transformation, and empowering you with the knowledge to confidently make well-informed financial and life decisions.

5. Fear of commitment

Successful investing is typically a decades-long commitment. But not being able to access your money for a significant period can feel daunting.

What if you need to use that money after all?

But certainty is only available in the long term.

History also tells us that the longer you leave your money invested, the more chance you have of it going up, and the lower the likely downside.

You have to find the right balance between liquidity (bring able to access your money quickly) and growth (increasing it's value over time).

Don't continue to avoid investing because of this fear. Avoidance typically manifests itself as indecision, inaction, resistance, apathy, inertia, procrastination, wrong action, status quo bias and ultimately, in downward drift (red line).

Here we’ll typically see people endlessly languish in outdated, inappropriate, and poorly-performing products, that quietly rot their future purchasing power/life opportunity.

To overcome this fear?

Keep enough cash to cover 6 months' of living expenses.

This means you can comfortably invest your other funds, without worrying about the need to access them in an emergency.

The unlived life: regret is far more worrying than any fear

Whenever you find yourself scared of investing, remember this.

In our experience, the cost of inaction is typically both invisible and unimaginable to the unaided human mind.

Time and again this inaction compounds over time and often leads to catastrophic but extremely hard to see consequences.

For example, those with a ‘Vigilance’ money personality are typically driven by fear and scarcity, experiencing emotional pain which drives them to avoid any form of spending.

Frugality is a strength, but being ‘penny smart but pound stupid’ can often have crippling effects.

This gets to the root of the unlived life.

You must properly understand this cost of opportunity, time and lost future purchasing power.

This is often not measured in monetary terms, but in units of future life regret.

Imagine yourself years from now.

Did you let fear dictate your financial decisions?

Did you miss out on life choice, freedom, love, connection, peace of mind, security, living an authentic life, autonomy, happiness, and the possibility of getting what you want, because of a cognitive fear and inattention?

Yes, there will be risks. There's always risk in every part of life.

But as long as you invest systematically and control your behaviour, you'll grow your wealth and therefore your life opportunity in the long term.

By thinking about the kind of life you want to live, you can use your money as a tool to design – and live! – that life, so you can enjoy happier lives and, in the end, look back with fewer regrets.