Some years ago, two international professionals in the UAE decided to start investing to maximise their significant earnings.

Mark and James were very much alike:

- Both were high earning executives in oil and gas,

- Both shared a passion for golf,

- And both were filled with ambitious dreams for the future.

Today, Mark and James are still very much alike in many ways.

But there’s a difference.

Mark has retired already, even though he’s only just fifty, and he’s enjoying the time of his life in Dubai’s perpetual playground, playing golf every day with his friends.

James is in Dubai too…

- Still working,

- With no retirement date in sight,

- Sadly, with his best laid financial plans laid to waste.

What made the difference?

Have you ever wondered what makes this kind of massive financial difference when it comes to investing?

It isn’t intelligence, talent or luck.

It isn’t that Mark wanted to succeed and James didn’t.

The difference is, Mark decided he needed a solid and reliable investment solution, backed by research and evidence.

- An approach that was low cost,

- Fairly low risk, and

- Pretty much hands off…

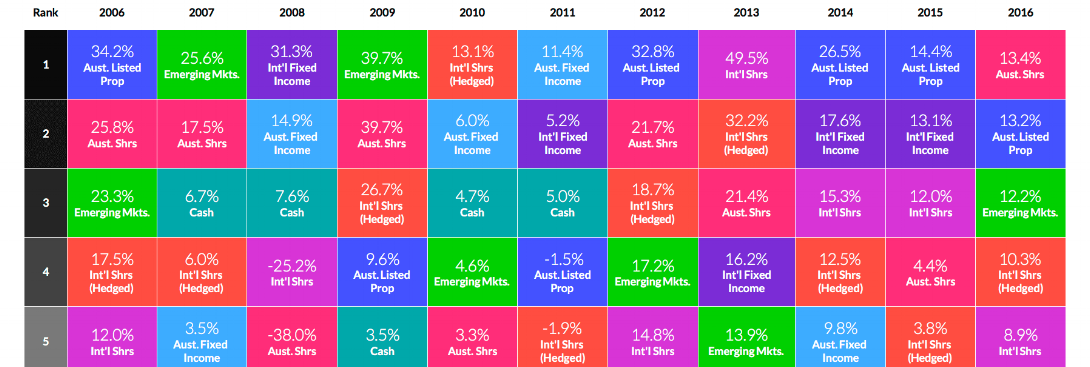

Mark understood that investors weather regular financial storms, and that markets correct themselves with time, rewarding long-term investors handsomely.

So, he decided to go for a passive, evidence-based investment approach, rather than trying to guess and time the market.

And, because Mark was a busy executive who knew he wouldn’t have time to worry about his investments every day, he took the approach of ignoring financial news, investing regularly, and leaving the management of his passive portfolio to a professional.

He chose a chartered financial planner who shared his passion for passive investing, established a well-diversified portfolio of exchange-traded funds, and got on with his life.

On the other hand, James just wanted to save as much time, effort and money as he could, so chose a financial salesperson who offered his services for free.

- He transferred James’s BP pension to a QROPS,

- Sold him an offshore investment bond to wrap all his money in,

- And got James in to some really exciting-sounding funds, that had all seen massive gains in recent years.

It was a one stop investment solution – quick, simple and seemingly free…

James figured he could always upgrade and employ a personal wealth manager to stock pick once he’d made some serious gains.

But the first time James received a portfolio valuation, he saw his pension and investments had shrunk because of massive fees he’d had no idea he’d have to pay.

And it got worse.

The risky and badly diversified investments inside his bond crashed, wiping out over half his fund’s remaining value.

At that point James panicked, and decided he needed to claw back what he could before he lost the lot.

He emailed his 'adviser' and told him to cash in the bond, and pull his money out of the failing funds.

He’d learned his lesson.

Or so he thought.

It turned out the salesperson no longer worked for that brokerage, and if James wanted to encash, the offshore investment bond and underlying investment providers still had fees and charges they’d need to claw back first meaning the money James had already lost was only the start of it.

Instead, it was suggested James speak to a new 'adviser' at the brokerage, who recommended James transfer what little money he had left into much better investment funds…

And top up to make up for lost time, James decided to make the best of a bad job, and took the recommendations – after all, he wasn’t the financial expert.

He decided to trust the new 'adviser'; he was giving his time for free to try and help James get back on track.

The salesperson assured James that the new funds he was recommending had a fund manager with a very successful track record, who knew when to buy and sell to beat the market and capture the biggest gains.

But all James did by transferring and topping up was expose his money to more risks and more charges.

When his next portfolio valuation came through, James felt defeated, and the indifferent response he got from the brokerage was the final straw.

Fortunately, James still had his job, his health and his visa to live and work in Dubai.

So, although his trust was destroyed and his financial wellbeing undermined, today James is managing to save some money each month into an account back home.

It isn’t really earning him anything, but it’s not losing him anything either, (unless you take inflation into account).

An investment approach unlike any other

Mark managed to avoid all that pain, simply by starting with a systematic, evidence-based investment strategy.

He avoided high and hidden costs, the stress of trying to time and beat the market, and the risks of being badly diversified.

He also chose a chartered financial planner whose interests were entirely aligned with his own interest, who charged a transparent fee for his ongoing advice and portfolio management services.

As a result, there was no clawing back of hidden commissions from Mark’s invested wealth, no expensive fund switches, and no need for Mark to worry about being abandoned by his adviser.

Evidence-based financial advice was only the beginning.

Mark also got:

- Better results,

- Peace of mind, and

- Lower charges

His portfolio was:

- Diversified,

- Balanced, and

- Risk appropriate

Plus, Mark was free to access his money whenever he wanted.

And when Mark wanted to ask a question, make a change or get advice, his planner was there to help.

An investment in success

Contact us to find out how a low cost, systematic investment management approach could benefit you.

If you don’t like what we have to say, you can just walk away – no cost, no commitment.