Investing is something we all need to do

It’s also hugely important to get it right.

The 10 principles inside will help you take advantage of opportunities provided by efficient capital markets, and provide a systematic, time-proven way to reach your financial goals.

.webp?height=900&name=Pursuing%20a%20better%20investment%20experience%20downloadable%20asset%20(3).webp)

The five decisions

- The Do-It-Yourself decision

Should you try to invest on your own or seek help from a professional? If so, who? - The asset allocation decision

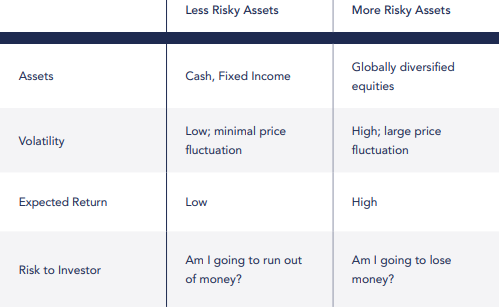

How should you allocate your investments among stocks (equities), bonds (fixed income), and cash? - The diversification decision

Which specific asset classes within these categories should you include in your portfolio, and in what proportions? - The active versus passive decision

Should you opt for an actively-managed approach to investing , or a more passive approach? - The rebalancing decision

When should you sell and when should you buy more?

Each of these decisions significantly influences your overall investment journey.

Whether you realise it or not, every day you're making these decisions, even if you choose to maintain your current strategy and take no action with your investment portfolio.

Below, we'll provide you with the necessary knowledge to navigate these decisions. To assist you in making intelligent choices, we'll share our perspectives.

We're therefore evolutionarily wired to buy stocks and bonds when their prices have already increased. We do so because we feel comfortable and confident during market upswings. Conversely, when markets decline, fear takes hold, and we often rush to sell.

This behaviour often leads us to buy at (or near) market peaks, and sell at (or near) market bottoms, resulting in the failure to capture even a market rate of return.

Whilst our psychology (ego) protects us from thinking we're making these errors or reacting in the wrong way - the reality is we're all human and this is played out in the numbers from studies such as Dalbar.

Our emotions around money aren’t limited to just investing. With saving, borrowing, spending, earning, and giving … all of these areas of money life trigger their own unique brain chemistry.

Our 'saving' brain is a bit different from our 'investing' or 'charitable' brains (cortisol, dopamine, oxytocin and endorphins). So, when we say your money fears and anxieties are all in your head, that doesn’t mean it’s made up or illegitimate. Not at all. It’s literally true.

Our emotional attachment to our hard-earned money is powerful. When we take risk, even just a little, we can feel it. It’s a physical sensation in addition to an emotional one.

With our money decisions, and with the emotional rollercoaster of investing in particular, it can be comforting to know that this is just who we are. With that knowledge, we’re a bit better able to pause and reflect, to gain perspective on what triggers us, even to adapt.

Fear of regret

The fear of making the wrong investment decision can often lead to hesitation and inaction.

We may leave money uninvested out of fear of entering the market at the wrong time. It's important to remember that the right time to invest is when we have the funds available, and the right time to sell is when we need the money.

Affinity traps and personal relationships

There is a huge difference between genuinely unconflicted advice where you receive uncomfortable truths, and conflicted advice where you are likely to receive comfortable lies.

Most people prefer the comfortable and personable option. We must acknowledge the dangers of falling into affinity traps. How often do we make investment decisions based solely on our personal connections, those we meet on the golf course, or the recommendations of respected individuals? Although these feel extremely natural decisions (how much we like someone), relying on such factors without detailed due diligence and research can be extremely risky.

There are other emotions that can negatively impact our financial well-being. Charles Kindleberger, an economic historian, found that seeing a friend become wealthy can disturb and disrupt our own judgment. These emotional reactions, in turn, cloud our decision-making process.

Recognising these biases is crucial for making informed investment decisions. By understanding that the media and behavioural tendencies can influence our actions, we can take a more measured and rational approach to investing. It's essential to focus on long-term goals, conduct thorough research, and seek advice from unconflicted professionals to ensure a more certain financial pathway and improve your overall financial well-being.

Now, the question arises: which type of adviser should you choose?

Bankers, brokers or fee-based financial life managers?

In the past, bankers and brokers were the primary sources of investment advice due to the limited availability of independent, fee-based, fiduciary advisers and planners.

However, times have changed, and you now have a choice.

It's important to understand the significant differences between the two options before deciding.

Small vs. large companies

Growth lines highlight the inherent relationship between risk and return.

For example, small company stocks tend to carry higher risk compared to large company stocks, consequently yielding a higher return.

This is seen in practice when banks are considering interest rates for lending. A bank evaluating lending to a small company versus a well-established entity would naturally charge the small company a higher interest rate due to its greater risk and increased likelihood of loan default.

Equity investors approach risk in a similar manner, demanding a higher rate of return from smaller companies. The outperformance of small company stocks relative to large company stocks reflects a risk dimension known as the size effect. This elevated return serves as a reward for assuming greater risk within a properly functioning free capital market.

It's important to note both small and large company stocks entail higher risk compared to bonds. Hence, it’s unsurprising that both small and large company stocks have generated greater returns than long-term government bonds, which, in turn, have outperformed treasury bills (characterised by lower risk due to shorter maturities).

While it’s possible for treasury bills to outperform stocks in any given year, it is extremely unlikely over any prolonged period of time.

As long-term investors, we should look beyond these fluctuations and consider the historical data and investment theory, which strongly suggest the existence of a prevailing risk and return hierarchy over time.

Value vs. growth companies

Another crucial aspect of risk in equity markets is known as the value effect.

Value stocks are characterised by low stock prices relative to their underlying accounting metrics such as book value, sales, and earnings. These stocks often represent distressed companies with limited earnings growth or unfavourable prospects for the future.

On the other hand, growth stocks are associated with highly profitable and rapidly expanding companies, resulting in higher stock prices relative to their underlying accounting measures.

As of the time of writing, many large bank stocks are considered value stocks. While these banks possess significant assets, they also face notable financial challenges. Consequently, equity investors today demand a higher return from large banking stocks to compensate for the increased risk they present.

Diversification: key points

Knowledge, success or longevity is no substitute:

Many investors ridicule diversification, believing their skills or investment history have shown they're beyond such a quaint concept. This is arrogance/overconfidence masquerading as foresight. They're not immune to calamity.

The wipe out:

Companies can and do fail. They may have the benefit of regulators offering a clean bill of health and lawyers attacking critics. It's cold comfort on the day of failure, when a company tumbles 90%.

Diversification may not be what you think:

Self-directed investors often devise their own versions of diversification. Whilst they understand the general concept, they've usually done little to effectively diversify or lower their risk. And diversification is not buying two investment properties instead of one.

Lower volatility:

Having uncorrelated assets within a portfolio helps to lower volatility, can help to improve returns, and make your wealth compound faster.

View your portfolio as a whole:

Looking at last year's or last month's best performer will only serve to frustrate you. Last year's best may be this year's worse and vice versa. View the total return and measure it against your goals.

Overlap:

Judicious portfolio construction ensures assets aren't crossing over each other. Using funds with similar characteristics lowers diversification.

Diversification doesn't eliminate risk:

At some point it won't matter how much you've diversified, there's a threshold where risk still exists. No investor can escape it.