On a recent flight back to Dubai, I got talking to an oil and gas professional named Neil.

After discovering I was in financial services, he was all too eager to share his own experiences with his 'adviser'.

They often met up for a round of golf.

In fact, his 'adviser' became part of his close circle of friends.

During the conversation, I kept biting my tongue.

After years of hearing them...

I knew how stories like these inevitably ended.

I was sceptical about Neil's 'adviser'.

He had recommended Neil invest in structured products.

They were inflexible and expensive.

They had a term of at least 10 years.

(Most senior international professionals in Dubai don't stay this long).

Early withdrawals come with huge exit penalties.

Nevertheless, I kept my thoughts to myself and offered Neil a Second Opinion Review.

It's a service that puts investments under the microscope.

Showing investors the evidence of how an investment is either working for, or against them.

Neil agreed to the review - after all, what did he have to lose?

Our team of chartered financial planners took the list of products and created his review.

I then had the awkward job of ringing to explain the evidence we'd uncovered…

- £110,000 in commission paid to his friend’s brokerage;

- Significant market underperformance;

- Years of extra work now required to save for his retirement.

It all boiled down to one thing.

It’s best not to choose your finance person based on ‘friendship’.

Most of us wouldn't go for drinks or a round of golf with our doctor or lawyer.

Does that make them less trustworthy?

No.

The cost of free and friendly financial advice

In traditional financial services, free and friendly financial advice is driven by commission bias.

Close rates and charisma are valued more than professional expertise.

Fortunately, financial reforms are in the UK.

But in "expatriateland" – where you and I live – the old, commission-based model is alive and well.

As Frank Furness, one of the top sales trainers in the financial marketplace says:

“It’s the best job in the world. Where else can I go out and meet somebody, drink their coffee, eat their cake, and walk out with $5,000 in my pocket? No other business!”

But beware - that’s your money ending up in their pockets.

You're paying for their 'friendship'... as Neil discovered.

7 alarming things to know before hiring a financial planner

Financial planning is a lifelong commitment.

You need to make sure you partner with someone who has your best interests at heart.

With so much at stake - your retirement, children's education, dream property...

You cannot leave your ideal future in the wrong hands.

So here are 7 alarming things you must know before hiring a financial planner.

1. Too many people trust the wrong people

The US Federal Reserve did a survey of consumer finance, and found that friends were the average American's number one source of information for making financial decisions.

The reforms that ended direct-selling in the UK were focused on ensuring that something as important as giving financial advice was delivered by professionals, not friends or salespeople.

Think about chartered accountants, lawyers, engineers, doctors, teachers and architects as examples of professionals from whom you might seek advice and then remember - if you think it's expensive to hire a professional, wait until you hire an amateur.

2. The numbers don't lie

Often the only way to tell whether financial advice is working is to look at the numbers.

And as evidenced by another US study, most people have no idea whether the financial advice they are receiving is good or bad until a long time after they’ve received it.

You shouldn’t care less whether an adviser is likeable or not, you just need to care about the value they bring.

People often tell me they are happy with their investments because they are ‘up’.

But 5 or 10% up over a period of years in which the market is up over 120% isn’t good.

A professional may give you some uncomfortable truths from time to time, but they will also quickly set you back on the best course for financial success.

Your friendly salesperson on the other hand will continue to feed you comforting lies.

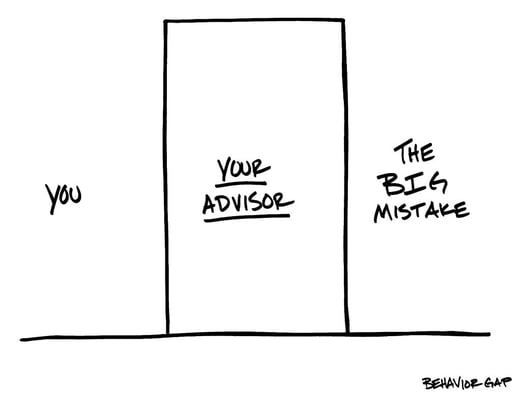

3. Entire life savings have been lost to the wrong 'adviser'

The expat financial adviser, who's been introduced to you by your friend or colleague, works in a system that’s beyond their control – a system that has tremendously powerful financial incentives to focus on maximising its profits over yours.

- Who has tracked you down and is cold calling you at work;

- Who is turning up where you socialise;

- Who’s been introduced to you by your friend or colleague; and

- Who’s now offering you the benefit of their free advice

...works in a system that’s beyond their control – a system that has tremendously powerful financial incentives to focus on maximising its profits over yours.

This system has made victims of 1000s of senior international professionals.

The damage for some has been irreparable.

Like this investor who lost an astounding £210,000 to hidden commission.

Or this lawyer who paid his adviser £66,000 the very day he signed on the dotted line.

4. There are more than 200 different titles for financial advisers

Offshore, over 98% of all international financial advisers, no matter what job title they go by, are brokers.

This means they’re incentivised to sell.

Your needs, goals and ambitions don't matter.

Their needs take priority.

5. Most 'advisers' do not have your best interests at heart

You'd be forgiven for thinking that every stock and bond broker, financial planner, wealth architect, IFA or whatever other made-up title your friendly adviser goes by, has a legal responsibility to act in your best interests.

This so-called fiduciary duty is actually only held by a very small portion of the entire wealth management profession.

And this fiduciary standard is only upheld by those financial professionals who charge fees instead of commissions.

For example, those holding chartered status from the Chartered Insurance Institute.

Does your friendly 'adviser' qualify?

6. 'Financial advisers' who operate on your time, at your expense

You use a professional for things you cannot do yourself...

Either because you don’t know how, or because you think they will do it better or more efficiently.

The only thing you want from them is the best advice you can get.

Am I right?

Friendship doesn't even factor into the equation.

Now compare a professional’s approach to that of a financial salesperson who seemingly has oodles of time…

Time for a round of golf, time for a drink, time to travel across the country to see you...

This is how traditional direct salespeople have always operated – on your time, at your expense.

7. The right financial planner is also a life coach

Do you want a financial professional who will help you reach your goals?

Or a buddy?

Do you want a doctor who tells you what’s wrong and then helps you?

Or one who brushes off your concerns and invites you out for a drink?

If you consider your current adviser to be an implicitly trusted friend...

Perhaps it's time to break ties and find a more professional adviser who separates finances from friendship.

At the end of the day, having the right financial planner in your corner is about more than having a money manager.

It's like having a life coach.

Since money is only the means to get and keep the life you want.

It makes sense to find someone who's as passionate about your goals and ambitions as you are.

A financial planner would want you to live richly.

And keep you on track even when the markets test you and the news taunts you.

Understanding the various roles of a financial planner is key to knowing what you deserve.

If you'd like to chat to one of our planners, get in touch.

The first call is on us and gives you the opportunity to see if we're the right fit for you.

We hope to hear from you.